")

How trade dynamics, key species, and quality oils shape one of the world's most resilient seafood sectors

The canned fish sector is a significant segment of the global seafood industry, providing consumers worldwide with affordable protein that has a long shelf life. Canned fish (from tuna and sardines to mackerel and anchovies) accounts for roughly 10% of the global fish trade by volume. In 2023, international trade in prepared or preserved fish products reached about 3.2 million tonnes valued at USD 17.5 billion, a share that has held steady in recent years. Demand even spiked during the COVID-19 pandemic, as consumers stocked up on non-perishable seafood for food security.

.png)

Market size and growth trajectory

The canned seafood market has demonstrated consistent expansion over the past decade, driven by rising global demand for convenient, protein-rich food products and increasing health consciousness among consumers. In 2024, the global market generated revenues ranging from $30.46 billion to $32.7 billion, with projections indicating growth to $31.78 billion to $36.1 billion in 2025. Market forecasts through 2033 anticipate the industry reaching $51.1 billion, supported by demographic shifts, urbanisation, and evolving dietary preferences.

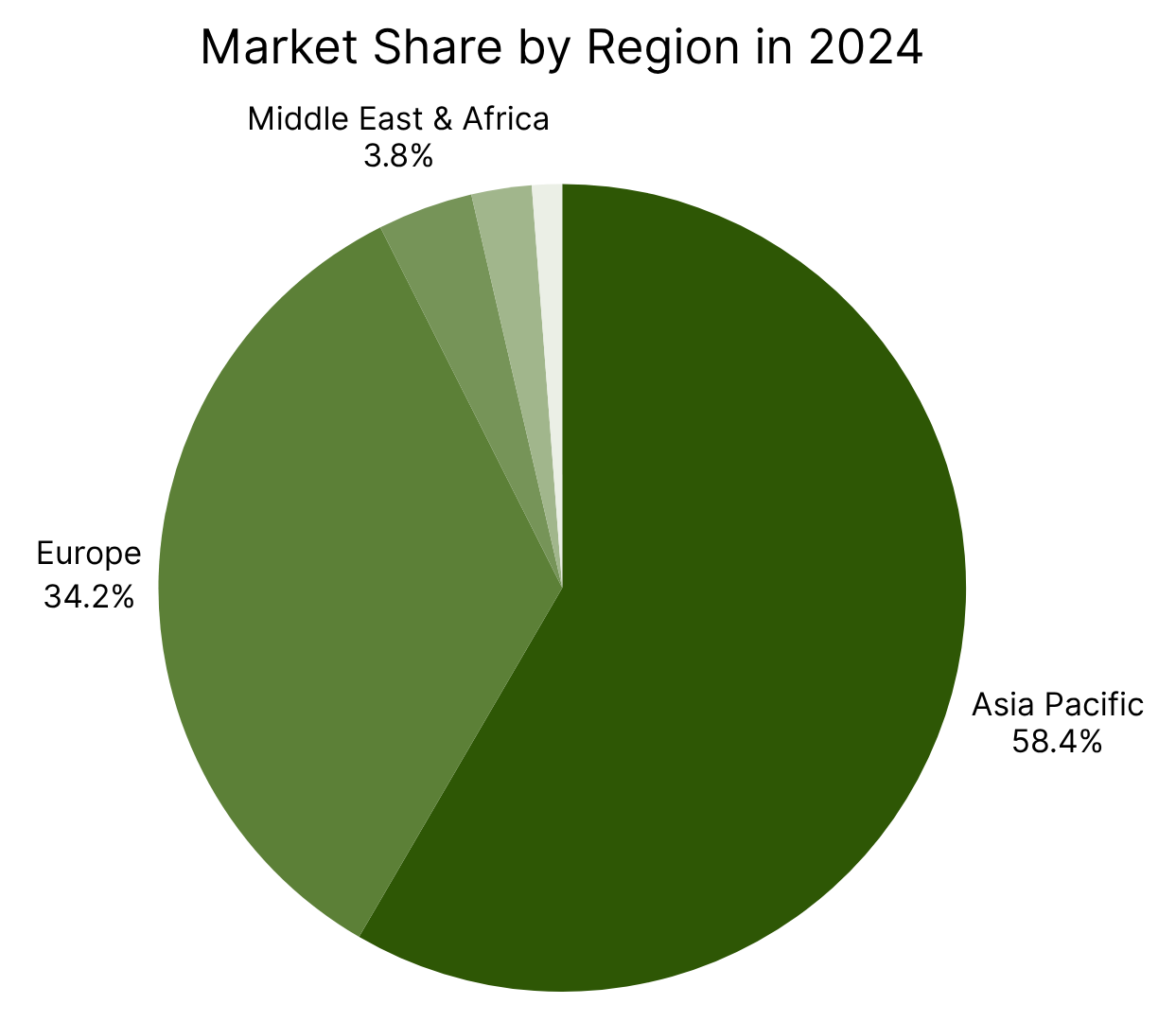

Asia Pacific dominates the global landscape, commanding a 58.6% market share in 2024, underpinned by high per-capita seafood consumption, robust production infrastructure, and expanding middle-class populations across China, Japan, Thailand, and other Southeast Asian nations. The region is expected to maintain its leadership position with a projected compound annual growth rate of 4% through 2030, reaching $15.99 billion.

Europe represents the second-largest market, accounting for approximately 34% of global canned tuna revenues. The European Union serves as both a major consumption centre and processing hub, importing over 9.5 million tonnes of seafood annually in live weight equivalent. European consumption patterns reflect mature market dynamics, with growth rates moderating as consumer preferences shift toward premium, sustainably sourced products.

Emerging markets in the Middle East, Africa, and Latin America present significant growth opportunities. The Middle East and Africa canned seafood market is valued at $3.20 billion in 2025 and is forecast to reach $4.45 billion by 2030, driven by urbanisation, rising disposable incomes, and increasing acceptance of shelf-stable protein sources in regions with limited cold-chain infrastructure.

Major producers & exporters

The global market for canned fish is broad, but a few countries dominate production and exports.

Thailand

Thailand remains the largest exporter of canned tuna, the most traded canned fish product globally. In 2024, Thai fishery exports reached a 10-year high of about $659 million, up 13.7% from 2023. Canned tuna shipments climbed 32% year-on-year to 548,653 tonnes, with export values rising 34% to approximately $2.25 billion.

Thailand's dominance rests on its advanced processing infrastructure and strategic location near the Western and Central Pacific Ocean, one of the world’s richest tuna-fishing areas. The country imports large volumes of raw tuna for processing and re-export, supported by a mature logistics network and competitive labour costs.

The United States remains Thailand's largest customer, importing around 271,000 tonnes in 2024, a 25% increase from the previous year. This is followed by China, Japan, and ASEAN partners, which together absorbed over 318,000 tonnes.

Ecuador

Ecuador ranks as the second-largest exporter of canned tuna, accounting for approximately 5.4% of the global market share. In 2024, Ecuador's canned and processed tuna exports expanded strongly, reaching an estimated $1.1 billion.

China

China has become the largest exporter of canned and prepared fish by volume, representing 22–26% of global exports in 2023. The country exported 1.2–1.5 million tonnes of processed fish products worth roughly $7.5 billion, reflecting vast processing capacity, integrated supply chains, and competitive labour costs.

Spain

Spain leads Europe's canned seafood production, with 343,000 tonnes processed annually and an industry value exceeding $1.6 billion. About 43% of production is exported, mainly to other EU member states.

Tuna accounts for over 80% of Spain's canned fish exports by value, consolidating the country's role as a continental processing hub. Spanish canneries rely heavily on imported raw materials, including tuna from Ecuador, sardines and anchovies from Morocco, mackerel from Portugal, and salted anchovies from Argentina, which enables them to maintain a steady output despite EU fishing quota constraints.

Morocco

Morocco has secured a global leadership position in canned sardines, exporting more than 152,000 tonnes in 2022 worth over $540 million. The country also ranks first in world trade for semi-preserved anchovies, thanks to rich pelagic fisheries along its Atlantic coast and a strong processing base in Agadir and Safi.

Approximately 91% of Europe's imported canned sardines from outside the EU originate in Morocco, underlining its importance for European supply chains. Moroccan exporters have also expanded to sub-Saharan Africa and the Middle East, building a diverse customer base for small pelagic fish products.

Top fish species for canning

A handful of fish species dominate the world's canned seafood market.

Tuna remains the undisputed leader, accounting for about 45–50% of global canned seafood sales. The most commonly canned varieties are skipjack (Katsuwonus pelamis), yellowfin (Thunnus albacares), and albacore (Thunnus alalunga). Skipjack is the main source of "light tuna," while albacore is marketed as "white tuna," preferred in premium segments. Tuna's mild flavour, high protein content, and convenient format make it a staple in North America, Europe, and Asia. In the European Union, canned tuna has consistently ranked as the most widely consumed seafood product by volume, surpassing fresh cod and salmon.

Following tuna, small pelagic fish form the backbone of the canning industry. Sardines (Sardina pilchardus) are among the oldest and most widely canned fish, often preserved in tomato sauce, oil, or brine. They are especially important in Morocco, Portugal, and the Philippines, where abundant stocks and strong consumer demand support major processing industries. Sardines are celebrated not only for their affordability but also for their high levels of omega-3 fatty acids and calcium from edible bones.

Mackerel (Scomber spp.) is another key species, particularly in Europe, West Africa, and East Asia. Canned mackerel is valued for its rich flavour and nutritional content, often featured in spiced or smoked variants.

Anchovies (Engraulis spp.) occupy a smaller but distinctive niche, especially in Mediterranean cuisine. Typically sold as fillets preserved in oil or salt, they are used more as a flavouring ingredient than as a primary source of protein, yet they represent an essential export for Morocco, Spain, and Peru.

Salmon (Oncorhynchus spp.), particularly pink and sockeye, also maintains a loyal consumer base, with established canning industries in Alaska, Canada, and Chile. Although the fresh and frozen salmon trade has surpassed canned salmon in volume, the latter remains popular in markets like the United States and the United Kingdom due to its convenience and long shelf life.

Global imports by species

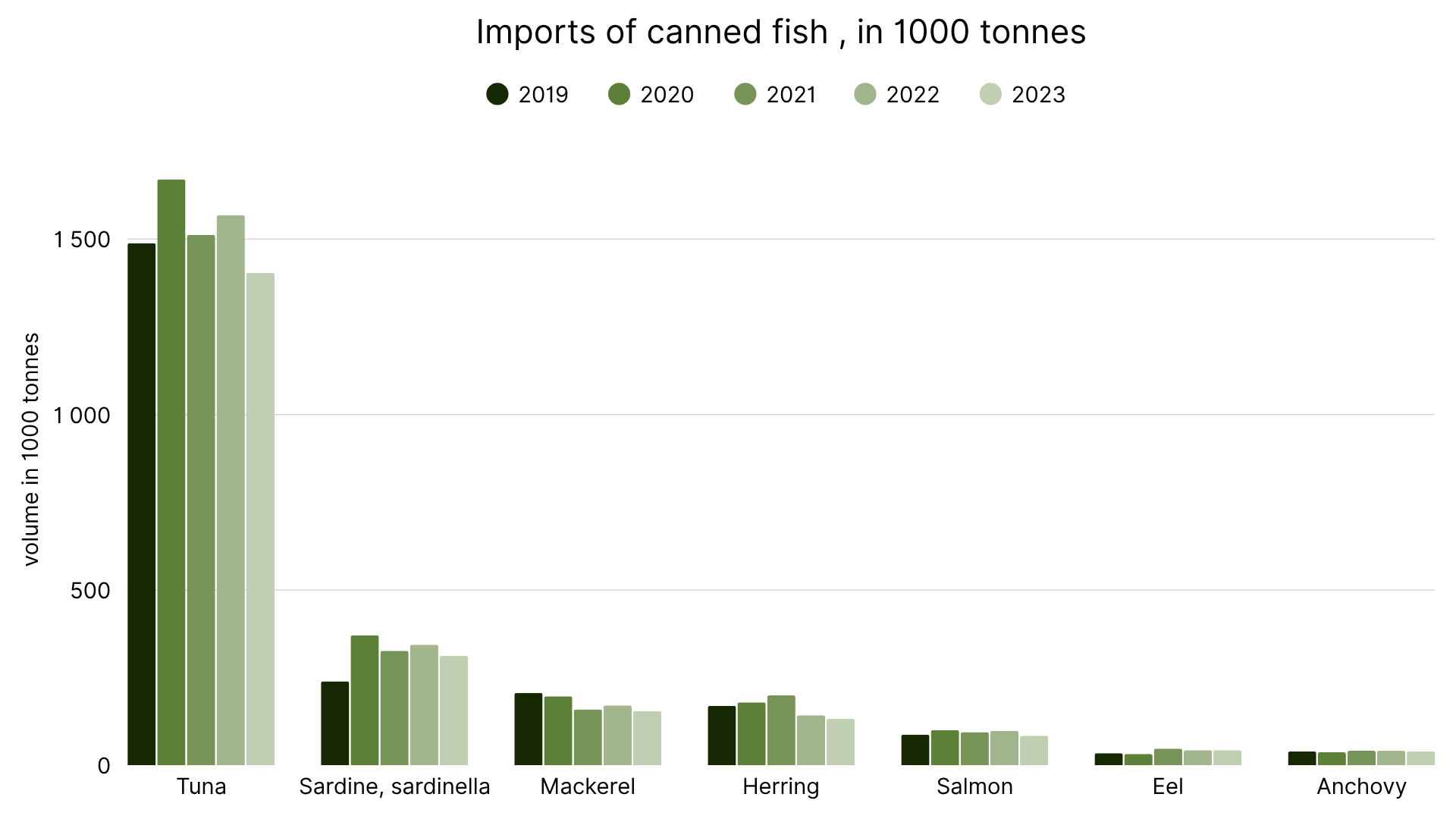

Tuna dominates global canned and prepared fish imports, representing more than 60% of total traded volumes in recent years. In 2023, global imports of canned and prepared tuna reached 1.4 million tonnes, far surpassing other species such as sardines (313,000 tonnes), mackerel (155,000 tonnes), herring (133,000 tonnes), and salmon (85,000 tonnes).

Major consumer markets

Global canned fish consumption is concentrated in a few major regions, accounting for most of the global demand.

United States

The U.S. is the world's largest single market for canned seafood, especially tuna. Despite modest per capita consumption (1.2–1.6 kg per year), the country's large population drives enormous demand.

In 2024, U.S. imports of canned and prepared tuna reached approximately 230,000 tonnes, with an import value of $1.2 billion. Thailand is the leading supplier, followed by Ecuador, Vietnam, Indonesia, and the Philippines. American preferences are shifting from traditional chunk light tuna in oil or brine toward flavoured, low-sodium, and pouch-packed formats that emphasise convenience and nutrition.

European Union

The EU is the world's largest regional market for canned fish, with the highest per capita tuna consumption, around 2.78 kg per year. Spain, Italy, and Portugal have deep-rooted culinary traditions involving canned seafood, while northern Europe favours fresh or frozen fish.

EU imports of canned tuna exceed $1.8 billion annually, mainly from Ecuador, the Seychelles, and the Philippines. Strict EU rules on traceability, sustainability, and food safety drive demand for certified and premium products, helping compliant exporters secure better prices.

Japan & China

Japan ranks among the top seafood consumers globally, with a canned fish market worth approximately $2 billion. Canned mackerel (saba), tuna, and sardines are common, valued for convenience and compatibility with traditional meals.

China, meanwhile, is the largest seafood importer by volume and an emerging canned fish market, fueled by e-commerce growth. Chinese consumers increasingly favour smaller portion cans featuring tuna, sardines, and mackerel adapted to local tastes.

Emerging markets

The growing demand in Australia, Canada, the Middle East, and Latin America reflects the role of canned fish as an affordable, nutritious, and shelf-stable protein source. Saudi Arabia and Libya have become key importers of Thai tuna, while Southeast Asia shows strong domestic consumption growth.

Role of oils in the canned fish industry

One interesting aspect of the canned fish industry is the role of packing medium (especially edible oils) in product quality and marketing. Many canned fish products are packed in either brine (salt water) or vegetable oil. The choice of oil, typically olive oil or sunflower oil, and sometimes soybean or other oils, can significantly influence the flavour, texture, and consumer perception of the product.

If you're sourcing high-quality oils for seafood processing or product development, explore Wikifarmer's selection of industrial-grade olive oils and vegetable oils available for bulk purchase:

Vegetable oils for industrial use

Olive oil

In the premium segment, extra virgin olive oil (EVOO) is the preferred medium, especially among Mediterranean producers in Spain, Italy, and Portugal. Olive oil imparts a rich flavour that complements tuna, sardines, and anchovies while aligning with the region's culinary identity and the growing consumer focus on health and authenticity.

Scientific studies show that polyphenol-rich olive oils enhance the stability and nutritional quality of canned fish by inhibiting lipid oxidation during heat processing, helping preserve flavour and extend shelf life. This combination of taste, health benefits, and antioxidant protection makes olive oil-packed products stand out in premium categories.

In Europe, labels such as "en aceite de oliva" (in olive oil) are seen as a mark of quality and tradition, often commanding price premiums of 30–100% compared to water- or vegetable oil-packed alternatives.

Sunflower and other neutral oils

Sunflower oil is the most common alternative for standard or economy products. Its light flavour allows the natural taste of the fish to dominate, and its lower cost makes it ideal for high-volume, price-sensitive markets. Many Moroccan sardine exports, for example, are packed in sunflower oil for its neutral profile and reliable performance in canning.

In some markets, soybean and canola oils are also used, particularly in North America, where these oils are familiar and inexpensive. These products cater to consumers who seek practicality and everyday affordability, rather than gourmet appeal.

Market implications

The choice of packing medium is both a technical decision and a marketing signal.

As global demand diversifies, brands increasingly offer multiple variants: tuna in water for calorie-conscious consumers, tuna in sunflower oil for mainstream buyers, and tuna in olive oil for premium markets. This segmentation enables producers to reach different audiences without altering the core product, demonstrating how even the choice of oil can shape the identity and success of canned fish brands.

Conclusion

The canned fish industry connects oceans, producers, and consumers worldwide. Behind every tin lies a combination of fisheries management, processing expertise, and ingredient quality, including the choice of oil that defines flavour and market identity. As the sector continues to evolve toward sustainability and traceability, opportunities emerge for producers, traders, and food brands that invest in quality and innovation.

Sources

- International trade of canned and processed fish (HS 1604) in 2019-2023

- SpecTUNA: better quality and a more competitive tuna industry thanks to EU funding

- The European market potential for canned fish

- Governance of the circular economy in the canned fish industry: A case study from Spain

- Granger causality between the canning sector and the Spanish tuna fleet: Evidence from the Toda-Yamamoto approach

- Canned Seafood Market Size, Share & Industry Analysis, By Species

- New Perspectives on Canned Fish Quality and Safety on the Road to Sustainability

")