")

Weekly Olive Oil Market Updates

The global olive oil market is undergoing significant shifts as the 2024/25 campaign unfolds. In Spain, a remarkable bloom among olive trees has raised expectations for a robust upcoming harvest, setting the stage for changes in both supply and pricing dynamics. Across the Mediterranean, producers and buyers are closely monitoring developments, with price corrections, quality concerns, and regulatory debates shaping the market landscape. As production rebounds in key regions and international trade picks up pace, stakeholders are navigating a complex environment marked by evolving consumer demand, inventory pressures, and new food safety standards.

Production and Supply:

According to the latest data from the European Commission and the International Olive Council (IOC), the 2024/25 olive oil campaign in the EU is marked by a significant production recovery. Spain, the bloc’s leading producer, is expected to reach approximately 1.42 million tonnes, a 51% increase from the previous season. Greece and Portugal are also seeing strong rebounds, while Italy is forecast to see a decline in output compared to last year. Overall, EU production is estimated at just over 2.1 million tonnes for the current campaign.

Price Developments:

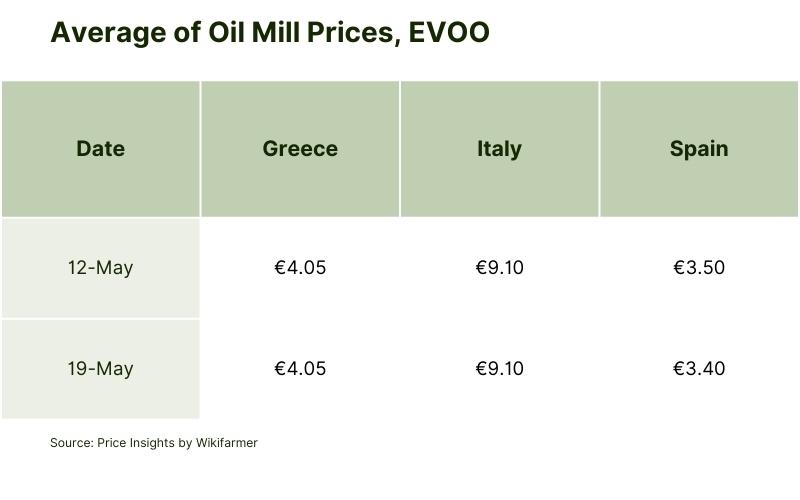

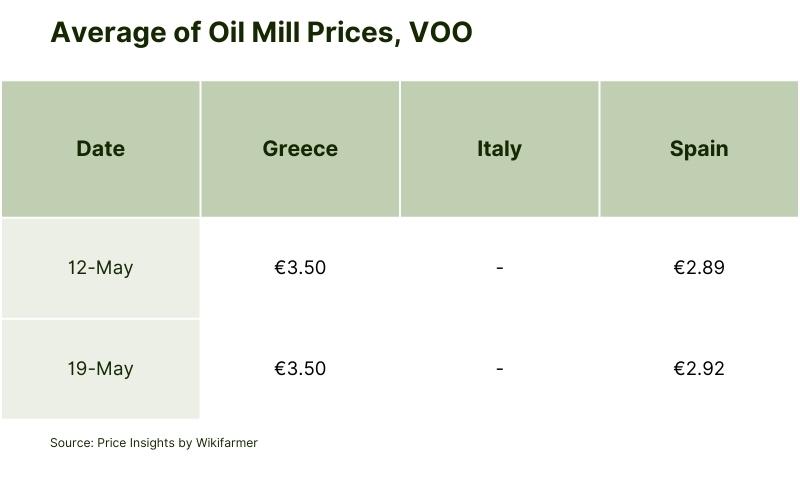

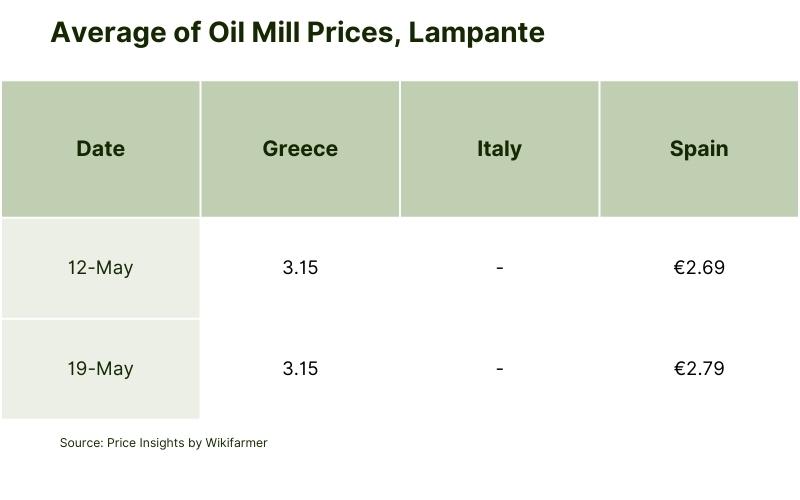

Producer prices for extra virgin olive oil have sharply corrected from the historic highs of 2023 and early 2024. As of the first week of May 2025, official IOC statistics report:

- Jaén, Spain: €3.55/kg (down 53% year-on-year)

- Bari, Italy: €9.70/kg (up 0.5% year-on-year)

- Chania, Greece: €3.90/kg (down 46% year-on-year)

The European Commission’s price monitoring confirms this trend, with prices in Spain and Greece falling substantially, while Italy remains at a premium due to ongoing supply constraints.

Trade and Demand:

EU olive oil exports have rebounded, with extra-EU shipments rising by over 20% year-on-year in February 2025. The United States, the EU’s largest export market, saw import volumes from the EU rise by 34% in February compared to the previous month, and by 7% over the first five months of the 2024/25 crop year. However, the unit value of EU olive oil exports continues to decline, reflecting the normalization of prices after the previous year’s peaks.

Consumer Prices and Stocks:

Retail prices for olive oil in the EU have started to ease, with the Harmonised Index of Consumer Prices (HICP) for olive oil dropping by 13.9% in February 2025 compared to the previous year. Despite the production recovery, stocks are expected to remain below the five-year average by the end of the campaign, at an estimated 460,000 tonnes.

Our view

Our experts in Spain have observed a remarkable bloom among olive trees, with branches bending under the weight of abundant flowers. This development bodes well for the upcoming harvest and raises expectations for market trends.

Last week, the release of AICA data led to a slight recovery in prices. While Extra Virgin Olive Oil is available, the quality remains an issue, with many oils barely passing official panel tests. Spanish and Italian buyers are closely monitoring the market as prices begin to rise, but they are currently purchasing only what they need. Despite this uptick, prices are expected to drop again: the promising outlook for the next harvest, combined with large unsold quantities at mills and producers, will likely create pressure to clear inventory. Furthermore, with the first official Spanish crop forecast expected at the end of May, there is widespread belief that prices will continue to decline.

In Greece, domestic trading is active, with prices generally stable around €4–€4.20 per kilogram for good quality Extra Virgin Olive Oil in the Peloponnese. There is a possibility of slight price increases due to demand. In Crete, producers and mills are experiencing price declines but are reluctant to accept rates below €4 per kilogram, insisting on higher prices. The lack of competition in the current market allows them to maintain these rates. Italian buyers are holding off on purchasing olive oil from Greece, anticipating significant price drops. Additionally, the current quality of the offered olive oil is low, leading buyers to consider purchases only for specific needs.

Regulatory and Quality Landscape

Spain is currently at the forefront of the EU debate on setting stricter limits for mineral oil hydrocarbons (MOSH and MOAH) in olive oil and olive-pomace oil. These proposed regulations, driven by EU authorities, would impose progressively tighter thresholds for these contaminants over the next several years. Spain has found itself largely alone in advocating for a delay, citing concerns that regulatory action is outpacing scientific consensus and could have significant economic repercussions for the sector. Other major producers, such as Italy and Greece, have not opposed the new measures as actively.

This regulatory uncertainty is creating tension within the Spanish olive oil sector, with industry representatives urging the government to defend a more cautious approach. The debate highlights the broader challenge of balancing food safety, scientific evidence, and the economic health of the olive oil industry. Meanwhile, technological innovation and quality control remain priorities, as demonstrated by recent industry gatherings focused on improving analytical methods and traceability.

Conclusion

The outlook for the olive oil market in late May 2025 is defined by a strong production recovery in Spain and Greece, leading to a notable decline in producer prices after last year’s historic highs. While exports, particularly to the United States, are on the rise and retail prices are beginning to stabilize, lingering stock shortages and regulatory uncertainties continue to influence market sentiment. As the sector adapts to new quality and safety requirements, the balance between supply, demand, and policy will remain central to shaping future trends in the global olive oil industry.

Sources:

International Olive Council: Olive Sector Statistics – April/May 2025

Spanish Ministry of Agriculture, Fisheries and Food

Buy Olive Oil in Bulk - Olive Oil Bulk Purchase

Olive Oil PET - Olive Oil Bottles

Olive Oil Retailers - Olive Oil in Bottle

The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions.Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")