")

The global tomato market in 2024–2025 is characterized by record production levels, climate-driven volatility, and shifting price dynamics across farmgate, wholesale, and retail segments. Despite a projected 11.5% decline in processing tomato production for 2025, fresh tomato markets remain robust, with demand for specialty varieties and premium products reshaping trade flows.

Tomato Varieties in Global Trade: Classification and Commercial Applications

The global tomato trade revolves around distinct varieties optimized for specific market segments, ranging from industrial processing to premium fresh consumption. This analysis categorizes tomatoes into five primary commercial types—industrial, fresh consumption, cherry, Roma (plum), and vine tomatoes—detailing their varietal characteristics, production regions, and market applications.

Tomatoes for Industrial Processing

Industrial tomatoes are cultivated specifically for their high yield, thick flesh, and concentrated solids content, making them ideal for processed products such as paste, sauces, and canned goods. Key characteristics include intense flavor, strong disease resistance, and suitability for mechanical harvesting. Major production hubs include China (Xinjiang), California (USA), and Italy (Emilia-Romagna), where arid climates and advanced irrigation systems support large-scale, efficient output. Over 90% are used for paste or canned products, with China exporting roughly 1.2 million tonnes of paste annually.

Tomatoes for Fresh Consumption

Fresh-market tomatoes are bred with a focus on visual appeal, shelf life, and texture. These varieties are valued for their juicy flesh and are commonly used in salads and sandwiches. They are also optimized for uniform ripening and transport durability. Mexico and Spain account for around 60% of the fresh tomato supply to North America and the EU, respectively, primarily supported by advanced greenhouse systems that ensure year-round output.

Cherry Tomatoes

Cherry tomatoes, typically weighing less than 25g, are prized for their sweetness and snackability. In the Netherlands, high-tech greenhouses yield around 3.5 kg/m², serving premium European markets where retail prices can reach €3.50/kg. These tomatoes are often packaged in 250g clamshells to emphasize convenience and freshness. Turkey has also emerged as a strong competitor, increasing its cherry tomato exports by 22% since 2022.

Roma (Plum) Tomatoes

Roma tomatoes are oval-shaped, low-moisture varieties ideal for cooking and processing. Two well-known cultivars are:

- San Marzano: DOP-certified, 7%+ solids, used in authentic sauces.

- Granadero: Hybrid with 6.2° Brix and disease resistance, used across Mediterranean processors.

Vine Tomatoes

Sold while still attached to the vine, these tomatoes command premium prices due to their perceived freshness and enhanced presentation. In 2024, Turkey’s vine tomato exports to Europe grew by 18%, benefiting from shorter transit times compared to Spanish competitors and strong demand in Northern European markets.

Global Tomato Production Overview

Record Output in 2024

Global tomato production reached 186 million metric tonnes in 2024, with processed tomatoes accounting for 45.7 million tonnes—a 3.3% increase from 2023. China solidified its dominance, contributing 37% of global output (68.2 million tonnes), primarily from Xinjiang’s processing regions. California, the second-largest producer, saw output decline to 11 million short tons (9.98 million metric tonnes) due to heat waves and water constraints. The European Union maintained stable production at 11 million tonnes, with Italy (5.6 million tonnes) and Spain (2.8 million tonnes) leading despite spring planting delays. Moreover, for 2024, tomato production for fresh consumption in Europe reached 6,670 tonnes, with Spain leading the market at 1,650 tonnes. It was followed by Italy (1,189 tonnes), the Netherlands (828 tonnes), Poland (934 tonnes), and France (527 tonnes).

2025 Production Forecast

The WPTC projects an 11.5% decline in global industrial tomato output for 2025, totaling 40.5 million tonnes, driven by reduced planting in China (-42%) and California (-7%) caused by low prices in 2024 in China. Northern Hemisphere yields face risks from excessive rainfall in Europe and drought in the Mediterranean, while Southern Hemisphere production remains stable at 3.05 million tonnes.

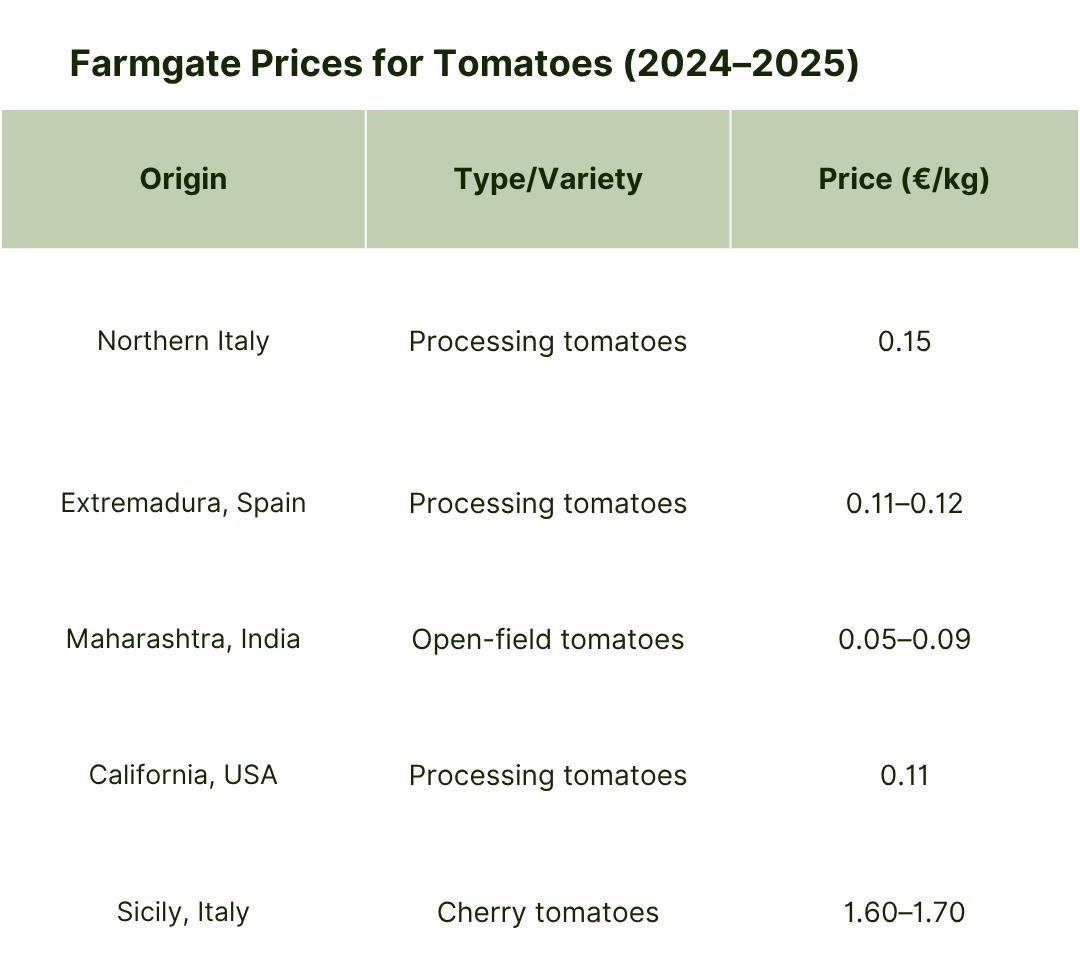

Farmgate Prices: Regional Disparities and Production Costs

Farmgate prices for processing tomatoes vary significantly across regions, influenced by factors such as production scale, labor costs, and climatic conditions. In Spain (Extremadura), prices averaged €0.11–0.12/kg—among the lowest in the EU—thanks to high-volume contracts and efficient large-scale operations. In Northern Italy, contract prices rose to €0.15/kg, marking a 5% year-over-year increase driven by tighter supply and adjustments for rising energy costs. In California (USA), prices declined to €0.11/kg as growers reduced planting in response to surplus inventories and persistent water shortages. Meanwhile, in India (Maharashtra), farmgate prices fell sharply to €0.05–0.09/kg due to post-harvest oversupply, underscoring the sector’s vulnerability to market gluts.

While EU prices for processing tomatoes remain higher than the global average, particularly compared to China, where prices range from €0.03–0.033/kg—rising input costs continue to pressure producer margins.

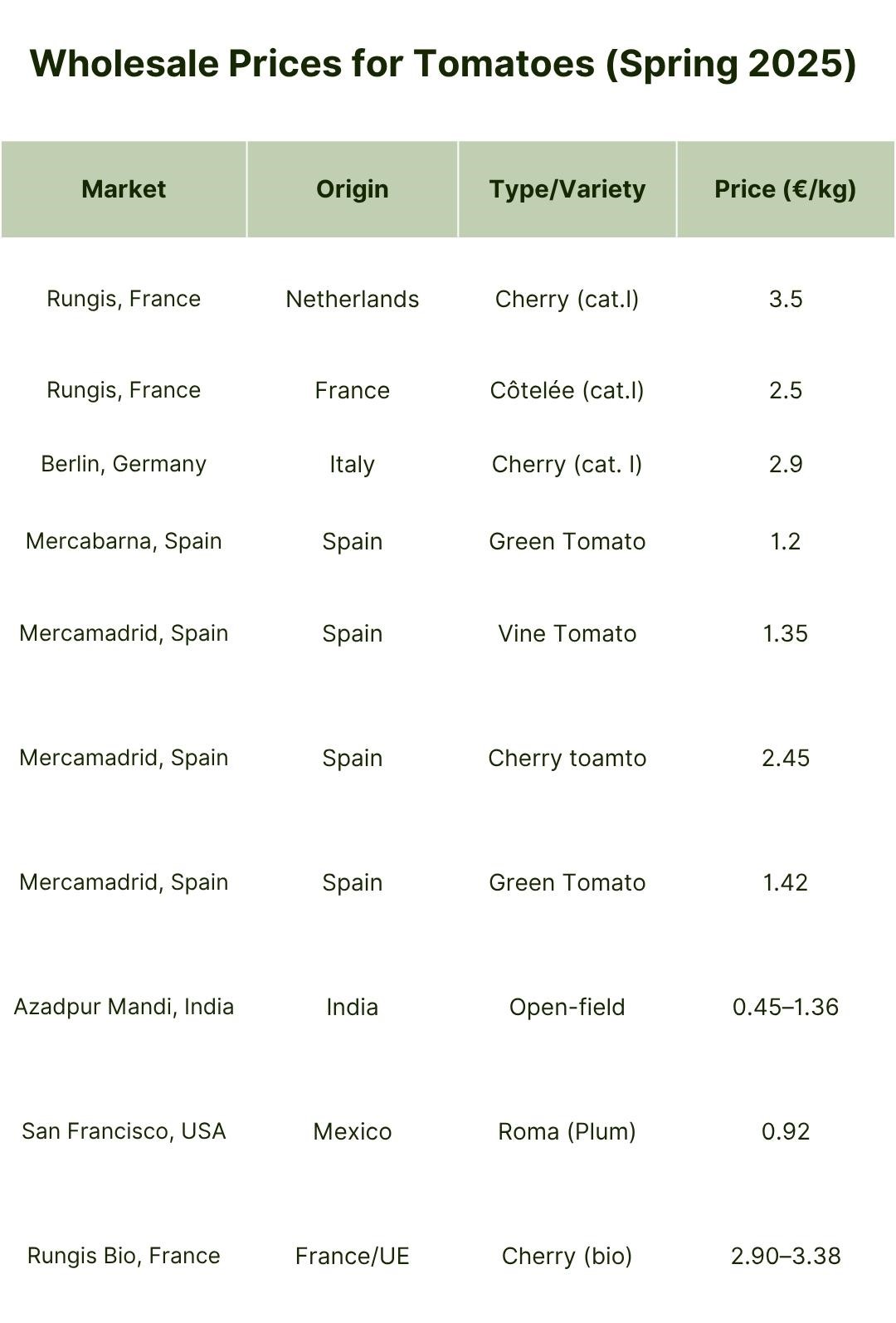

Wholesale Prices: Premiums for Specialty Varieties

Wholesale markets continue to reflect strong premiums for niche products and quality-driven demand. In the Netherlands, cherry tomato prices reached €3.50/kg in April 2025—up 43% compared to the 5-year average—while vine tomatoes held steady at €1.48/kg, marking a 16% year-over-year increase. Spanish and Italian cherry tomatoes seem to be offered at lower prices, at 2.45 to 2.90 euros per kg. These elevated prices are supported by advanced Dutch greenhouse operations and export-oriented supply chains. In Spain, vine tomatoes averaged €1.35/kg, an 80% YoY surge driven by delayed plantings and robust demand from Northern Europe. In Sicily, Italy, plum tomato prices spiked to €5.50/kg during November 2024 amid severe shortages caused by drought, highlighting the increasing influence of climate volatility. Meanwhile, in India’s Azadpur Mandi, prices fluctuated between €0.36 and €1.36/kg, reflecting the supply instability brought on by monsoon-related weather disruptions. Overall, Northern European markets prioritize product consistency and quality, while Southern Europe and parts of Asia face growing challenges from climate-driven supply shocks.

Retail Prices: Packaging and Consumer Preferences

The retail price data for tomatoes across several major markets in spring 2025 reveals significant regional differences shaped by local production costs, consumer preferences, and market structures. In the United States and Germany, standard loose tomatoes command some of the highest prices, ranging from €4.35 to €5.30 per kilogram, reflecting higher labor, transportation, and retail overheads, as well as a greater share of imports in the off-season. In contrast, Mediterranean countries such as Spain, Greece, and Italy offer much more affordable prices, with standard loose tomatoes in Spain retailing as low as €0.89 per kilogram and in Greece ranging from €0.83 to €2.15 per kilogram. This difference is largely attributable to favorable growing conditions, shorter supply chains, and the dominance of domestic production.

The Netherlands, a major exporter and innovator in greenhouse agriculture, shows moderate prices for loose (€1.18/kg) and vine tomatoes (€1.48/kg), with a premium for cherry tomatoes in clamshell packaging (€3.50/kg). The higher price for cherry tomatoes reflects both the cost of packaging and their positioning as a premium product. Spain, on the other hand, offers cherry tomatoes in clamshells at just €1.63/kg, suggesting either lower packaging costs, higher production volumes, or less emphasis on premium branding. Italy’s cherry and specialty tomatoes, also sold in clamshells, are priced between €2.10 and €2.80/kg, indicating a market that values quality and regional varieties but remains competitive compared to northern Europe.

Emerging markets such as China, India, and Egypt display the lowest retail prices, with standard loose tomatoes selling for €1.07, €0.51, and €0.38 per kilogram, respectively. These low prices are driven by local production, lower input and labor costs, and less intensive packaging or branding. However, these markets may also face greater price volatility due to weather and supply chain disruptions. Notably, the data illustrate how packaging influences retail prices: cherry tomatoes in clamshells consistently fetch higher prices than loose or vine types, especially in Western European and North American markets. This premium in prices is associated with both perceived convenience and quality, as well as the additional cost of packaging materials and logistics.

Overall, the trend of choosing higher-quality and more unique products is especially strong in Northwestern Europe, where consumers really value new and interesting options, like tomatoes in unusual colors, and care about how the food is grown and packaged in a sustainable way. In summary, retail tomato prices in 2025 reflect a complex interplay of geography, production systems, consumer demand, and retail strategies, with packaging and product differentiation playing increasingly important roles in price formation.

Factors Driving Price Differences

A range of structural and external factors contributed to regional price disparities in 2024–2025. Climate volatility played a major role. Drought conditions in key growing areas like Sicily (Italy) and California significantly reduced yields, fueling retail and wholesale price surges. Additionally, excessive spring rainfall across parts of the EU delayed tomato plantings, which in turn tightened summer supplies and supported elevated prices.

Energy and labor costs further influenced pricing. Dutch greenhouse operations, reliant on stable energy inputs, faced rising costs that contributed to wholesale cherry tomato prices reaching €3.50/kg. Similarly, U.S. retail prices reflected the effects of labor shortages and transport disruptions, especially in the aftermath of hurricane-related infrastructure damage.

Global trade dynamics also shaped the pricing landscape. In Q4 2024, China’s exports of processed tomatoes dropped by 46,000 tonnes, indirectly easing supply pressure on EU producers. Meanwhile, Moroccan tomato imports helped stabilize Spain’s winter market but led to softer prices for standard varieties, particularly in southern Europe.

Market 2025 Outlook

Production Risks

The global tomato production landscape for 2025 is shaped by a confluence of climatic disruptions, economic pressures, and strategic supply adjustments, driving an 11.5% decline in processing tomato output to 40.5 million metric tons compared to 2024. In the Northern Hemisphere, China’s projected 42% production collapse (to 6.0 million tons) stems from 2024’s low farmgate prices, which disincentivized planting, while California’s 14% reduction in planted acreage (to 200,000 acres) reflects efforts to balance surplus inventories and water scarcity. Southern European producers face dual challenges: excessive spring rains delayed planting by 3–4 weeks in Spain and Portugal, compressing growing windows, while drought in Southern Italy threatens irrigation-dependent crops despite stable northern output.

Meanwhile, Egypt’s summer crop yields fell 20% due to extreme heat (40–42°C), exacerbating supply constraints. These climate shocks intersect with economic decisions, as high 2024 carryover stocks (from record processing volumes of 45.7 million tons) prompted growers to reduce planting, particularly in China and California. Conversely, stable Southern Hemisphere production (3.05 million tons) and incremental gains in Brazil and Chile highlight less climate-exposed regions’ capacity to offset Northern declines. The net effect is a fragmented global supply chain: regions with resilient infrastructure (e.g., Dutch greenhouses) or favorable policies (e.g., Italy’s €145/ton contracts) mitigate losses, while water-stressed and economically vulnerable areas face steeper declines.

Price Projections

Changes in weather, limits on how much can be produced, and changing consumer needs are expected to cause big ups and downs in tomato prices worldwide in 2025. Severe droughts in Sicily and California are reducing yields of premium fresh varieties (e.g., cherry and vine tomatoes), creating localized supply shortages that have already spiked Italian wholesale prices for plum tomatoes to €5.50/kg. Simultaneously, excessive spring rains in Spain and Portugal delayed planting by 3–4 weeks, compressing the Northern Hemisphere growing window and raising production costs, which are projected to elevate EU farmgate prices by 5–7%.

In China, the drop in industrial tomato output is easing global oversupply pressures, stabilizing farmgate prices at ¥2.2–2.4/kg ($0.30–0.33/kg) despite weaker export demand. Meanwhile, rising fuel and energy costs compound wholesale and retail price increases, particularly for long-distance shipments of Mexican Roma tomatoes to the U.S. and Dutch greenhouse cherries to EU markets, where logistics may inflate prices by 5–7%. Conversely, stable water allocations in California and efficient Northern European supply chains mitigate volatility in key industrial and fresh segments, ensuring moderate price growth for bulk buyers. These dynamics underscore a fragmented market: climate-stressed regions face supply-driven inflation, while regions with resilient infrastructure or diversified sourcing maintain relative stability.

Demand Trends and Market Shifts

Demand–Supply Dynamics

Global demand for processed tomatoes remains stable at approximately 45–46 million metric tonnes. However, China's recent export decline—down 46,000 tonnes in Q4 2024—may help ease pricing pressures for producers in other regions. In the fresh tomato segment, consumption of cherry and grape tomatoes continues to rise, with a 12% increase observed across both the EU and the U.S. This growth is largely driven by consumer trends favoring healthy snacks and convenient salad ingredients.

Climate and Geopolitical Risks

Weather-related disruptions remain a key risk for the tomato industry. Persistent droughts in Southern Europe and California have led to yield reductions, while excessive rainfall in Northern Italy and Spain has delayed planting schedules, tightening supply during peak seasons. Geopolitical developments and trade policy shifts have also impacted market dynamics. In 2024, Moroccan tomato exports to the EU surged by 19%, increasing competitive pressure on Spanish and Dutch producers, particularly during the winter season.

Innovation and Production Costs

Innovation in tomato breeding continues to influence retail trends. Seedless hybrid varieties now account for 35% of U.S. retail tomato sales, thanks to their extended shelf life and consumer appeal due to reduced waste. However, rising production costs pose challenges, especially in high-tech greenhouse operations. In the Netherlands, energy inflation has driven production costs up by 10–15%, contributing to elevated wholesale and retail prices for cherry tomatoes.

Conclusion

As climate disruptions intensify and consumer preferences evolve toward specialty and sustainable products, the global tomato market is undergoing a structural transformation. Producers, processors, and traders must adapt by investing in resilient varieties, optimizing input costs, and aligning with shifting demand patterns, particularly for premium and off-season segments. Success in this new landscape will depend not only on yield and price efficiency but also on agility in responding to environmental pressures, regulatory changes, and evolving trade dynamics.

Read more:

Deep Dive in Watermelon Prices: A Comprehensive Price Study 2024-2025

Deep dive in green asparagus prices: A comprehensive price study 2024-2025

Sources:

World Processing Tomato Council (WPTC)

European Commission’s Agri-food Data Portal