")

European Olive Oil Market Report - February 2025

Main Market Figures - Spain

February usually is the concluding month for fresh olive harvesting. However, the previous rainy weather has extended the harvesting procedures to continue in February, and AICA data are anticipated to show high volumes of fresh olive oil production. Below, we are conducting an in-depth analysis of the AICA report for the month of February, including expert commentary on the bulk olive oil market.

Weather Conditions

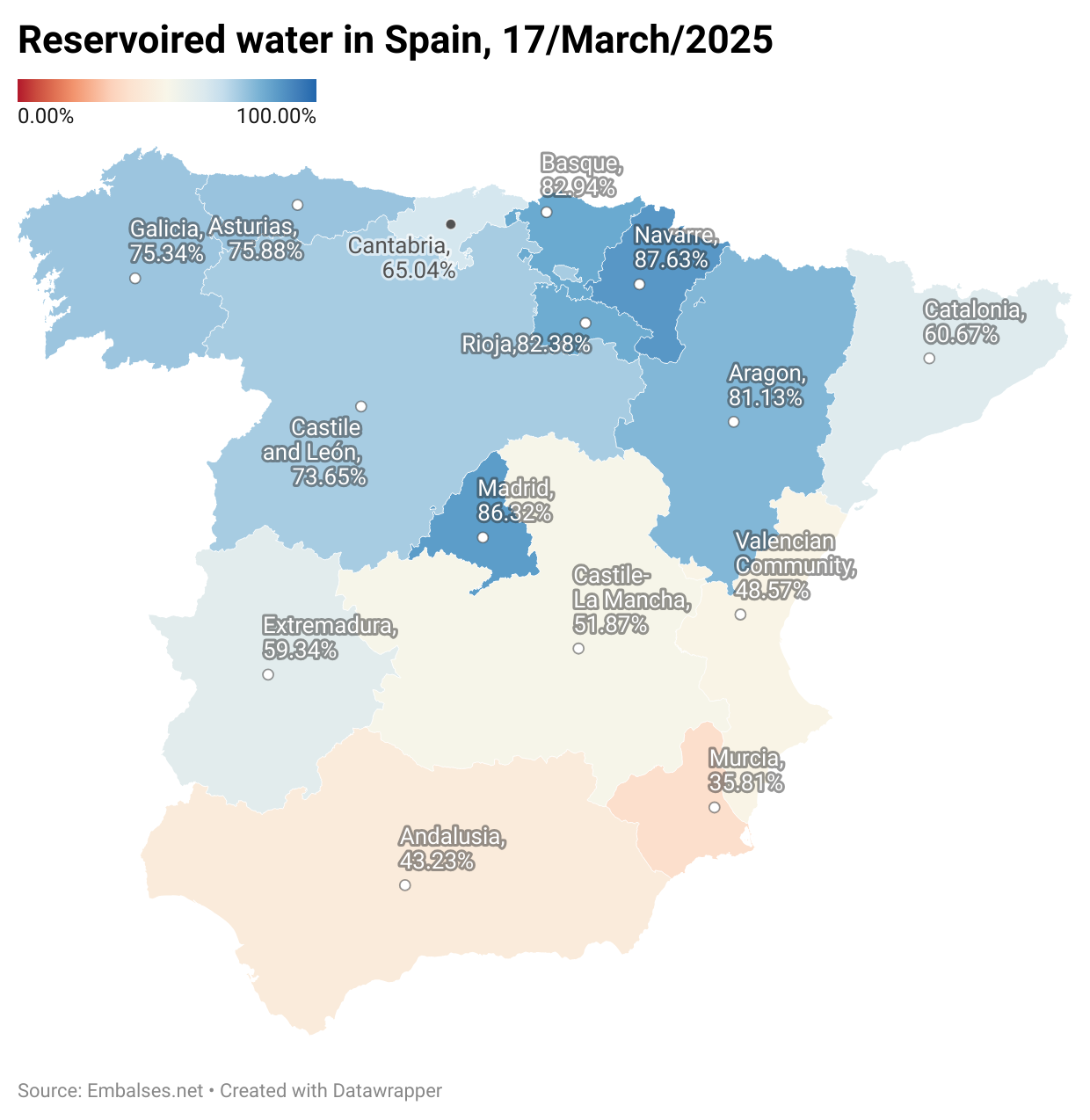

February brought substantial rainfall across Spain, a trend that has continued into early March. These rains have significantly improved water reservoir levels, creating favorable conditions for olive groves. As a result, the outlook for the upcoming growing season appears positive, with healthy tree development expected.

Crucially, the heavy rains have replenished reservoir levels, which had been critically low in recent years. In Andalusia, the heart of Spain’s olive oil production, reservoir levels rose from 38.91% to 43.23%, marking a significant improvement in water availability. This increase helps secure irrigation for the dry summer months, reducing the risk of water stress for olive trees.

Looking ahead, the next crucial period for olive trees will be the flowering stage in late April and May. If temperatures remain warm and stable, conditions could be optimal for a strong bloom, setting the stage for a potentially improved harvest. However, sudden heatwaves or unexpected cold spells could still impact production.

The current state of water reservoirs in Spain is showcased in detail in the following graph:

Outputs

As noted in our previous update, December saw intense harvesting activity, but persistent rainfall in January slowed this trend. Harvested volumes in January reached 341,490 tons, nearly halving compared to the previous month.

By the end of February, total 2024/25 crop production had reached 1,385,337 tons, with February’s harvest contributing 150,769 tons. Meanwhile, total stocks now stand at 1,100,113 tons, with packers holding 200,062 tons and farmers retaining 884,020 tons.

-2.jpg)

Market activity remained robust despite ongoing cautious purchasing. February outputs, which include both domestic consumption and exports, totaled 109,988 tons, slightly below January’s figure but still within strong trading levels. The 2025 average monthly output now stands at 113,073 tons, reinforcing a stable market despite initial price resistance and weather-related uncertainties.

Overall, while improved production levels and strong stock positions provide supply stability, weather conditions leading up to the flowering stage remain a key factor to monitor in the coming months.

Our View

This month has provided greater clarity on key aspects of the olive oil market. The 2024/25 crop is now expected to exceed 1.4 million tons, reflecting a notable recovery supported by favorable rainfall. At the same time, consumption has rebounded significantly, with monthly outputs stabilizing around 110,000 tons.

Farmers continue to hold over 80% of available stocks, as packers have largely purchased only what was necessary to meet immediate commitments. However, there is a gradual shift, with buyers increasingly willing to secure supply for longer periods.

In terms of pricing dynamics, high-quality Extra Virgin Olive Oil (EVOO) remains scarce in Spain, boosting demand for Greek EVOO, which continues to command a price premium. Meanwhile, refined olive oil prices are proving more elastic, adjusting downward at a faster pace than EVOO.

Looking at regional conditions, despite the overall improvement in production prospects, Jaén, Spain’s leading olive oil-producing area, remains a point of concern. Local farmers report that rainfall has been insufficient, and olive trees still show signs of stress from previous dry years.

For now, the market remains stable, with expectations holding steady until the crucial flowering period in late spring.

Main Developments in Greece

The Greek olive oil market remains firm, with prices stabilizing at high levels despite regional variations. Producers continue to show reluctance to sell at current offers, preferring to wait until Easter, a period that typically brings stronger demand. While some areas have seen slight price increases due to limited supply in mills, others experienced minor declines. However, following the latest AICA data release, prices have shown signs of stabilization. With the harvest nearing completion, market participants are closely monitoring price movements, as producers remain cautious about committing to sales below their targets.

Looking ahead, the post-harvest period and upcoming Easter season will be key in shaping price trends. Many producers are holding out for €5/kg or above, anticipating that reduced availability in the coming months could drive prices higher. However, buyer resistance may create a more cautious trading environment, preventing rapid price increases. Limited supply in mills, combined with strong producer confidence, suggests that the Greek market will remain firm but sensitive to shifts in demand and international price trends.

Powerful solutions for you

-webp.webp)

Impactful data: our price insights tool 📈

Analyze historical trends and compare prices across countries or categories.

.jpg)

Education to support sourcing decisions 🎓

Online course: Sustainable Olive Oil Production, Quality, and Economics