")

AICA data | May 2026

The latest figures from Spain’s Agencia de Información y Control Alimentarios (AICA) provide a snapshot of the final stages of the 2025/26 olive oil campaign. Market activity slowed further in May, while stocks continued to decline as olive oil moved through commercial channels. Market attention is focused on the flowering, fruit set, and early expectations for the 2026/27 harvest.

Stay up to date with our Weekly Olive Oil Digest

The tail-end of production

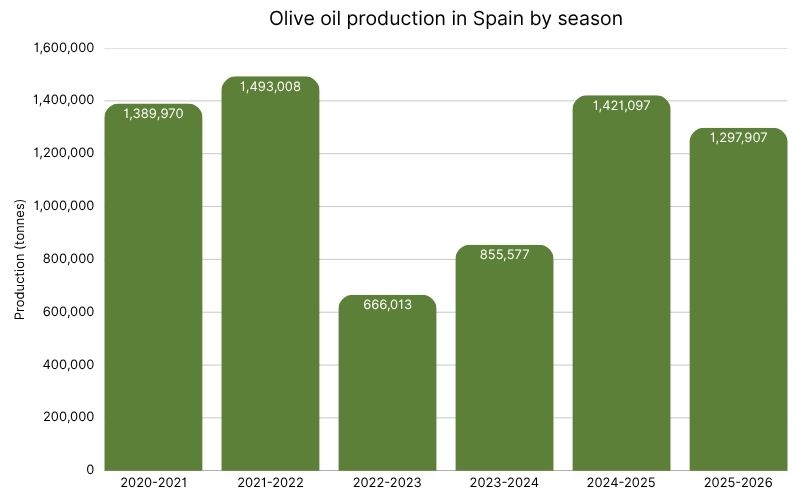

Spain produced 1,917 tonnes of olive oil in May, down 85.38% from 13,114 tonnes in April, reflecting the very end of the production season.

.jpg)

This brings the total cumulative production for the 2025–2026 campaign to:

- 1,297,907 tonnes

This final figure is just 5.4% below MAPA’s initial October estimate of 1,371,938 tonnes and 8.3% below the previous campaign's figure of 1,415,767 tonnes.

Since harvesting and milling activities have concluded, the market is focused on stock management, demand trends, and production expectations for the upcoming season.

Stocks continue to decline steadily

Total olive oil stocks at the end of May stood at 774,987 tonnes, down 10.2% from 863,339 tonnes at the end of April, representing a monthly reduction of more than 88,000 tonnes.

Stock distribution across the sector was as follows:

- Olive mills: 506,972 tonnes (-15.5% month-on-month)

- Bottlers and refiners: 261,498 tonnes (+2.8% month-on-month)

- Patrimonio Comunal Olivarero: 6,517 tonnes (-25.5% month-on-month)

.jpg)

The reduction in mill inventories and the rise in bottler stocks indicate a continued transfer of oil into commercial channels. Packaging activity and fulfillment of commercial commitments continue, despite slower overall market demand.

Market outputs fall further in May

Total market outputs in May reached:

- 90,161 tonnes

This is a 4.62% decline from April's 94,527 tonnes.

This comes as a disappointment for many market participants who expected demand to recover from April lows. Instead, sales activity weakened further, highlighting a more cautious purchasing environment. Buyers are waiting and watching, limiting purchases to immediate needs and eyeing the next harvest, which is expected to be strong.

What does this mean for the market?

The May AICA figures paint a mixed picture: Stocks continue to decline at a healthy pace, with oil steadily moving through the supply chain without shortages, but the further decrease in monthly output suggests demand is still softening.

With no replenishment of supply until the new harvest begins, producers and traders are expected to manage stocks carefully during the coming months.

For buyers and packers, current inventory levels remain sufficient, but the market will increasingly focus on the size and condition of the upcoming 2026/27 crop.

Market sentiment is now being driven less by current availability and more by expectations for the next harvest, including weather conditions across Spain. If favourable conditions persist, prices could continue to decline, but concerns about drought, heat stress, or crop development could quickly shift sentiment and support prices.

Over the coming months, make sure to watch stock evolution, monthly output figures, and new-crop forecasts, which will be the key indicators shaping market direction.

Source olive oil with confidence on Wikifarmer's Marketplace:

Looking for gold standard EVOO?

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.