")

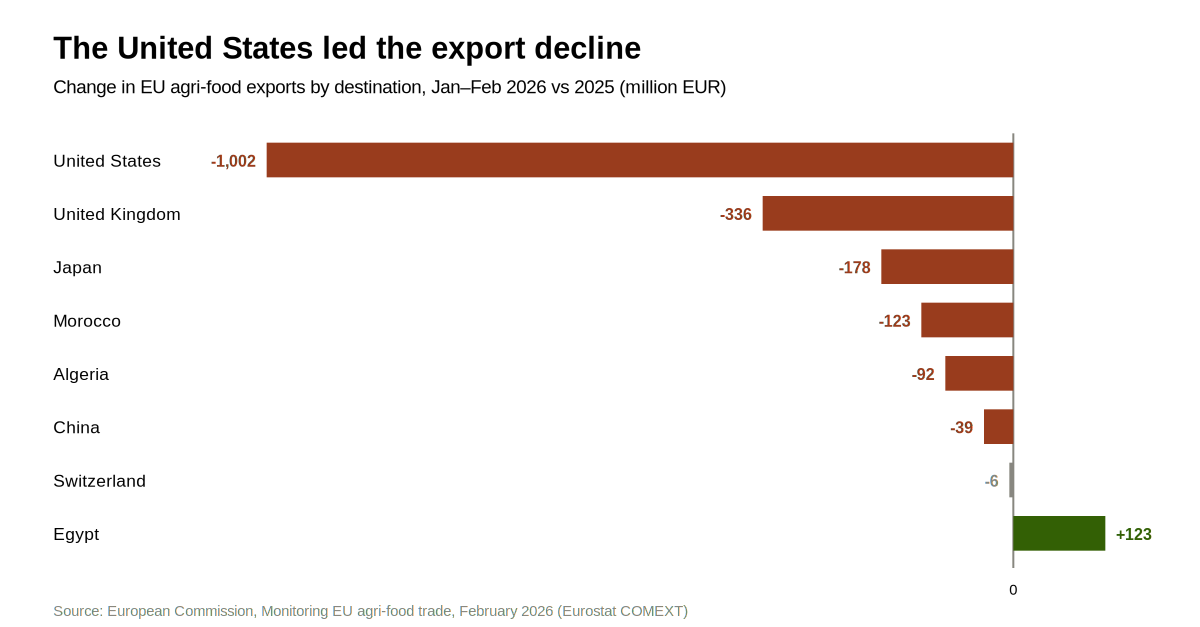

EU agri-food exports to the United States fell EUR 1.0 billion (-20%) in the first two months of 2026 compared with the same period in 2025, the steepest decline of any export market. The drop follows an unusually high 2025, when exporters shipped extra product to the US to get ahead of expected tariff increases (EC, 2026). That early buying has now run its course, and the largest single line in the EU's February trade report is a contraction in its second-biggest market.

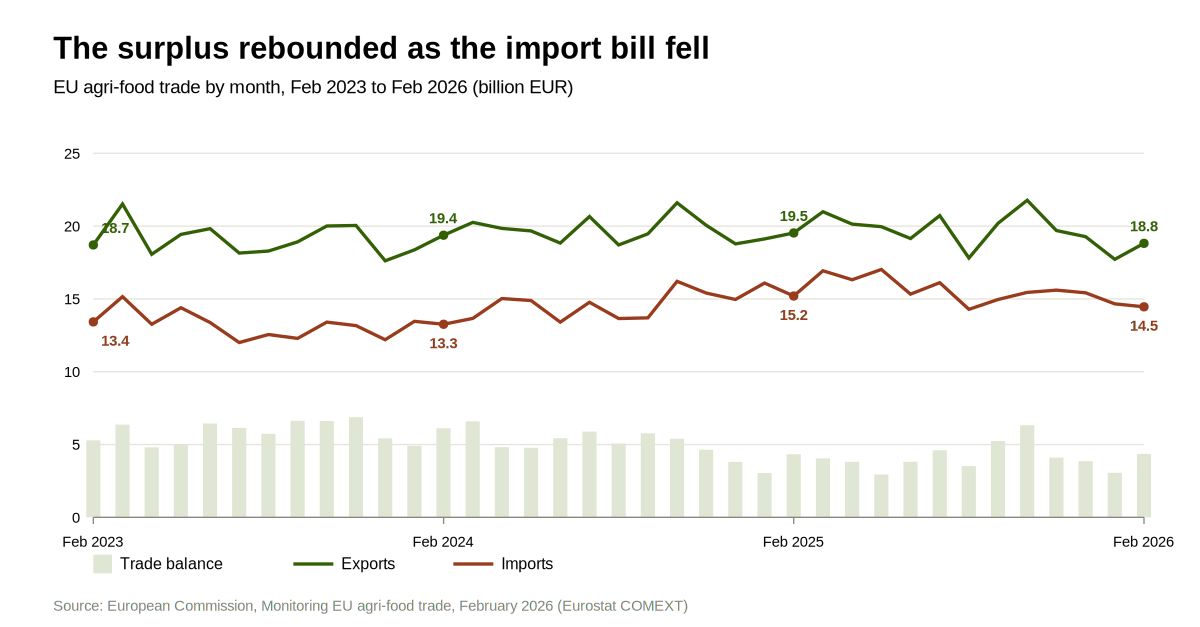

The wider numbers look healthier than they are. The EU exported EUR 18.8 billion of agri-food products in February 2026, 6% more than January but 4% less than a year earlier. It imported EUR 14.5 billion, down 1% from the month before and 5% from the year before. The trade surplus jumped 43% month-on-month to EUR 4.4 billion, roughly its February 2025 level. Stronger sales did not drive that rebound. It came from a falling import bill, led by lower cocoa prices.

This is the monthly counterpart to the longer story covered in the 2025-2035 outlook, where cheese, whey, and olive oil carry export growth while bulk commodities lose ground. The February figures show those same pressures in a single month, with the US shift now sitting atop them.

The US drop is the largest single change in the report

EU exports to the US fell harder than anywhere else, with drinks and olive oil leading the reductions. The reason sits in 2025. Buyers stocked up on EU products through last year to beat the tariffs they expected Washington to impose, so shipments ran unusually high. Once that stockpiling stopped, sales dropped back, and early 2026 now reads as a steep fall against an inflated base.

The olive oil detail matters for Mediterranean growers. EU exports of olives and olive oil fell by EUR 252 million (-24%) over the two months, on lower olive oil prices (-14%) and volumes (-11%), with the US named as a particular destination for the volume loss. For Greek and Spanish producers, a 24% fall in export value is a margin question, not an abstract trade statistic.

Other markets also slipped. The UK, the EU's first destination, fell EUR 336 million (-4%) on lower pigmeat and cereals. Exports declined to Japan (-EUR 178 million, -13%), Morocco (-EUR 123 million, -18%), and Algeria (-EUR 92 million, -18%). The clearest gain was Egypt, up EUR 123 million (+39%) on higher wheat exports.

Why the surplus number is misleading

Cumulative exports for January and February reached EUR 36.5 billion, EUR 2.1 billion below the same months of 2025. Imports fell further in absolute terms, to EUR 29.1 billion, down EUR 2.2 billion year-on-year. When the import bill drops faster than the export total, the surplus widens even as overall trade shrinks. A 43% jump in the monthly surplus reads like strength. Underneath it is a smaller trade flow on both sides.

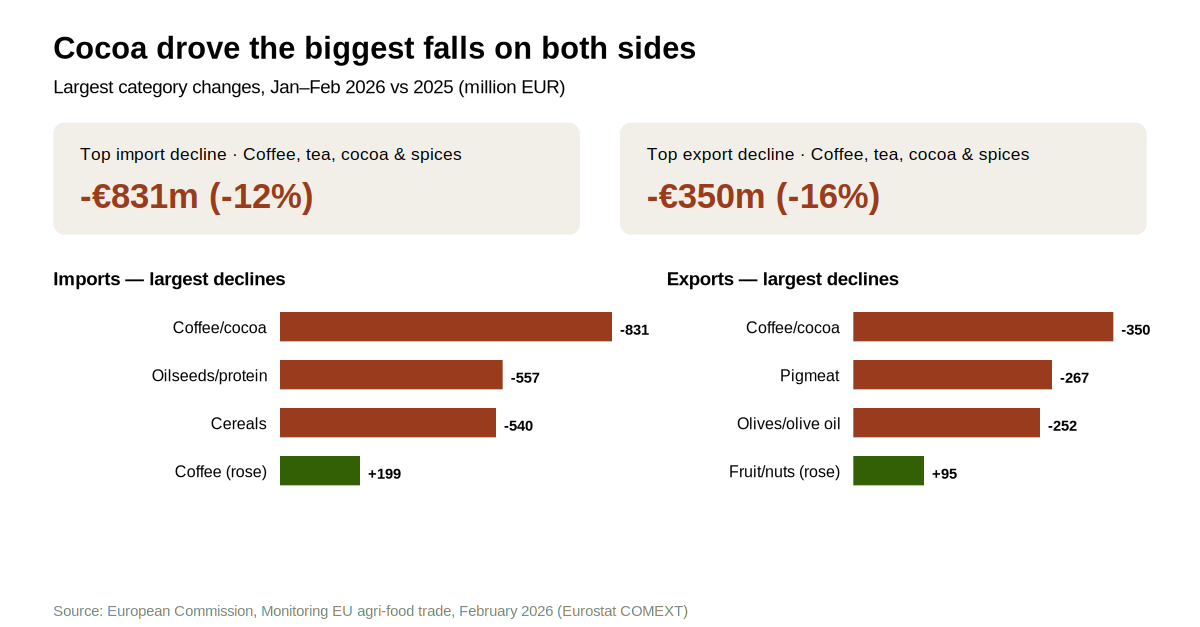

The category doing most of that work is cocoa. Imports of coffee, tea, cocoa, and spices fell by EUR 831 million (-12%) year-on-year, mostly on lower cocoa volumes (-14%) and prices (-15%). After two years of record cocoa prices, the correction is now feeding straight through to the import bill and the trade balance.

Cocoa cuts both ways. Imports from Côte d'Ivoire fell by EUR 498 million (-29%), the largest supplier decline, on lower volumes of cocoa beans (-24%) and of cocoa paste, butter, and powder (-25%). Cameroon fell to EUR 202 million (-46%) on beans. On the export side, the EU re-sells processed cocoa, and that fell too: exports of coffee, tea, cocoa, and spices dropped EUR 350 million (-16%), the biggest export-category decline, on lower volumes (-21%) and prices (-17%) of cocoa paste, butter, and powder. The same price signal runs through the June El Niño advisory, where NOAA put the odds of a very strong event at 63%. Cocoa has come off its peak, but the weather risk that drove the original spike has not gone away.

Pigmeat keeps losing on price; fruit and nuts hold up

Pigmeat exports fell by EUR 267 million (-13%), almost entirely due to lower prices (-12%) rather than volume, consistent with its steady loss of global share to lower-cost competitors. Preparations of fruit, nuts, and vegetables also fell by EUR 203 million (-10%), mainly on volume.

A few categories rose. Fruit and nut exports increased by EUR 95 million (+8%), led by apples and pears. Non-edible products rose by EUR 77 million (+10%) on flax exports to China.

Coffee from Vietnam is the one import that is growing

While cocoa imports collapsed, coffee imports rose. Imports from Viet Nam rose by EUR 214 million (+31%) year-on-year, almost entirely due to larger coffee volumes (+82%). Within the coffee, tea, cocoa, and spices category, coffee imports rose by EUR 199 million (+6% in volume), even as the cocoa component fell. Viet Nam was the only major supplier to post a large increase.

Two other supply stories sit underneath the headline. Imports from Ukraine fell EUR 435 million (-19%) on sharply lower cereal volumes (-30%) and oilseeds and protein crops (-43%). Imports from the US fell EUR 273 million (-11%), mostly on lower soya seed volumes (-23%).

On the product side, imports of oilseeds and protein crops fell EUR 557 million (-18%) and cereals fell EUR 540 million (-30%), the latter on a 62% drop in wheat import volumes. Imports that grew included margarine and other oils and fats (+EUR 150 million, +22%, on coconut oil) and beef and veal (+EUR 130 million, +28%, from Brazil, the UK, and Uruguay), the latter supported by short EU supply and high domestic beef prices.

What the EU actually trades

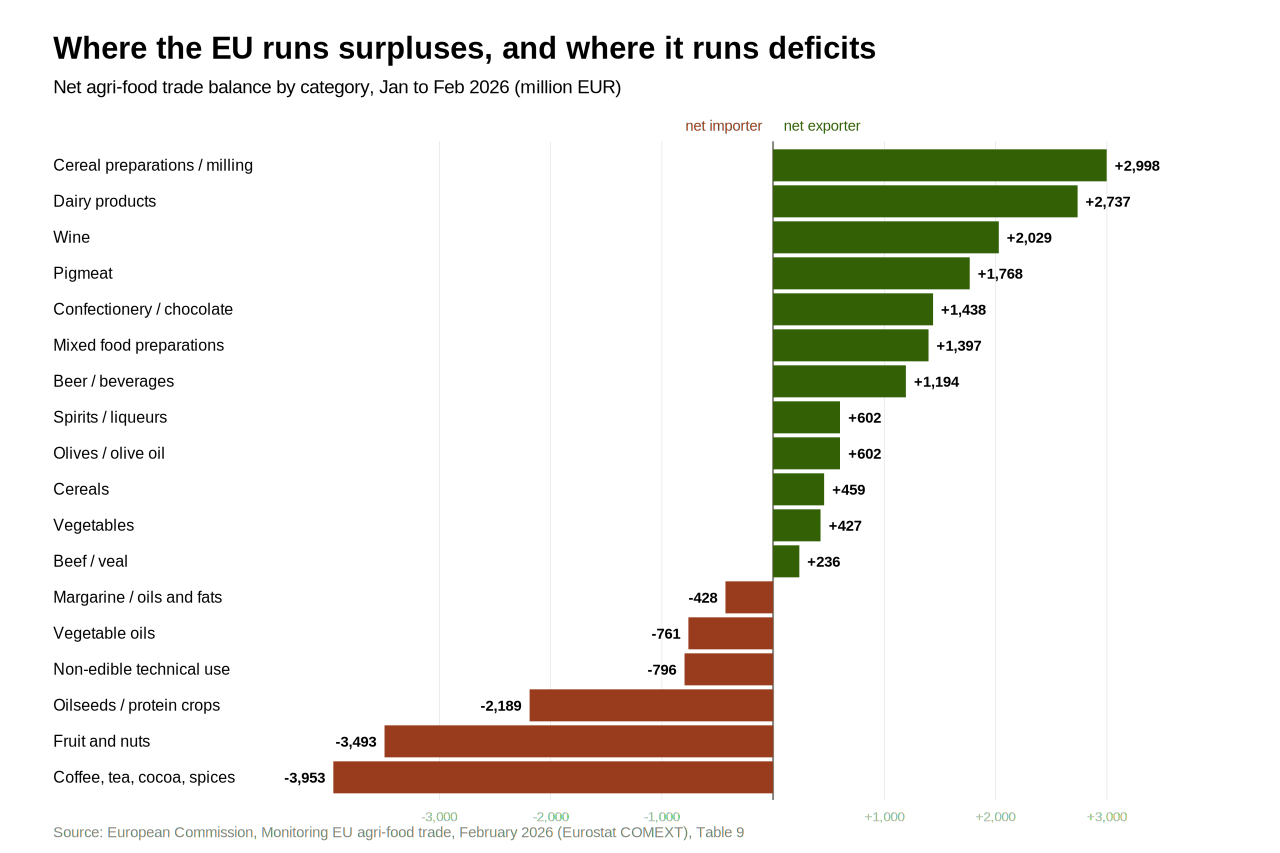

Behind the monthly swings sits a stable structure. The EU is a large net exporter of processed and branded goods, cereal preparations, dairy, wine, pigmeat, confectionery, and runs its deepest deficits in tropical and feed commodities it cannot grow at scale, cocoa, coffee, fruit and nuts, and oilseeds.

That structure explains why a cocoa price move swings the headline surplus so hard. Coffee, tea, cocoa and spices alone ran a EUR 4.0 billion deficit over the two months, and fruit and nuts another EUR 3.5 billion. When the price of a major deficit category falls, the whole balance improves without anything changing on the export side. It also shows where the EU's pricing power sits: the surplus categories are almost all processed or origin-branded, the same up-market lines the long-term outlook identifies as the bloc's growth engine.

What it means for farmers and traders

For olive growers, the 24% fall in EU olive oil export value, with the US singled out, shows the tariff effect in hard numbers rather than forecasts. Producers who sell into the US market should plan for thinner export volumes this year.

For cocoa and chocolate processors, the falling bean price is relief after two punishing years, but it rests on a weather outlook that could reverse if El Niño strengthens through the second half of 2026.

For cereal and oilseed traders, the collapse in wheat and soya import volumes points to ample domestic and Black Sea supply pressing on prices, the same dynamic squeezing grain margins across the bloc.

For anyone reading the surplus number, the lesson is to read past it. The strength in February is mostly cheaper imports and a structural deficit getting smaller, not a stronger export performance, and the export side just lost a fifth of its US business.

References

- European Commission (2026). Monitoring EU agri-food trade developments in February 2026. DG Agriculture and Rural Development, Brussels.

- European Commission (2025). EU agricultural outlook 2025-2035. DG Agriculture and Rural Development, Brussels.

")