")

EUROPEAN OLIVE OIL MARKET REPORT - APRIL 2025

As the 2024/25 harvesting season wraps up, the market is now looking forward to the flowering of the olive trees. Stakeholders are closely monitoring market activity, particularly as prices have fallen while production levels remain high. A report from AICA, released this week, will provide valuable insights into how the market is evolving.

Weather Conditions

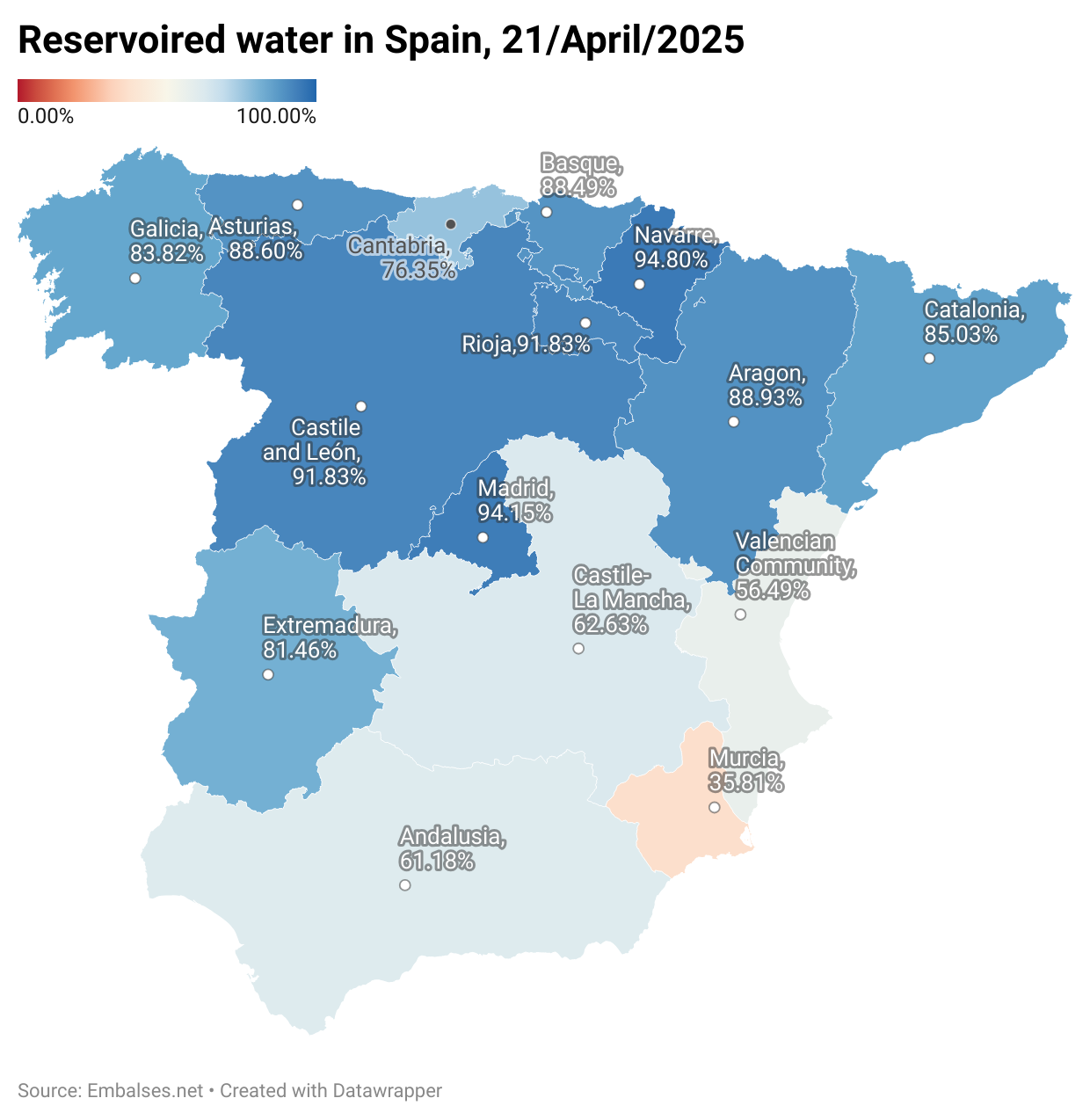

In April, the weather has positively impacted water reservoirs in Andalucía, keeping their levels above 60%. While this high level does not ensure a complete recovery of crops for the upcoming season, it does promise adequate irrigation for the trees throughout the summer.

As we enter the flowering phase, it is crucial for the weather to remain stable and mild. Avoiding extreme temperatures and heavy rainfall will help protect the flowers and support fruit development in the coming weeks.

Outputs

The production of olive oil is nearing its conclusion, with minimal harvests contributing to the total yields for the 2024/25 crop year. In April, 3,582 tons of fresh olive oil were collected, bringing this year's total to 1,410,494 tons. As of April 30, total stocks reached 881,758 tons, with packers holding 205,465 tons for their needs. Meanwhile, producers and farmers are storing 666,458 tons in mills, creating a significant imbalance in the market.

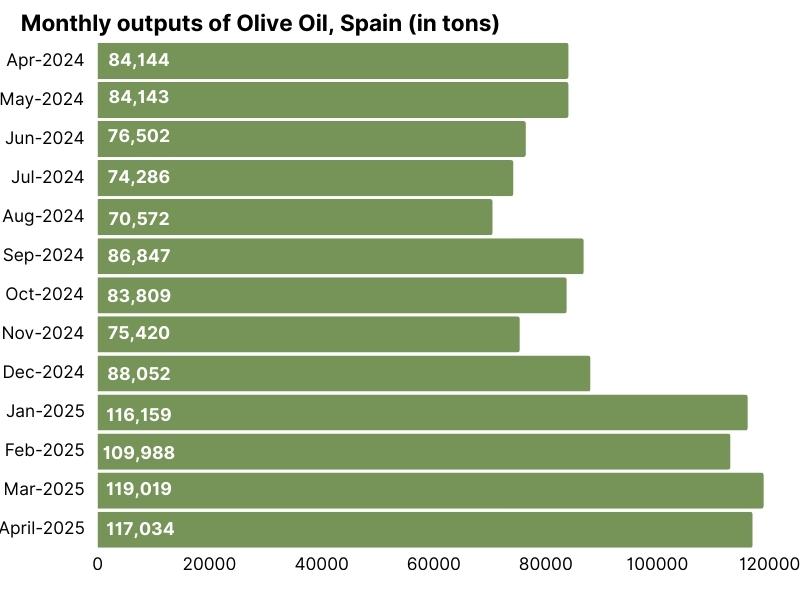

In April, the Spanish market maintained strong output levels, reaching 117,034 tons. This high volume has pushed the current average for 2025 to 115,550 tons. This trend indicates strong demand, fueled by lower prices both domestically and for exports. It is crucial for the market to adapt to these figures.

Our view

Our experts report that the current crop has surpassed 1.4 million tons, with favorable conditions expected for flowering, suggesting a potentially strong outlook for the next harvest. With this in mind, attention is shifting toward the 2025/26 carryover.

Production continues its steady recovery, with outputs on track to reach 120,000 tons. However, the outlook is divided between producers and packers, particularly with stock levels currently at 880,000 tons.

Market Perspectives

- Producers remain optimistic, believing the positive output trend will continue. With 5–6 months remaining until the next crop, they argue the carryover could end up being tight, potentially creating upward pressure on prices.

- Packers, on the other hand, anticipate a slower pace in outputs, which could lead to a larger carryover and reduce tension in the market.

Geographically, stock concentration in Andalusia—especially in the Jaén area—suggests sellers there may show greater willingness to release product, possibly leading to more varied pricing across regions.

Product Segments Overview

- High-quality Extra Virgin Olive Oil (Gold Standard) remains scarce. This limited availability is likely to support prices, keeping them firm and possibly pushing them back toward the €4.00/kg level, with a strong floor at €3.80/kg.

- Standard quality EVOO is expected to hold steady in the short term. However, this category may face a gradual decline in price as volumes are cleared.

- Lampante oils are showing signs of recovery, and the price of one ton is anticipated to increase by €100–€150.

- Refined Pomace oil is expected to remain stable, trading between €2.15 and €2.20/kg.

International Context

Turkey’s Market Dynamics

In Turkey, the olive oil sector has seen a remarkable turnaround in the 2024/25 season, with production expected to reach a record 475,000 tons. This figure includes about 100,000 tons of carry-over stocks, bringing the total available supply close to half a million tons. The Turkish government responded to this surplus by lifting the export ban on bulk olive oil in late 2024. Previously, this ban had restricted exports and led to a buildup of unsold stock. With the restrictions now eased, the sector is targeting $1 billion in olive oil exports for the season.

As a result of the increased supply and renewed export activity, domestic olive oil prices have started to fall noticeably. Average retail prices have dropped from €9 per liter to €7 per liter in spring 2025, and further declines toward €5 per liter are expected as the market continues to absorb the large harvest. While specific government-published export price data for May 2025 is not available, industry sources confirm that Turkish olive oil is being offered at highly competitive rates on international markets, often undercutting Spanish bulk prices by €0.50 to €1.00 per kilogram.

Tunisia: Production Challenges and Market Position

Tunisia’s olive oil sector has also experienced a strong recovery. According to the Tunisian Ministry of Agriculture, production for the 2024/25 season is projected at 340,000 tons, representing a 55% increase over the previous year. The National Olive Oil Office (ONH), which oversees much of the country’s olive oil export process, has provided clear pricing data and policy guidance.

Retail prices for olive oil in Tunisia were forecasted by the Ministry to range between 18 and 22 Tunisian dinars per liter (approximately €5.5–€6.6 per liter) for the 2024/25 season. However, by early 2025, wholesale prices had already fallen to between 14 and 18 dinars per liter (€4.1–€5.6 per liter), reflecting a 54.9% year-on-year drop due to the bumper harvest and global price corrections.

To support local consumption, some olive oil was subsidized and sold at 12 dinars per liter (about €3.34 per liter). On the export side, Tunisia’s prices have remained slightly below European levels to maintain competitiveness. The ONH has occasionally intervened in the market by purchasing and storing olive oil to stabilize farmgate prices.

Main Developments in Greece

The market is currently stagnant, with prices declining in April compared to March, yet remaining stable overall. Mills are stocked with a substantial amount of high-quality Extra Virgin Olive Oil (EVOO), but producers are dissatisfied with the prices they can fetch. The strategy among many Greek producers appears to be holding out for price increases during the summer months and just before the next harvest.

Currently, good quality EVOO is priced between €4.20 and €4.50 per kilogram. Many Greek buyers prefer to purchase Greek olive oil over Spanish options, despite the price difference, due to its superior quality.

As the market anticipates a strong crop next year, prices may continue to drop. Many producers are beginning to realize that prices are unlikely to rise soon and are starting to sell off their stock.

Market Outlook and Conclusion

April 2025 marked a period of stabilization for the olive oil market, with production recoveries in Spain and Greece helping to ease the supply pressure seen in previous years. However, Italy’s continued struggles and the scarcity of high-quality EVOO are maintaining price floors in premium segments. The market is now focused on the flowering phase, with stable weather conditions seen as crucial for a successful 2025/26 harvest.

Looking ahead, the balance between strong consumption, significant stock levels, and regional production disparities will determine price trends and market stability. While the overall outlook is optimistic, ongoing climate risks and trade uncertainties-especially regarding U.S. tariffs-remain key factors to watch. The Mediterranean olive oil sector appears resilient, but stakeholders must remain agile as the market continues to evolve.

Sources

La Agencia de Información y Control Alimentarios (AICA)

Turkish Ministry of Agriculture and Forestry

National Olive Oil Office (ONH)

Tunisia’s Ministry of Agriculture

")