")

Fresh Market Digest – Week 17, 2026

The European strawberry market has reached its lowest point of the 2026 campaign. Wholesale data from Mercamadrid, Rungis, Germany’s BLE benchmark, and Greece's OKAA market show that abundant Spanish volumes are pushing prices down, while newly arrived northern European fruit is establishing a clear premium.

Stay up to date with our weekly Fresh Market Digest

Spain's Mercamadrid

In Spain's wholesale market, strawberry prices opened the year at €8.00/kg in week 1 driven by limited early supply. By week 6, prices had compressed to €3.90/kg as Huelva volumes ramped, before a brief Easter-related rally pushed them back to €4.50/kg in weeks 8 and 12. Since then, the trajectory has been downward, now €2.50/kg in week 17.

.jpg)

This represents a 69% decline from the January peak and a 44% drop over the last five weeks alone, a very steep late-campaign correction. In the first months of the season, production was low, and now there is an abundant supply at very low prices. The 2026 campaign started late and short on volume after cold, rain, and wind hit the Huelva planting window, and by the time volumes recovered, the market window had narrowed, and supply is now arriving at exactly the moment northern European origins are beginning their own campaigns.

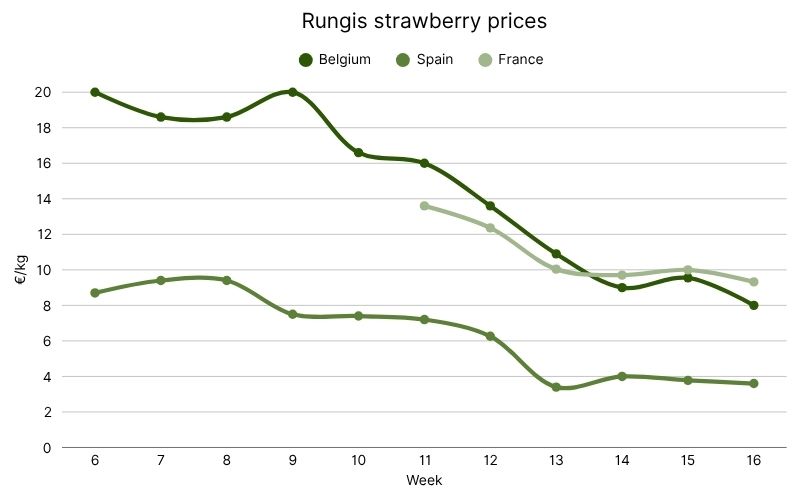

France’s Rungis International Market

The French Rungis market clearly captures the premium trend. Across weeks 6–16, the three tracked origins have diverged sharply:

Belgian fruit, the premium anchor, opened at €20/kg in week 6 and, after briefly touching €20 again in week 9, began a steep descent to €8/kg by week 16. That 60% decline reflects both seasonal compression and the arrival of French domestic volumes from week 11 onwards, which capped the Belgian premium.

French fruit entered the Rungis market in week 11 at €13.60/kg and settled at €9.40/kg by week 16, still commanding a meaningful premium over Belgium in the final weeks, a function of freshness, a short supply chain, and French marketing positioning.

Spanish fruit never exceeded €9.50/kg this season and closed week 16 at €3.60/kg, less than half the Belgian price and about 40% of the French price. The Spain-France spread has widened to nearly €6/kg, showing origin segmentation.

Germany's Federal Office for Agriculture & Food (BLE)

The German BLE benchmark shows six distinct strawberry origins, which split cleanly into two groups.

.jpg)

Mediterranean origins decrease. Spanish fruit peaked around €7/kg in weeks 6–9 and has since fallen to €3.20/kg in week 16, with a low of €2.90/kg in week 14. Italian fruit, which had held the top of the Mediterranean band at €8/kg in weeks 7 and 9, has fallen to €4.60/kg. Greek fruit, the price leader in early winter weeks, has dropped to €3.60/kg. All three are now competing in a narrow €3.20–4.60/kg band, and Spanish fruit is setting the floor.

Northern origins establish the premium. The market changes entirely when Dutch fruit enters in week 12 at €8.10/kg. German domestic fruit traded at €8.50/kg in week 14. Belgian fruit enter in week 15 at €8.50/kg, then quickly compresses to €6.60/kg by week 16. Dutch (€7.70/kg in week 16) and German (€8.40/kg in week 16) are holding their ground firmly.

The gap is now €5/kg between German domestic and Spanish fruit, a premium structure that reflects quality perception, provenance marketing and the strong local soft-fruit demand.

Greece’s Central Market of Athens (OKAA)

The Greek OKAA benchmark behaves very differently from the others.

.jpg)

Prices have bounced: €2.50/kg (wk 12), €2.30 (wk 13), €1.50 (wk 14), €2.20 (wk 15), €1.50 (wk 16), €2.00 (wk 17). The zigzag pattern of 30–40% week-on-week swings is characteristic of a market dominated by domestic supply rather than managed import programmes. When Greek growers have a strong harvest window, prices compress sharply; when rain or labour disrupts the cut, prices rebound quickly. The week 17 reading of €2.00/kg is the lowest strawberry price across the four markets surveyed.

Market outlook

● Spanish market approaching the floor: At €2.50/kg in Mercamadrid, Spanish strawberries are trading close to marginal cost for many growers. However, prices are not bottoming because supply is still high. The key shift will likely be supply-driven: once Huelva volumes begin to drop, the market could rebound quickly. Until then, downside risk remains.

● Premium structure: The €5/kg spread between northern and Mediterranean origins reflects clear market segmentation. Northern fruit is benefiting from freshness, proximity, and strong retail positioning, while Spanish fruit is firmly anchored in the volume segment. Some compression is likely as Dutch and Belgian volumes build through May, but a full convergence is unlikely. A persistent premium for local and northern origins should be expected through the remainder of the campaign.

● Greek volatility: The Greek market remains highly reactive, with sharp week-to-week price swings driven by harvest conditions. If prices stabilize above €2/kg and weather disruptions persist, short export opportunities could open.

Week 17 confirms that Spanish origin is playing a volume role, while northern Europe controls the premium tier. Buyers may move away from single-origin strategies and adopt a dual approach: Spanish fruit for price-driven, high-volume programs and Northern/local fruit for premium positioning and margin protection. The coming weeks will be about managing origin mix as the market remains segmented.

Buy and sell fresh fruit on the Wikifarmer Marketplace and check real-time prices with Wikifarmer’s Price Insights

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")