")

The 39 countries that suffered food crises driven by extreme weather between 2016 and 2022 received an average of USD 21.71 per person per year in climate-related development finance. Every other country received USD 40.21. The places most exposed to climate-driven hunger got roughly half the per-capita support of places that were not in crisis. That inversion sits at the centre of a recent FAO analysis of climate finance for food crisis prevention, and it matters because for many of these countries development finance is the main source of climate finance available, with little else to fall back on.

The gap is widest exactly where the need is greatest. Of those 39 crisis-hit countries, 28 are in Africa, many in protracted crisis lasting four years or more. When funding is measured per head, the crisis group consistently trails, and the divergence is sharpest for mitigation finance, where crisis countries received USD 7.09 per capita against USD 17.69 elsewhere. It persists for adaptation too, USD 11.73 against USD 16.18. The report calls this a clear sign of serious misalignment between where climate money goes and where climate shocks land.

Key takeaways

- Crisis countries get about half the per-capita finance. The 39 weather-driven crisis countries averaged USD 21.71 per person a year against USD 40.21 for everyone else, with the widest gap in mitigation funding.

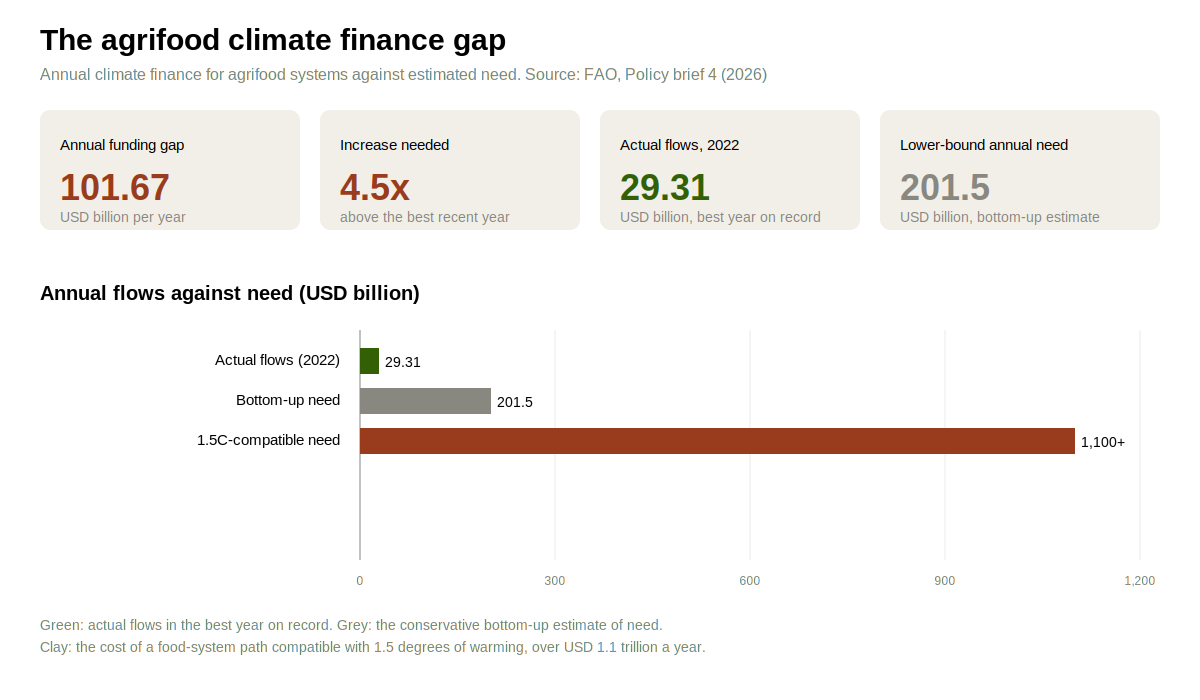

- The agrifood funding gap is roughly USD 101.67 billion a year. Closing even the lowest estimate of need would require climate finance for agrifood systems to rise at least 4.5 times above its best recent year.

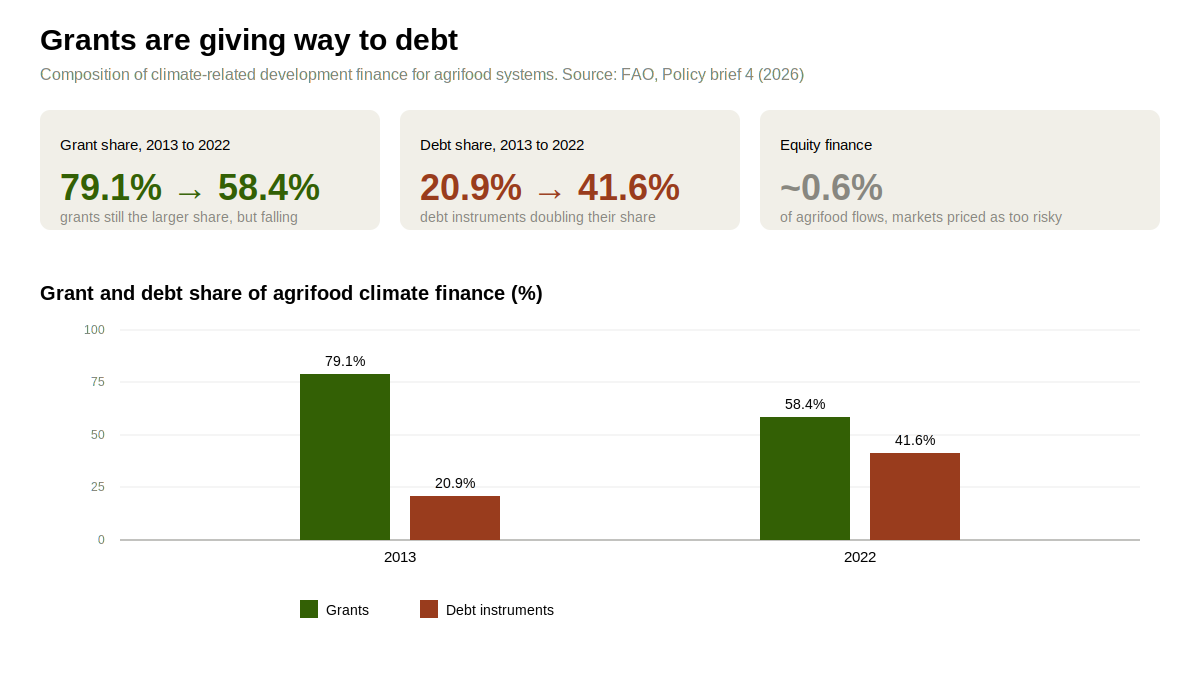

- Grants are giving way to debt. The grant share of agrifood climate finance fell from 79.14% in 2013 to 58.44% in 2022, while debt instruments climbed from 20.86% to 41.56%, a concern for countries with limited ability to borrow.

- Africa carries most of the need. 28 of the 39 crisis countries are in Africa, yet development finance, while better aligned than private flows, still falls short of the regional pattern of need.

- Weak national plans hold back funding. All 39 crisis countries have submitted Nationally Determined Contributions, but only 18 have published National Adaptation Plans, and few break needs down by sector.

Why food systems sit at the centre of the problem

The case for spending on agrifood systems is not in dispute. The way the world produces, processes, transports and wastes food accounts for roughly one-third of net greenhouse gas emissions, with the IPCC putting the food system's share between 21% and 37%. Climate change is already a primary driver of acute hunger, and without faster adaptation, crop yields could fall by up to 10% by 2050 and up to 25% by 2100. Investment in climate-resilient crops and farming systems addresses both the cause and the consequence at once.

The money has grown, but from a low base relative to what is required. Climate-related development finance for agrifood systems averaged USD 17.63 billion a year over 2013 to 2022 and reached USD 29.31 billion in 2022, almost three times the 2013 level. The agrifood share of total climate finance kept falling even so, because funding for other sectors such as transport grew faster. Against the scale of the task the totals remain small. Putting food systems on a path compatible with 1.5 degrees of warming would cost over USD 1.1 trillion a year, while a more conservative bottom-up estimate based on countries' own national plans still comes to USD 201.5 billion annually. Actual flows were around USD 28.5 billion in 2019/2020.

A funding gap that would take a 4.5-fold increase to close

The shortfall is stark once needs and flows sit side by side. The report estimates a funding gap of roughly USD 101.67 billion per year for agrifood systems development. Meeting even the lowest estimate of what is needed would require climate finance for agrifood systems to increase at least 4.5 times over its best recent year. This is a different order of commitment, not a marginal adjustment to existing budgets.

Part of the misallocation is regional. Independent tracking by the Climate Policy Initiative finds that sub-Saharan Africa and South Asia, the regions most vulnerable to climate impacts on food and agriculture, receive only 16% and 5% of total climate finance respectively, far below their exposure. Development finance specifically does somewhat better than the wider picture, directing 30.19% of its agrifood flows to sub-Saharan Africa, which suggests public concessional money is partly compensating for private capital's reluctance to enter high-risk markets. That distinction matters for agrifood systems development. Where private investors stay away, public finance does the heavy lifting, and pulling it back would leave the largest hole precisely where alternatives are thinnest.

The shift from grants to debt

The composition of agrifood climate finance changed over the decade in a way that should concern anyone watching low-income countries' balance sheets. Grants fell from 79.14% of the total in 2013 to 58.44% in 2022, while the share carried as debt instruments climbed from 20.86% to 41.56%.

For countries with limited capacity to service debt, many of them already in protracted crisis, loading more climate finance onto borrowing is a fragile basis for long-term resilience. The report argues for alternatives that create fiscal space rather than consume it, including concessional finance on softer terms and debt swaps that convert repayment obligations into domestic climate and nature investment. Equity finance, which would share risk rather than add to liabilities, has stayed almost negligible at around 0.6% of agrifood climate flows, because investors price these markets as too risky.

The capacity gap behind the numbers

The funding gap is not only about donor priorities. It is also about whether countries can plan, attract and absorb finance in the first place. National plans turn climate ambition into costed, fundable projects, and most of the crisis countries' plans are not detailed enough to do that job. All 39 have submitted Nationally Determined Contributions, but only 18 have published National Adaptation Plans, and fewer still break their needs down by sector or activity. Without that detail, a government struggles to show a financier exactly what needs funding, and struggles to track whether money already received is closing the gap.

The country cases make the scale concrete. Nepal's National Adaptation Plan puts the average annual financing need for its agriculture and food security programme at USD 631.7 million, and climate-related development finance covered only about a quarter to a third of that. Zimbabwe's plan implies annual needs of USD 596.3 million for agriculture, against which actual flows met less than 10%. These are rough figures, and the report is candid about the difficulty of matching donor data categories to national plans, but the direction is unmistakable.

What would change the picture

Closing a gap of this size on grants and concessional finance alone is unrealistic, which is why the report points to mobilising private capital as the larger prize. Private investors hold over USD 410 trillion in financial assets globally, with USD 16 trillion in developing countries, and shifting even 1% toward climate and development goals would dwarf current public flows. The instruments to attract it exist, including blended finance, green and sustainable bonds, political risk insurance and debt-for-climate swaps, and concessional public money can be used to lower the risk that keeps private capital out. These tools need stable macroeconomic conditions and developed financial markets to work, which many of the poorest countries cannot yet offer, so technical support to build that foundation is itself part of the solution.

Three priorities follow for the institutions that allocate this money. Concessional flows should be redirected toward the most vulnerable and crisis-prone countries, where development finance is often the only climate finance available and the impact per dollar is highest. The drift toward debt needs careful monitoring, with grants, concessional terms and swaps favoured for low-income countries that cannot safely borrow more. And planning capacity deserves investment, through better national plans and clearer climate finance data, so that countries can make their case and funders can track results. The logic is the same one that drives climate-smart agriculture at the farm level. Resources do the most good when matched to where the pressure is, and right now, for food security in the countries that need it most, they are not.

")