")

The world trades more food than ever. By 2023 about 60% of all the trade links that could exist between countries in food and agricultural products were actually in use, up from 47% in 2000. Yet the three cereals that feed most of the planet, wheat, maize and rice, still flow from a small group of exporters. That concentration is the quiet fragility inside an otherwise resilient system, and it is what turns a bad harvest in one country into a price rise felt far beyond its borders.

FAO's State of Agricultural Commodity Markets 2026 maps the global trade network in detail, and the picture for staples is consistent. Trade overall has grown dense and well connected, but the specific markets for wheat, maize and rice remain narrow, leaning on a few origins and a thin set of routes.

Key takeaways

- Trade is more connected than ever. About 60% of all possible trading relationships between countries were active in 2023, up from 47% in 2000.

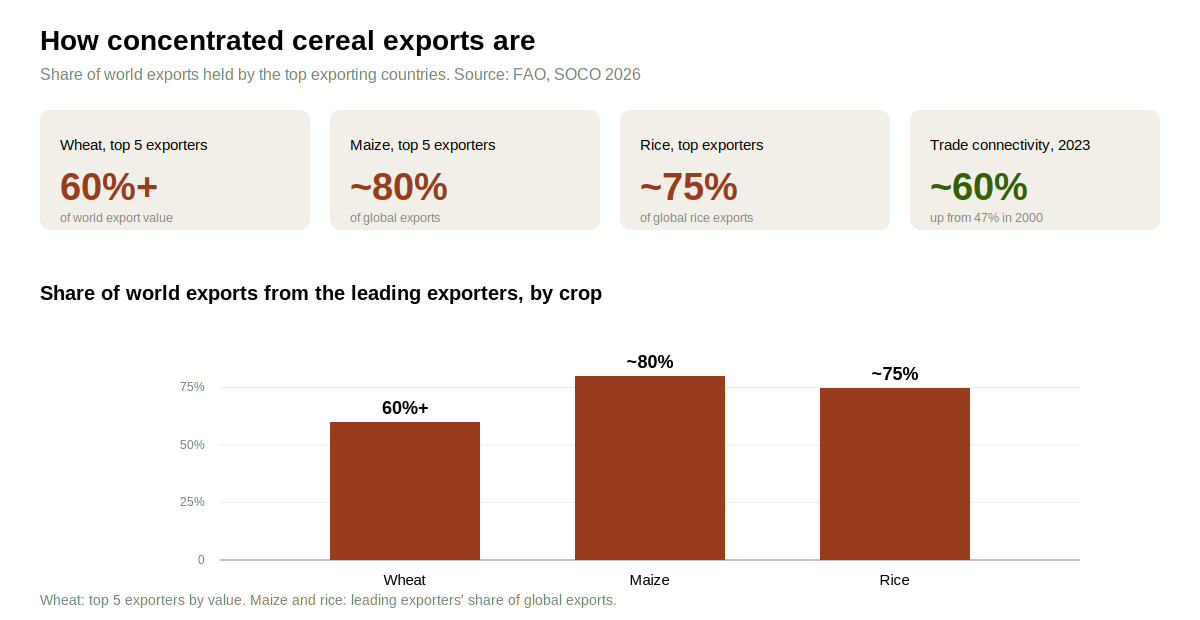

- A few exporters dominate each cereal. Five countries supply more than 60% of wheat export value, close to 80% of maize exports, and about 75% of rice exports.

- Little of each crop is actually traded. Only around 10% of world rice production crosses a border, and most cereals are eaten where they are grown.

- The cereal networks are sparse. Of all the trade routes that could carry them, only 9% are used for wheat, 11% for maize and 16% for rice.

- Connection is the buffer. Countries with more trade partners recover from a supply shock faster, because they can re-source when one supplier fails.

Trade has never been more connected

Between 2000 and 2023 the network of food and agricultural trade grew denser across the board. About 60% of all possible trading relationships between countries were active by 2023, against 47% at the start of the century, and connectivity rose in every major network. The report's high-frequency data shows why this matters. Countries with more trade partners and deeper integration into world markets recover from a supply shock faster, because when one source fails they can turn to another without waiting for a single supplier to bounce back.

Most traded grain comes from a handful of countries

Behind that headline connectivity, the staple cereals are the exception. For wheat, five exporters, Australia, Canada, Russia, Ukraine and the United States, together account for more than 60% of world export value. Maize is tighter still, with Argentina, Brazil, France, Ukraine and the United States supplying close to 80% of global exports, and demand is concentrated too, as China, Japan, Mexico, South Korea and Vietnam take around 36% of all maize imports. Rice is the most concentrated of the three, with India, Pakistan and a few South-east Asian countries providing roughly 75% of all rice shipped. When so much of a crop comes from so few origins, a problem in any one of them moves the entire market.

Only a thin slice of each crop is actually traded

Concentration is compounded by how little of each harvest ever leaves its country of origin. Only about 10% of world rice production is traded internationally, and most is eaten where it is grown, so a small shift in one exporting country can swing the traded market sharply. The networks themselves are sparse. Across all food and agricultural products 60% of possible trade routes are in use, but for wheat only 9% of the links that could exist are active, for maize 11%, and for rice 16%. Global rice trade has grown quickly, reaching around 60 million tonnes in 2024, a 160% rise since 2000, yet it still runs through a small number of routes.

Why concentration is a vulnerability

A thin, concentrated market has little slack. When one large exporter has a poor harvest or holds back shipments, buyers have few alternatives, so the shortfall shows up quickly as a higher world price. The 2026 European heatwave that cut France's maize crop is a live example, because a handful of countries dominate maize exports, a loss in one of them tightens the whole market at once. Concentrated networks also pass trouble along faster, and the countries most exposed are the net food importers that depend on those few suppliers and have the least room to switch.

What lowers the risk

The remedy the report points to is deeper connection. Importers that spread their purchases across several exporters, and keep strong links to well-connected trading hubs, absorb a supplier's failure instead of amplifying it. Building those relationships takes time and investment, but it is the most reliable buffer a food-importing country has. Keeping trade open in a crisis is the other half of the same lesson, since export restrictions shrink the very network that would otherwise spread a shock thinly across many partners. Alongside open trade, targeted domestic support such as cash transfers protects vulnerable households without draining supply from the market, which is what turns a well-connected market into real food security.

Sources

- FAO. 2026. The State of Agricultural Commodity Markets 2026. Rome.

")