")

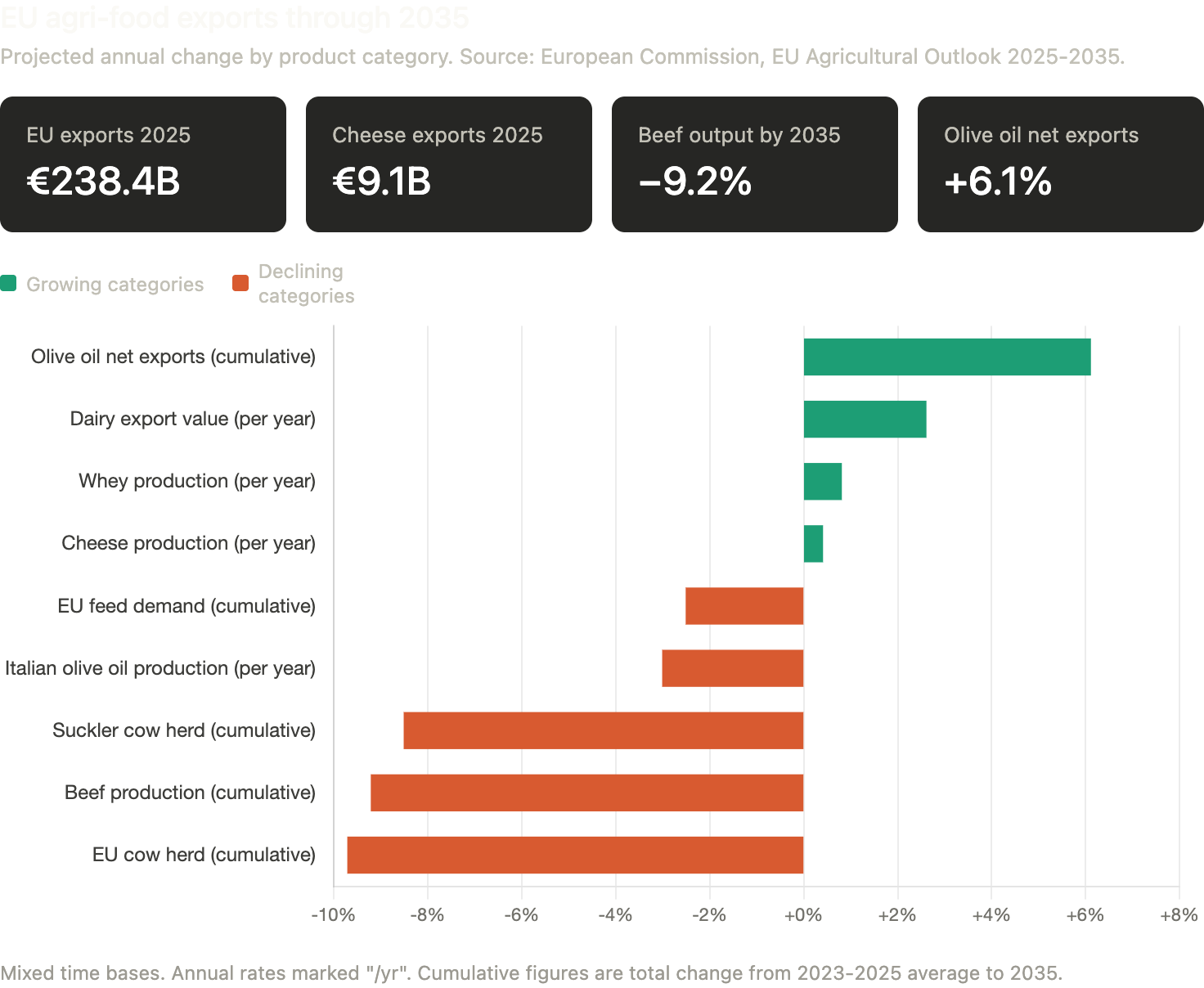

When the European Commission published its 2025-2035 agricultural outlook in December, the headline read well: EU agri-food exports hit a record €238.4 billion in 2025, and the Commission expects growth to continue through 2035. Look past the headline and the story is narrower. The report says, plainly, that "EU's market shares in products such as beef, pigmeat, and soft wheat" are under pressure from global competition, and that EU export growth is being carried by "high value added products like cheese, whey powders and olive oil." That is not a growth plan. It is a strategic shift, and it is already visible in the 2025 trade figures.

What is growing: cheese, whey, olive oil

EU dairy exports grew €1.1 billion in 2025, one of the three largest product-category increases of the year. Cheese and curd alone reached €9.1 billion. Volumes were broadly stable, but prices rose, especially for cheese and butter, and growth came from North America, the Middle East, South-East Asia, and other Western European destinations.

The Commission projects EU cheese production to grow 0.4% per year through 2035, and whey production 0.8% per year. Dairy export volumes barely change in the projection. Export value could grow 2.6% per year, slower than the last decade's 3.2% but still meaningful. In other words, EU dairy is not producing much more. It is selling what it produces into higher-margin categories.

Olive oil is the other growth story. Net EU olive oil exports are projected to rise 6.1% by 2035. On paper, that sounds broadly positive. In practice, it masks a geographic rebalancing. Spanish production is projected to approach 1.8 million tonnes per year by 2035, up from roughly 1.4 million tonnes today, as super-intensive irrigated groves replace traditional non-irrigated farms. Portuguese production is also rising. Italian production is projected to decline about 3% per year. Greek production could fall below 180,000 tonnes. So "EU olive oil exports" increasingly means "Iberian olive oil exports," even as the olive oil market itself normalises after the 2022-2024 price spike.

What is shrinking: beef, pigmeat, soft wheat, sugar

EU beef production is projected to fall 9.2% by 2035, with the cow herd shrinking by 9.7%. Pigmeat is losing global share. Soft wheat is being squeezed by Black Sea and Australian competitors. EU sugar faces Brazil, India, and Thailand, all of which combine lower production costs, better climates, and more aggressive export logistics. Feed demand inside the EU is projected to fall 2.5% by 2035, a direct consequence of the shrinking livestock base.

The common thread is cost. For raw commodities traded in bulk, landed price per tonne decides orders. The EU cannot beat Brazilian sugar, Argentine soybeans, or New Zealand milk powder on cost, and nothing in the outlook suggests that will change.

Why the EU is shifting up-market

EU processors face the same pressure farmers do, from the other end of the chain. When global bulk prices sit below EU production costs, processors push further into product lines where pricing power still exists: branded cheeses, protein-enriched whey derivatives, specialty olive oils, cured meats, wines with origin claims.

The Commission's own framing is blunt: "global competition is forcing processors to boost their profit margins by extending their higher value-added product lines." The shift is not a strategy chosen from strength. It is the part of the chain where margins still work.

What it means for farmers and traders

Dairy farmers supplying into cheese and specialty whey processing have an opportunity, but it comes with longer contracts and tighter specification. Basic fluid milk margins stay thin.

For olive growers, geography is becoming destiny. Spanish and Portuguese super-intensive operations will expand. Traditional groves in Greece, southern Italy, and parts of southern France face a harder path without irrigation investment, cooperatives, or protected-origin branding.

For beef, pigmeat, and cereal producers, the outlook describes a long contraction. Input costs remain well above pre-crisis levels, regulatory pressure builds, and the 3 million EU farms that disappeared in the last decade will likely be followed by more consolidation.

For traders, the map itself is the signal. Cheese, whey, and Iberian olive oil are where growth sits. Basic commodities remain large in volume, but the margin stories are elsewhere, and volatility around the edges (drought, tariffs, geopolitics) is constant.

The Commission calls this outlook a success because export value keeps rising. What sits underneath, though, is smaller: fewer farms, less volume, and more specialisation inside narrower product categories.

References

- European Commission (2025). EU agricultural outlook 2025-2035. DG Agriculture and Rural Development, Brussels.

- European Commission (2026). Monitoring EU agri-food trade developments in 2025. DG Agriculture and Rural Development, Brussels.

")