")

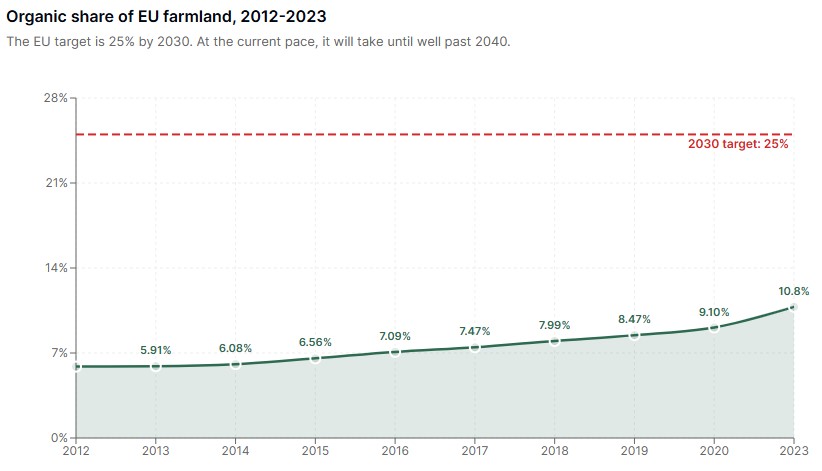

Organic farmland across the EU grew by 7.6 million hectares between 2013 and 2023, an increase of 84%. By 2023, an estimated 10.8% of the EU's total utilised agricultural area was farmed organically. That is real, measurable progress. But the EU's own target is 25% organic farmland by 2030, and at the current pace, Europe is not going to get there.

The latest Eurostat data, published in the 2025 edition of Key Figures on the European Food Chain, paints a sector that is growing steadily but unevenly. Some countries are well ahead. Others have barely started. And the gap between political ambition and on-the-ground reality raises a question that matters to every farmer considering the transition: is going organic actually worth it?

The numbers look good until you do the maths on 2030

Going from 10.8% to 25% in seven years means the EU needs to convert roughly another 23 million hectares. To put that in perspective, EU organic land grew from about 9.5 million hectares in 2012 to 14.7 million in 2020, adding 5.2 million hectares in eight years. Reaching the target would require nearly four times that pace. No policy currently in place makes that likely.

The growth so far has not been evenly spread. The leaders and laggards tell very different stories:

- Austria leads the EU with 25.3%, already hitting the 2030 target

- Estonia (22.8%), Portugal (22.5%), and Italy (18.8%) are well ahead

- Greece has been growing steadily, reaching 12.2%

- At the bottom, Malta (0.8%), Bulgaria (3.0%), and Ireland (4.3%) are barely getting started

The EU average is pulled up by a handful of frontrunners rather than broad continental progress.

.jpg)

Still, the direction is clear. The organic share of EU farmland almost doubled between 2013 and 2023, and that happened despite volatile input costs, a pandemic, and a war-driven energy crisis. Farmers converted because there were good reasons to do so, not because it was easy.

Organic farms are bigger, more productive, and use more labour

One of the more striking findings in the Eurostat data is that organic farming operations in the EU are, on average, significantly larger than conventional ones. In 2020, the average organic farm:

- Covered 42.4 hectares, compared with 15.9 for non-organic holdings

- Generated €86,400 in standard output, versus €37,500

- Kept 21.7 livestock units, compared with 12.5

- Employed nearly twice as much labour (1.5 annual work units versus 0.8)

.jpg)

What is being farmed organically also matters. Of the EU's 14.7 million organic hectares in 2020, permanent grassland accounted for 6.2 million (42%), arable land for 6.8 million (46%), and permanent crops such as olives, grapes, and fruit trees for 1.7 million (12%). The large share of grassland is significant because converting pasture to organic is simpler than converting arable or horticultural land. The harder conversions, the ones that require rethinking pest management, soil fertility, and crop rotations, still have the furthest to go.

Yet organic farms accounted for just 2.7% of all EU holdings in 2020, despite covering 6.8% of agricultural land. That tells us something important: organic conversion has so far been led by larger, better-capitalised farms that can absorb the upfront costs and income dips that come with the transition period. Small farms, which still make up the vast majority of EU agriculture, have been slower to make the switch.

This matters because small-scale farming and organic production are not natural opposites. In Greece, for instance, the average organic farm covers 14.3 hectares and generates €39,900 in output, nearly three times the €13,800 of a typical non-organic Greek farm. In countries like Austria, Italy, and Greece, smaller farms have found profitable niches through organic certification, particularly in high-value sectors like wine, olive oil, and dairy. But the pathway depends heavily on market access, fair certification costs, and consumer willingness to pay more.

.png)

The economics work, but not equally for everyone

The financial case for organic farming varies widely by crop, region, and market. In sectors with strong consumer demand and established supply chains, organic premiums can offset the lower yields that often accompany the transition. Organic olive farming, for example, has expanded significantly across the Mediterranean, driven by export demand and PDO certification.

For arable crops like cereals and oilseeds, the picture is more complicated. Yields typically drop during the conversion period, and organic inputs, while avoiding synthetic fertilisers, can be more labour-intensive and harder to source at scale. Without reliable premium prices, farmers on tight margins face a real financial risk during the two-to-three-year transition window.

EU policy tries to bridge that gap through the Common Agricultural Policy, which now channels more funding toward eco-schemes and organic conversion support. But farmer feedback consistently points to the same problems:

- Complex paperwork that discourages smaller operations

- Delayed payments that leave farmers exposed during the transition

- Support levels that do not always cover the true cost of conversion

For many small and medium-sized farms, the financial safety net is too thin to make the leap.

Fertiliser costs gave organic a boost, but the effect may not last

The 2022 fertiliser price spike, up 31.1% across the EU after Russia's invasion of Ukraine, briefly made the organic model look more competitive. Conventional farms that relied heavily on synthetic inputs saw their costs surge, while organic operations, already built around composting, cover crops, and biological nutrient cycling, were partly insulated.

Prices have since fallen sharply, dropping 24.5% in 2023 and another 17.6% in 2024. That has taken some of the urgency out of the cost argument for switching. But it also exposed a vulnerability in conventional farming: heavy dependence on global fertiliser markets makes input costs unpredictable. Organic systems, by building soil health over time, reduce that exposure, though the benefits accumulate slowly and are harder to quantify on a balance sheet.

Inorganic fertiliser use per hectare did fall 15.3% across the EU between 2013 and 2023, with 18 out of 25 reporting countries recording declines. Germany saw the largest drop, at 37.7%. Whether that reflects a genuine shift toward more sustainable agriculture or simply a temporary response to high prices remains to be seen.

What needs to change to reach 25%

Hitting the 2030 target would require a combination of things that are not yet happening at sufficient scale: faster certification, stronger premium markets, better technical support, and CAP payments that genuinely reflect the cost of conversion. It would also require addressing the demand side. If consumers do not buy organic products at volumes that sustain higher farm-gate prices, the economic incentive for farmers erodes regardless of how much public money flows into conversion support.

Farmers considering the transition need access to practical knowledge, market intelligence, and buyers willing to pay fair prices. On our marketplace, producers can list organic products and connect directly with buyers, while our price insights help track what organic commodities are actually fetching across different markets.

The EU's organic ambition is not unrealistic, but it is underfunded and behind schedule. The 7.6 million hectares converted over the past decade prove that farmers will make the switch when the conditions are right. The question is whether Europe can create those conditions fast enough for the remaining 22 million hectares.

References

Eurostat. (2025). Key figures on the European food chain, 2025 edition. Publications Office of the European Union.

")