")

EUROPEAN OLIVE OIL MARKET REPORT - MAY 2025

The Mediterranean olive oil market in 2025 is navigating a period of transition, marked by a recovery in production following years of drought and volatility, as well as shifting dynamics in pricing, quality, and international trade. Improved weather conditions, particularly in Spain, have led to a rebound in output and healthier reservoir levels, while other major producers such as Greece, Italy, Tunisia, Turkey, Morocco, and Portugal are each contending with their own unique challenges and opportunities, from fluctuating harvests and price pressures to evolving export strategies and government interventions. As the sector adapts to these changes, the distinction between standard and premium extra virgin olive oils remains noticeable, with high-quality oils maintaining strong prices and demand, while standard grades face downward pressure amid increased stocks and heightened competition. This evolving landscape underscores the importance of agility and strategic planning for producers and exporters as they respond to both local and global market forces in the year ahead.

Stay up-to-date with our weekly olive oil digest

Spanish Market developments

Weather Conditions

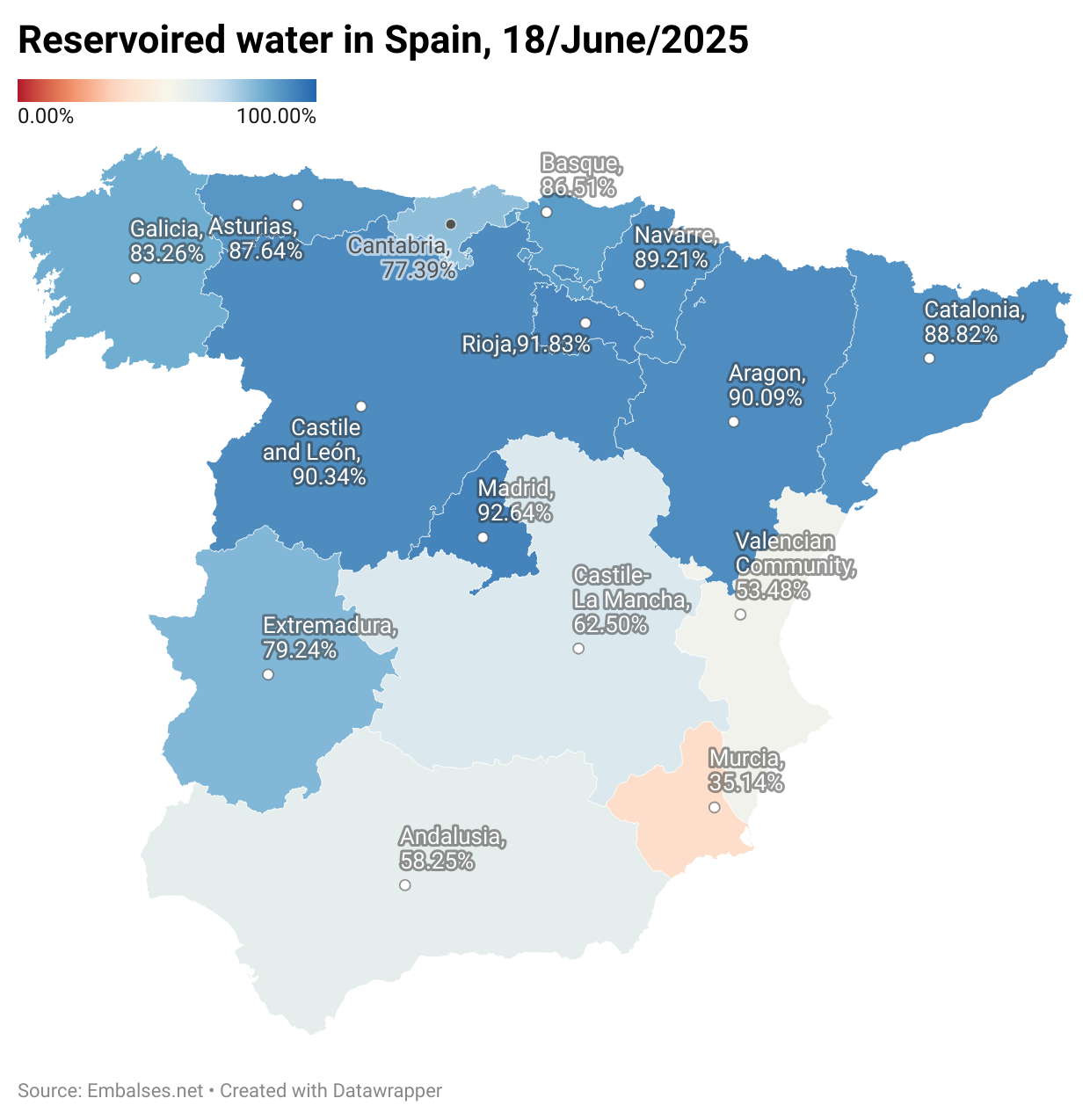

Following the beneficial rains in March and April, water reservoirs are significantly fuller this year compared to the drought conditions of the past two years. While current water levels may not guarantee a successful harvest in October, they do ensure that olive groves, which suffered in previous years, will have adequate irrigation this summer.

In the primary olive-producing region of Andalucia, water levels have reached 58.25%, reflecting a decrease of 4.91%. By late June, olive groves typically enter the pit-hardening stage, where the fruit has grown to about 50–90% of its final size and the stone begins to solidify. This stage is crucial as it marks the start of oil accumulation in the olive flesh. However, the region is also facing extreme heat, with daytime temperatures often exceeding 38–40 °C and dry conditions prevailing. This combination of intense weather and physiological development requires careful management.

During this critical period, moderate temperatures (ideally between 30–35 °C), controlled irrigation, and dry, well-ventilated conditions are essential. These factors promote healthy fruit growth, effective pit hardening, and the early onset of oil production while reducing the risk of disease. However, excessive heat and water stress can disrupt this balance. Prolonged high temperatures can hinder oil formation, cause sunburn damage, or even lead to fruit drop. Water stress is particularly concerning, as it may halt oil accumulation or cause the tree to abort developing fruit.

Another significant concern at this stage is the olive fruit fly, which targets green fruit. Warmer temperatures accelerate its life cycle, making monitoring and early intervention crucial. A sudden shift from heat to rainfall can further heighten the risk of fruit fly infestations and fungal issues like anthracnose.

Outputs

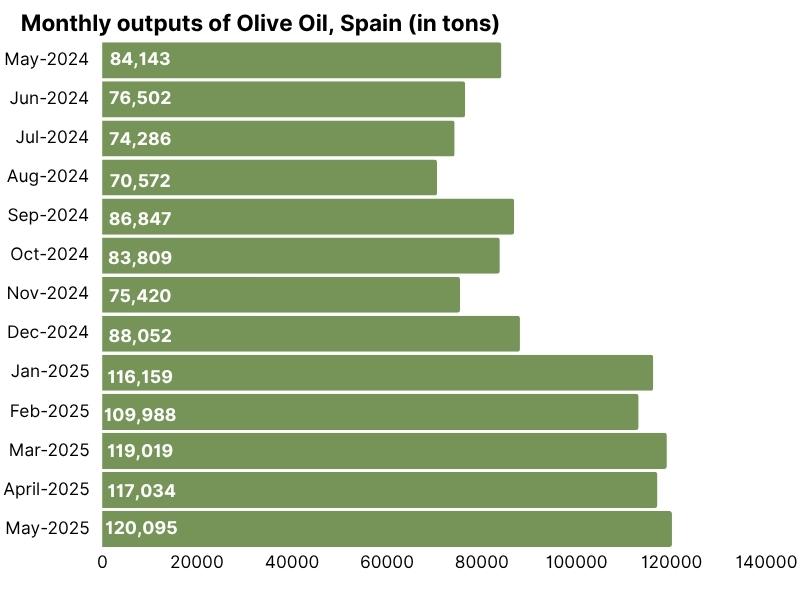

Olive oil production for the 2024/25 crop season has officially concluded, with May contributing an additional 971 tons to Spain's total production of 1,414,124 tons. As of May 31, total stocks, including carryover, reached 763,311 tons, with producers holding 555,574 tons and packers holding 220,609 tons. Output volume remains robust, exceeding 120,000 tons at 120,095 tons.

The average annual output in Spain has shown significant fluctuations from 2022 to 2025. In 2023, production fell sharply to just 68,627 tons, a 44% decrease from 2022, primarily due to severe drought conditions. In 2024, there was a partial recovery, but production levels still lagged behind the 2022 benchmark. By 2025, production rebounded strongly to 116,477 tons, approaching pre-crisis levels. This recovery suggests improved climatic conditions and possibly strategic changes in cultivation and irrigation practices, which have spurred strong purchasing activity.

Greek Olive Oil Market Developments

The Greek olive oil market in mid-2025 is characterized by stabilization after a period of price declines, with extra virgin olive oil (EVOO) prices settling around €3.90–€4.20/kg, depending on the region and quality. Producers in both the Peloponnese and Crete are reluctant to sell at current rates, hoping for better offers, but market realities and the need to liquidate stocks for financial obligations are pushing them toward sales at prevailing prices. The market remains challenging, as buyers—especially from Italy—are hesitant to purchase Greek oil due to its price parity with Spanish organic EVOO and concerns over quality, which has been generally assessed as standard or low in recent panel tests. Despite these hurdles, domestic trading is active, and there is cautious optimism for a slight price increase if demand picks up, though the window for such gains may be closing as the season advances.

Looking ahead, Greece is showing positive signs for the 2025/26 harvest, with orchards in the Peloponnese exhibiting 15–20% more flowering nodes than the previous year, suggesting a potentially strong crop. However, the sector faces ongoing pressure to clear inventories before the new harvest arrives, and the broader Mediterranean market is highly competitive, with Tunisia and Turkey also offering aggressive pricing3. Export dynamics are shifting, and Greek producers are advised to secure forward contracts and diversify their commercial strategies, especially as global consumption is projected to rise and EU stocks are expected to recover by the end of the 2024/25 season. While the market outlook is cautiously optimistic, producers must remain agile in response to evolving demand, quality expectations, and international competition.

Italy Olive Oil Market Update – May 2025

In May 2025, the Italian olive oil market experienced continued price resilience, with extra virgin olive oil producer prices in Bari averaging €970 per 100 kg, reflecting a slight 0.5% increase from the previous month and standing in stark contrast to the sharp declines seen in Spain and Greece. Despite a broader European trend of price drops due to improved weather and production outlooks, Italy’s limited stock levels and lower production kept prices elevated, especially for high-quality oils, which remain scarce and command a premium. The country’s overall production for the 2024/25 season is projected to be significantly lower than the previous year, primarily due to prolonged drought and adverse weather in southern regions, with estimates ranging from 215,000 to 235,000 tons—down over 30% from last season—raising concerns about Italy’s ranking among global producers. While demand remains stable and exports are robust, the market is marked by uncertainty, as producers face pressure from high costs and limited supply, and buyers monitor the potential impact of international trade policies and future harvest prospects.

Olive Oil Market Update – May 2025: Other Mediterranean Countries

Tunisia saw a strong production recovery, with output projected at 340,000 tons—a 55% increase over the previous year—leading to a sharp drop in wholesale prices to €4.1–€5.6 per liter and a surge in export volumes, even as export values declined due to global price corrections and increased competition. Turkey achieved a record harvest, with production expected to reach 475,000 tons, and responded by lifting its export ban on bulk olive oil, resulting in falling domestic prices (from €9 to €7 per liter, with further declines expected) and highly competitive export offers that often undercut Spanish prices by €0.50–€1.00 per kilogram.

Morocco, in contrast, faced its third consecutive year of declining harvests due to drought, with production forecast to drop to 90,000 tons—well below its five-year average—prompting the government to suspend import duties and import olive oil to meet domestic demand, while local prices continued to rise. Portugal benefited from improved weather and is projected to produce 190,000–210,000 tons, with prices stabilizing around €5.80 per kilogram, reflecting the broader Mediterranean trend of increased supply and easing prices, though high-quality oils remain scarce and command a premium.

Our view

The latest AICA data confirms that the olive oil sector has entered a clear recovery phase. With the 2024/25 crop surpassing 1.4 million tons, and flowering results from recent weeks indicating strong potential for the upcoming harvest, attention is now shifting toward the carryover into the 2025/26 campaign. The key question: how much oil will remain available by the time mills begin crushing again in the fall.

Monthly output figures reinforce this positive trend. For the first time since the crisis years, monthly production has exceeded 120,000 tons, marking a symbolic and practical milestone in the recovery process. The momentum suggests not only stabilized production, but also renewed market confidence, underpinned by strong stocks and robust commercial activity both domestically and in export markets.

From a price perspective, the segmentation between standard and high-quality EVOO remains highlighted. Premium extra virgin oils are expected to hold their value, with prices unlikely to drop below €3.80–3.90/kg, though the psychological threshold of €4 now appears firmly in the past. It is increasingly clear that the market is recalibrating, and €4/kg for bulk EVOO is no longer a viable reference, at least not in the foreseeable future.

In contrast, the standard quality market is showing short-term tension, driven by producers' efforts to reclaim a few euro cents and defend pricing. This defensive posture is particularly visible in areas like Jaén, where higher stock levels may soon exert downward pressure on local suppliers, possibly translating into commercial activity boosts over the summer.

Meanwhile, pomace oil continues to remain stable, trading around €2.15–2.20/kg (refined), and lampante oil is projected to stay within the €2.70–2.80/kg range. While these segments are less volatile, they are influenced by the broader availability of lower-grade oils, especially in a context of improved total output.

Packers' behavior is also evolving. Spanish packers currently enjoy better stock positions than their Italian counterparts, a factor that may tilt short-term market influence toward Spain. However, Italian packers are expected to become more active over the next three months, potentially introducing new dynamics, especially in markets sensitive to quality and origin.

Greece also remains an important piece of the puzzle, holding significant volumes of higher-quality oils. However, unlike some Spanish producers, Greek suppliers are under less commercial pressure to release stock, and are likely to hold firm, especially given sustained demand for quality oil over the summer months.

Lastly, reservoir levels across key growing regions are healthy, securing irrigation throughout the dry season. This removes a major source of uncertainty that has weighed heavily on the market in previous years, and further supports the thesis of a market stabilizing both structurally and psychologically.

Price Trends and Market Correction

The price correction that began in early 2025 has continued through May, with producer prices for extra virgin olive oil showing significant year-on-year decreases in most producing countries. According to International Olive Council data from the first week of May 2025, producer prices in Jaén (Spain) stood at €3.55/kg, marking a substantial 53% decrease compared to the same period last year. Similarly, prices in Chania (Greece) fell to €3.90/kg, representing a 46% decline year-on-year. Italy remains the exception, with Bari prices holding steady at €9.70/kg, showing a marginal 0.5% increase compared to May 2024.

The European Commission's Harmonised Index of Consumer Prices (HICP) for olive oil in the EU-27 reflected this downward trend, falling by 13.9% in February 2025 compared to the previous year, continuing the decline that began in April 2024. This price normalization is gradually influencing consumer behavior, with market analysts noting a return to olive oil consumption after many households had switched to cheaper alternatives during the recent price spikes. The European Commission's price monitoring data, updated on June 17, 2025, provides comprehensive evidence of this market correction, though the segmentation between standard and premium extra virgin olive oils remains very noticeable.

Future Outlook and Market Projections

Looking ahead, the outlook for the 2025/26 harvest is cautiously optimistic. Olive groves in the Peloponnese (Greece) are exhibiting 15–20% more flowering nodes than the previous year, suggesting a potentially strong crop for the next season. However, the sector faces ongoing pressure to clear inventories before the new harvest arrives, and the broader Mediterranean market remains highly competitive, with Tunisia and Turkey also offering aggressive pricing.

The European Commission's medium-term agricultural forecast suggests that olive oil production and consumption will face challenges in the coming decade due to climate change impacts on water availability and soil productivity. These changes are "limiting the potential for yield growth and causing a northward shift in agro-climatic zones, which affects cropping patterns, including olive oil," and these trends are expected to intensify.

The future profitability of the EU olive oil sector will depend on the successful transformation of production systems, particularly the shift from extensive orchards to intensive and highly mechanized plantations. Investments in plantations in Spain and Portugal are expected to contribute to average annual production growth of around 1.2% in Spain and 1% in Portugal over the next decade, while Italy and Greece may face challenges due to the gradual reduction of olive land.

The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions.Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

Stay updated on the olive oil market

Sources:

La Agencia de Información y Control Alimentarios (AICA)

Turkish Ministry of Agriculture and Forestry

National Olive Oil Office (ONH)

Tunisia’s Ministry of Agriculture

International Olive Oil Council

European Commision

Buy Olive Oil in Bulk - Olive Oil Bulk Purchase

")