")

Global Olive Oil Market Update – Week 19, 2025

The global olive oil market is entering a phase of cautious optimism in Week 19 of 2025, marked by improved production prospects, evolving regulations, and shifting market dynamics across major producing countries.

Production and Supply Outlook

The flowering season is approaching in the Mediterranean, traditionally signaling a period of heightened market activity and increased purchases in May and June. Favorable spring rains, especially in Spain, have boosted expectations for the 2025/26 crop, with the European Commission forecasting a 31–32% increase in EU olive oil output for the 2024/25 season. Spain, the world’s leading producer, is expected to see nearly a 50% rise in yield compared to the previous year, following two years of drought-induced shortages.

Outside the EU, Turkey and Tunisia have also reported strong production recoveries, with Turkey’s output more than doubling compared to last season and Tunisia’s increasing by over 50%.

Trade Volumes and Market Movement

March 2025 saw robust market activity, with Spain reporting total olive oil outputs of approximately 140,000 tonnes, up by 50,000 tonnes from the same month last year. Exports accounted for about 85,000 tonnes, while domestic consumption absorbed around 51,000 tonnes. EU import data shows a notable increase in olive oil imports from Tunisia and Turkey, while imports from Argentina have declined sharply.

Producer Prices and Market Segmentation

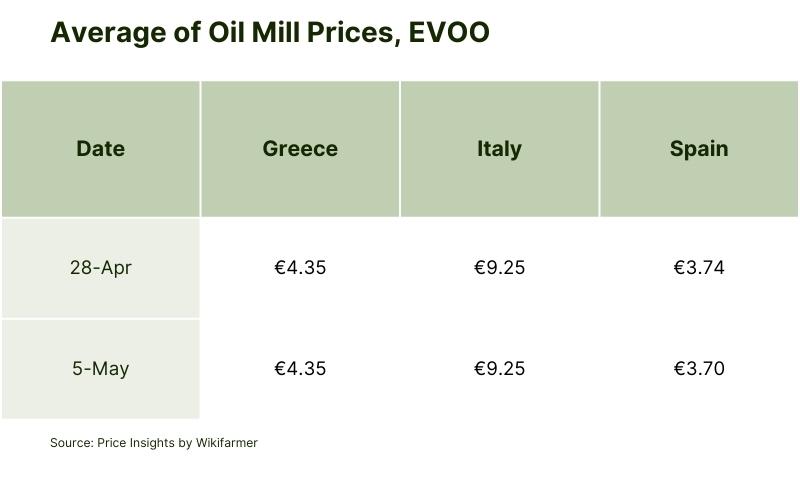

Producer prices have moderated from the record highs of 2024 but remain above historical averages due to inflation and elevated production costs. As of early May 2025, our experts in Spain have reported :

- High-quality extra virgin olive oil is priced above €4.00/kg.

- Medium quality ranges from €3.80 to €3.90/kg.

- Lower quality is between €3.50 and €3.70/kg.

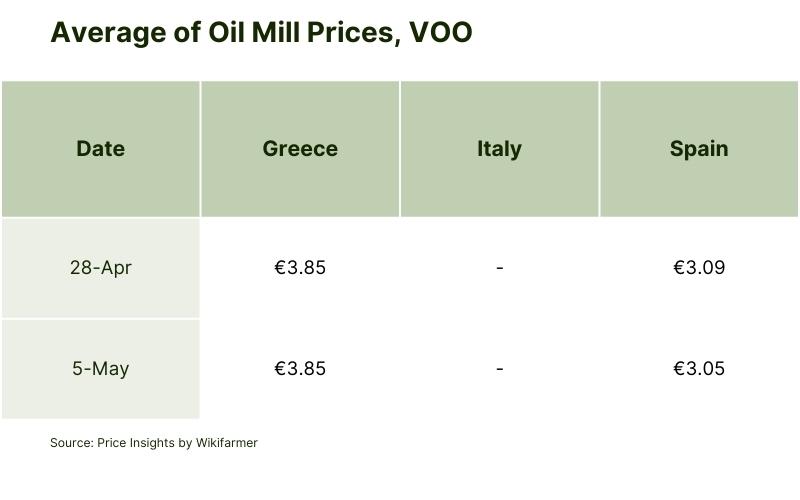

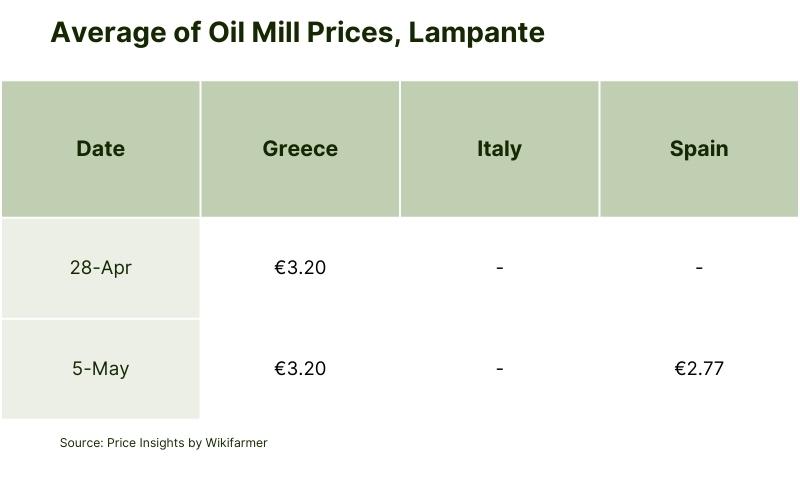

At this point, Spanish producer prices are down nearly 29% from last year, averaging €3.77/kg for extra virgin olive oil. Market segmentation by quality remains pronounced, with premium oils commanding a price premium and lower-quality oils facing weaker demand. In Greece, many producers are holding back stocks in anticipation of better prices, with the market remaining relatively stable, while in Italy, weaker harvests have kept prices higher than in Spain.

Weather and Crop Conditions

Recent rains in Spain and other Mediterranean countries have improved soil moisture, creating optimism for the upcoming crop. However, producers remain cautious, as continued favorable weather will be essential for a successful flowering and fruit set in the coming weeks. However, if prices fall below €4/kg, some Greek growers have indicated they may not harvest next year, underscoring ongoing concerns about profitability.

Regulatory and Structural Changes

Spain has enacted a significant update to its vegetable oil regulations, the first since 1983. The new rules:

- Allow production from a broader range of authorized edible fruits and seeds, not just the traditional eight.

- Permit both refined and mechanically pressed oils, with precise labeling requirements.

- Reserve the terms “virgin” and “extra virgin” exclusively for olive oil.

- Introduce stringent traceability and anti-fraud measures, including digital shipment tracking and non-refillable containers for extra virgin olive oil in hospitality.

- Require a new financial contribution from producers to support marketing, promotion, and innovation, which started in October 2024.

These changes are designed to enhance transparency, protect consumers, and strengthen Spain’s competitive position in the global market.

Consumer Demand and Market Sentiment

Consumer demand is gradually recovering as prices ease and the Mediterranean diet remains popular. There is growing interest in organic and high-quality olive oils, supporting sales in premium segments. However, the pace of inventory clearance and the influx of new supply will continue to influence short-term price dynamics.

Summary and Outlook

The global olive oil sector is stabilizing, with improved crop prospects, regulatory modernization, and a gradual return of consumer demand. Producers remain vigilant, balancing the need to clear stocks with the desire to secure favorable prices. The coming weeks will be critical as the flowering season unfolds and new production data becomes available.

References

Spanish Ministry of Agriculture, Fisheries and Food – New Quality Standards for Edible Vegetable Oils

European Commission – Olive Oil Market Data and Price Monitoring

Agencia de Información y Control Alimentarios (AICA) – Olive Oil Production and Stock Reports

International Olive Council (IOC) – Market News and Production Updates

Cooperativas Agroalimentarias de España – Monthly Market Reports

Italian Ministry of Agriculture – Olive Oil Price and Production Updates

Hellenic Ministry of Rural Development and Food – Greek Olive Oil Market Data

European Union – Official Journal: Regulation Updates for Olive Oil

Tunisian Ministry of Agriculture – Olive Oil Export and Production Data

Turkish Statistical Institute – Agricultural Production and Export Statistics

")