")

The global fresh sweet cherry market is experiencing a pivotal period in 2024-2025, characterized by record production levels reaching approximately 5.0 million metric tons globally, yet facing significant regional challenges due to extreme weather events. While overall production shows modest growth of 1.4% year-over-year, the market is witnessing unprecedented price volatility driven by frost damage across major European producing regions and supply chain disruptions. The cherry market, valued at USD 62.50 billion in 2023, is projected to grow at a CAGR of 7.3% through 2030, driven by increasing health consciousness and strong demand from Asian markets, particularly China.

Global Production Analysis 2024-2025

Production Outputs 2025

Global cherry production in the 2025 season is forecast to reach 5.0 million metric tons, representing a slight increase from the previous year despite significant challenges in key producing regions especially in Europe. The production landscape is dominated by Turkey, which maintains its position as the world's largest producer with 900,000 metric tons, followed by China at 850,000 metric tons.

Regional Production Challenges

Severe weather-related production losses across Eastern Europe and Turkey have marked the 2025 season. Ukraine faces catastrophic losses of 45-55% of its sweet cherry crop due to spring frosts, while Poland experienced losses of up to 80% in certain regions. Turkey's cherry production, while maintaining favorable conditions, is projected down 48,000 tons to 900,000 tons as this year's weather cannot match the exceptional conditions of 2023.

In Greece, the 2025 cherry harvest has been devastated by extreme weather events, with yields reportedly down by as much as 80% compared to normal years. The devastating impact is attributed to severe frost between March 19 and 21 during peak cherry tree blossoming, when temperatures plummeted to -7°C to -4°C in key producing areas in Central Macedonia.

Southern Hemisphere Production

Chile is the dominant Southern Hemisphere producer and the world's leading cherry exporter, accounting for over 50% of global cherry exports. The country achieved a record export of 625,000 tons in 2024, marking a 50% increase compared to the previous two seasons. Chilean cherry exports generated USD 3.57 billion in 2024, surpassing the value of Argentine exports.

Argentina is developing ultra-early cherry varieties in Jujuy province, potentially shifting harvest windows to late September, several weeks ahead of traditional Southern Hemisphere production.

Seasonality and Supply Dynamics

China, Chile, the European Union, and the United States are driving the growth of cherries production, with favorable conditions in most regions offsetting local declines. The season is fulfilled through a combination of sequential harvests in the Northern and Southern Hemispheres, ensuring near year-round supply for major markets. For example, North America’s cherry season runs from late spring through summer, with British Columbia extending the supply window into early autumn. The Southern Hemisphere, led by Chile, takes over from late autumn through winter, ensuring continuous availability for global consumers.

Price Analysis by Market Level (2025)

Farmgate Prices

In 2025, the cherry market is experiencing significant volatility, particularly in key producing regions of Europe and Turkey, where severe frosts in April drastically reduced harvests. Turkey, one of the world’s leading cherry producers, expects farmgate prices to be 75% higher than normal, likely averaging between 3.00 and 5.00 EUR/kg, due to a 50–70% harvest reduction. This sharp price increase is especially notable for top export varieties during the peak season.

In Eastern Europe, the impact of frosts has been similarly devastating. Russia has seen its cherry harvest decline by 40–50%, with farmgate prices projected to double or more, reaching 1.90–4.70 EUR/kg or higher. Poland, another major producer, is also facing higher prices, with farmgate rates expected to range from 2.50 to 4.00 EUR/kg due to local supply shortages.

Greece has been among the hardest-hit regions in Europe. Early in the 2025 season, farmgate prices in Greece soared to 5.00–6.00 EUR/kg due to extreme supply shortages caused by frost damage. As the season progresses and other regions begin harvesting, these prices may stabilize or decline slightly.

Elsewhere in the European Union, countries such as France, Spain, and Italy are anticipating farmgate prices in the 3.00–4.00 EUR/kg range. Early-season spikes are possible due to limited supply, but prices are expected to stabilize as more cherries reach the market. Uzbekistan, another significant producer, is seeing stable prices between 2.50 and 4.00 EUR/kg, with increased demand for processing cherries from Europe.

Export-focused regions outside Europe are experiencing more stable conditions. In the United States, farmgate prices are expected to remain in the 2.30–3.20 EUR/kg range, supported by strong export demand and fewer weather disruptions. Chile continues to benefit from robust export demand, particularly from China, and maintains stable farmgate prices of 2.00–3.00 EUR/kg.

China itself, while not a major exporter, is seeing stable farmgate prices with slight upward pressure from rising domestic demand. Prices are anticipated to range from 2.20 to 2.40 EUR/kg.

Overall, the 2025 cherry season is marked by high price volatility in Europe and Turkey, driven by weather-related supply shortages, while export-focused regions like the United States and Chile are experiencing more stable prices due to steady production and strong international demand. The market outlook suggests that weather events will remain a critical factor influencing farmgate prices across the top-producing regions.

Wholesale Prices

European markets, particularly France and Germany, show the highest price variability and premium levels for cherries, especially for large and premium-sized fruit. Rungis, France, offers cherries at 5.23–11.86 EUR/kg, reflecting both early and late season price ranges for large and premium varieties. Germany’s wholesale prices for imported large-fruit cherries range from 7.34–10.33 EUR/kg, with Turkish cherries commanding the highest price, likely due to quality and limited supply. Madrid, Spain, and Bologna, Italy, maintain strong prices, with Bologna’s early and premium cherries fetching 5.00–10.00 EUR/kg and Madrid at 6.44 EUR/kg, indicating robust demand and the impact of weather on local supply.

Outside the EU, the United States and China show more moderate prices, with the US ranging from 3.20–7.70 EUR/kg and China’s top-grade (32mm) cherries at 5–10 EUR/kg wholesale. The US benefits from stable production and strong export demand, while China’s prices reflect a combination of domestic production and imports, with oversupply in some periods leading to price pressure. Uzbekistan stands out with the lowest wholesale price at 1.22 EUR/kg, likely due to local market conditions and limited export orientation.

Greece, despite production challenges from frosts, maintains wholesale prices in Athens at 4.50–5.00 EUR/kg, which is relatively high for the region but lower than some other European markets. This suggests that while supply shortages have pushed up prices, the market has not seen the extreme volatility observed in some other countries. Overall, the data highlights the strong influence of size, quality, and origin on wholesale prices, with large and premium cherries from Europe commanding the highest values, while non-EU markets are more price-competitive but still subject to demand and supply fluctuations.

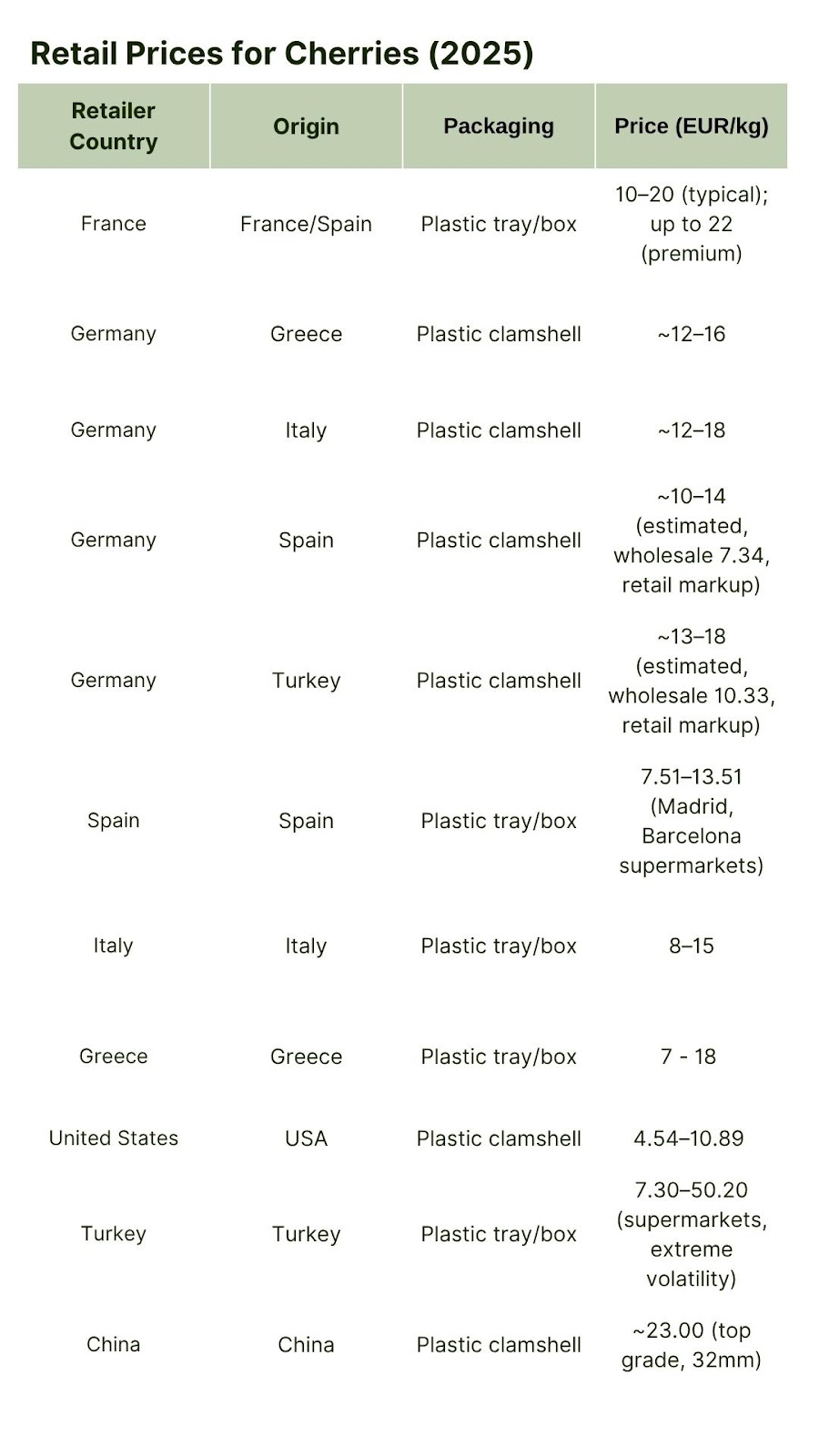

Retail Prices

Retail cherry prices in 2025 have shown dramatic increases in many regions, especially in Europe, due to severe weather-related supply shortages and increased operational costs. In France, Spain, and Italy, supermarket prices for cherries typically range from 8 to 20 EUR/kg, with premium and early-season varieties commanding the highest prices. In Greece, the combination of a poor harvest and logistical challenges has led to retail prices soaring to 18 EUR/kg on islands and in select supermarkets, making cherries a luxury item for many consumers.

Outside the EU, the United States maintains relatively moderate retail prices, with supermarket cherries selling for 4.54–10.89 EUR/kg, reflecting stable domestic production and strong supply chains. Turkey, however, has experienced extreme volatility, with retail prices ranging from 7.30 to over 50 EUR/kg in major supermarkets, driven by a dramatic reduction in harvests and strong local demand. In China, top-grade cherries retail for as much as 23 EUR/kg in Shanghai supermarkets, highlighting the premium value placed on large, high-quality fruit, while Uzbekistan’s retail prices remain very low at around 1.50 EUR/kg, reflecting abundant local supply.

Packaging for retail cherries is predominantly plastic clamshells or trays, which help maintain freshness and extend shelf life. The wide price gaps between regions are influenced by factors such as weather, supply chain efficiency, and market demand, with countries experiencing supply shocks facing the highest retail markups. Overall, the 2025 cherry market demonstrates how sensitive retail prices are to production disruptions and logistical challenges, making cherries a highly variable and sometimes luxury product in global retail markets.

Market Trends

The robust expansion of the global cherry market is underpinned by rising health consciousness, increased disposable incomes, urbanization, and government support for the industry. The Asia-Pacific region, led by China, is expected to be a key driver of growth, contributing 36–38% of the global market expansion, with China itself being both a top producer and importer of cherries.

Trends shaping the market include:

- Growing Demand for Organic and Premium Varieties: Consumers are increasingly seeking organic and sustainably produced cherries, leading growers to adopt new farming practices and expand the range of premium varieties available.

- Technological Advancements: Precision farming, automated irrigation, and improved crop management are enhancing efficiency, yield, and fruit quality, helping producers meet rising demand and mitigate climate risks.

- Expansion of Online and Emerging Markets: E-commerce is making cherries more accessible, while producers are targeting emerging markets in Asia and Latin America for growth.

- Rising Exports: Major producers such as the United States, Turkey, and Spain are increasing exports to meet international demand, leveraging competitive advantages in production and logistics.

- Adaptation to Climate Change and Weather Extremes :Cherry producers are investing in protective infrastructure such as multifunctional plant covers and advanced irrigation systems to safeguard crops from frost, hail, and excessive rain. These adaptations are critical for maintaining production levels and stabilizing supply in the face of increasingly unpredictable weather.

The Rise of Next-Gen Premium Cherry Varieties

Several new premium cherry varieties are being developed and introduced globally to meet evolving market demands for superior flavor, appearance, size, shelf life, and climate resilience. These innovations are reshaping the industry and allowing growers to capture higher prices and expand market opportunities.

Breeders are prioritizing cherry varieties that ripen earlier or later than traditional types, aiming to extend the market window and secure premium prices at both the start and end of the season. For instance, California breeders have introduced early-ripening varieties designed to withstand heat and reduced winter chill, enabling growers to harvest before most competitors and command a market premium.

Leading the charge in low-chill cherry innovation is International Fruit Genetics (IFG), which has developed a suite of trademarked varieties such as Cheery Cupid (IFG Cher-ten), Cheery Nebula, and Cheery Chap. These cherries are specifically bred for regions with mild winters and are now being commercialized in Spain, Chile, California, Australia, and South Africa. Cheery Cupid, for example, is noted for its heart shape and robust sweet-tart flavor, and is performing exceptionally well in test locations. IFG’s low-chill varieties, which require less than 300 chill hours, are helping to expand cherry production into new geographical areas and extend the global harvest calendar.

In the Pacific Northwest, varieties like Coral Champagne, Skeena, Rainier, and newer selections such as Strawberry Cherries and the Pearl Series are gaining popularity. These varieties are bred for unique flavor profiles, larger fruit size, and improved shelf life, with a focus on self-fertility, high yields, and distinctive taste and appearance to differentiate products in the marketplace.

Italy’s University of Bologna is also making significant contributions with its Sweet Series, a portfolio of new cherry varieties developed through an extensive breeding program. These varieties are being patented and trademarked for their improved sweetness, consumer appeal, and resilience to cracking, as well as their suitability for modern, intensive orchard systems. The Sweet Series is designed to cover a broad picking window, ensuring consistent quality and supply throughout the season.

Chile, the world’s largest cherry exporter, is investing in its own breeding programs to develop early and late sweet cherry varieties tailored to local conditions. The focus is on post-harvest quality to maintain fruit integrity during long-distance export, particularly to Asia. Chile’s INIA-Biofrutales Cherry Genetic Improvement Programme has advanced several promising selections, including a bi-color Rainier-type variety with excellent post-harvest characteristics, which could further strengthen Chile’s position in global markets.

These new premium varieties are helping growers meet consumer demand for sweeter, larger, and more visually appealing cherries, while also addressing climate resilience, productivity, and market timing. The trend is toward proprietary and branded varieties that can command higher prices and strengthen brand recognition in both domestic and international markets, setting the stage for continued growth and innovation in the global cherry industry.

Conclusion

The 2024–2025 global fresh cherry market stands at a critical juncture, shaped by a blend of record production levels and mounting regional challenges. Despite modest global growth, the season has been heavily impacted by severe weather events—especially in Europe—triggering sharp supply shocks and historic price volatility across farmgate, wholesale, and retail levels. Regions such as Greece, Turkey, and Eastern Europe have faced devastating frost damage, while producers in the Southern Hemisphere, led by Chile, have capitalized on favorable conditions and robust export demand.

Amid these disruptions, consumer demand continues to strengthen, fueled by rising health awareness, premiumization trends, and expanding market access—particularly in Asia. The evolution of the market is increasingly defined by innovation: from climate-resilient and low-chill cherry varieties to advancements in precision agriculture and logistics.

Looking ahead, the cherry market is poised for continued expansion, but success will depend on the industry’s ability to manage climatic risks, meet quality expectations, and remain responsive to shifting global demand. Strategic investment in breeding, sustainability, and market diversification will be essential to ensure long-term resilience and profitability in the global sweet cherry supply chain.

Discover more about the fresh market

Deep dive in tomato prices: A comprehensive price study 2024-2025

Sources

-

https://www.fas.usda.gov/data/european-union-stone-fruit-annual-3

-

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX%3A31990R1170

-

https://apps.fas.usda.gov/psdonline/circulars/stonefruit.pdf

-

https://extension.oregonstate.edu/catalog/pub/pnw-604-sweet-cherry-cultivars-fresh-market

")