")

Stone Fruit Market Digest | Week 28, 2026

European stone fruit prices steadied in Week 28 after two weeks of sharp declines, but the peak harvest kept supplies abundant. Peaches, nectarines and flat peaches settled near seasonal lows, while yellow peaches rebounded as higher-quality main-season fruit arrived. Cherries continued to weaken in Spain as late-season volumes reached the market, although wholesale prices strengthened further north as supplies tightened. Plums remained the most stable category, with new origins steadily entering the market.

This report covers stone fruit wholesale activity in four major EU markets: Mercamadrid (Spain), Rungis International Market (France), the Federal Office for Agriculture and Food (BLE) market reporting system (Germany), and Athens Central Market (OKAA) in Greece.

Stay up to date with our weekly Fresh Fruit Market Digests

Mercamadrid prices steady

The rapid declines that characterized the second half of June have begun to ease: Through late June, the Spanish peach complex fell 15–30% per week as peak-season supply overwhelmed demand, but this week those moves narrowed.

Red peaches slipped 7% to €1.70/kg, and nectarines edged 4% lower to €1.78/kg, while flat peaches were stable around €1.68/kg. Yellow peaches moved against the trend, rising 19% to €1.97/kg as their main-season, better-quality fruit arrived.

.jpg)

Cherries

The European cherry season is entering its final phase, with market conditions increasingly shaped by tightening availability rather than expanding harvests.

Spain remains the only major market where prices are still under pressure. At Mercamadrid the most-frequent price dropped to €2.50/kg (from €3.00) on a large late volume of 1,470 tons over seven days, led by Cáceres and Zaragoza. Those late-season volumes continued to outweigh demand.

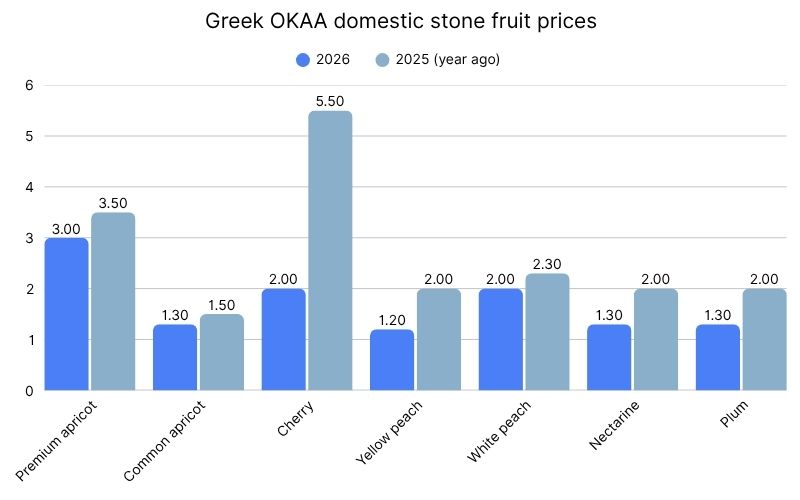

In Greece, domestic cherries held at €2.00/kg, barely a third of the €5.00–5.50 seen a year ago.

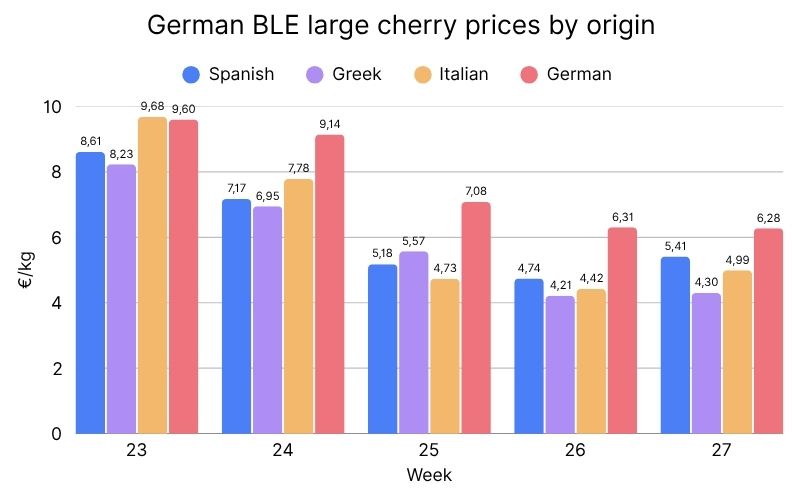

Germany presented a different picture: As Spanish and Italian harvests began to wind down, wholesale prices recovered from June's collapse. Large-fruited Spanish cherries firmed to €5.41/kg (from €4.74), Italian cherries to €4.99/kg (from €4.42), and German cherries held near €6.28, as tightening end-of-season supply supported the market.

At France’s Rungis, the French cherry campaign is finished; the market is now supplied mainly by Belgian fruit, with the last lots selling easily and prices revalued upward on scarcity.

Peaches and nectarines

The seasonal oversupply that weighed heavily on prices throughout June is no more. Although supplies remain plentiful, wholesale markets are no longer experiencing the steep weekly declines seen earlier.

At Mercamadrid, red peaches eased to €1.70/kg, nectarines settled at €1.78/kg, and yellow peaches climbed to €1.97/kg as the transition from early-season production to higher-quality main-season fruit gathered pace.

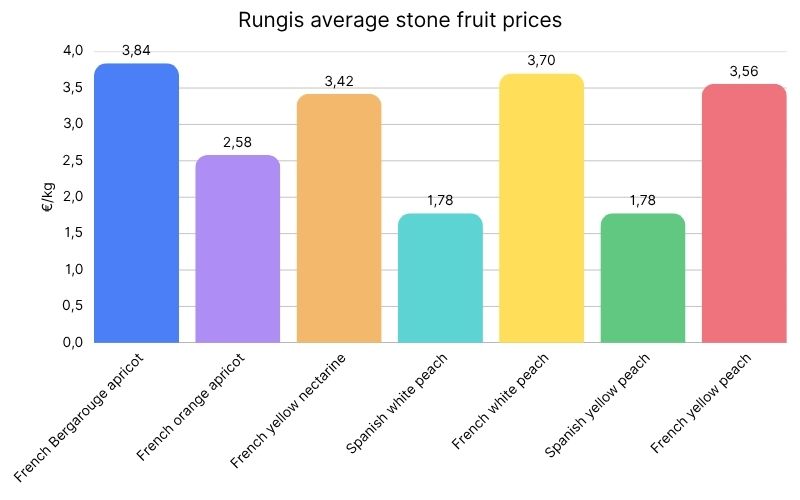

France's Rungis market was also more balanced. French white peach firmed 3.9% to €3.70/kg, yellow peach €3.56 and nectarine €3.42 (+2.4%), with Spanish peaches steady at €1.78. The end of the heatwave and the start of the summer holiday period softened consumer demand but prevented any major market disruption.

Germany continued to rely heavily on Spanish supplies, and quotations changed little. AA yellow nectarines averaged €3.05/kg, while French AA peaches stood at €4.14/kg. Turkish fruit remained concentrated in the lower-priced segment of the market.

Greece held domestic peaches at €1.20/kg and nectarines at €1.30.

Apricots

Apricot prices increasingly reflected differences in origin as production shifted across producing countries.

At Mercamadrid, Spanish common fruit slipped below €2 to €1.98/kg.

Germany's premium market was now led by Turkish fruit at €4.73/kg as its export season reached full pace. German apricots averaged €4.08/kg, followed by French fruit at €3.55/kg, Greek at €3.10/kg and Italian at €3.00/kg. Spanish apricots occupied the lowest-priced position at €2.73/kg.

At Rungis, French apricots remained stable at €2.58/kg, while premium Bergarouge varieties continued to command €3.84/kg.

In Greece, premium apricots held at €3.00/kg, whereas standard fruit eased to €1.30/kg.

Flat peaches and flat nectarines

Flat peaches showed little movement across European wholesale markets.

Paraguayos at Mercamadrid were steady at €1.68/kg on about 522 tons.

German wholesale markets also recorded limited price movement. Spanish and Turkish supplies kept paraguayos close to €2.89/kg, while platerinas (flat nectarines) averaged €3.77/kg.

Plums

Plums are the most stable segment of the stone fruit market as the season expands.

At Mercamadrid the purple plums held at €2.25/kg for a fourth consecutive week, with early strawberry plums at €4.00/kg and dark plums at €2.50, on a combined 460 tons.

The French season also gathered momentum. The first commercial volumes of Allo, Vars and Obilnaya entered Rungis, where balanced supply and demand kept prices firm.

Germany received plums from a widening range of origins, including Spain (€2.72/kg), Italy (€2.51/kg) and Turkey (€3.14/kg).

Greece entered the market with domestic plums at €1.30/kg.

Greece continues to trade well below last year's prices

Greek wholesale prices remain well below the levels recorded during the 2025 season.

Domestic cherries at €2.00/kg are worth only around one-third of last year's price. Peaches (€1.20/kg), nectarines (€1.30/kg) and standard apricots (€1.30/kg) also remain substantially lower year on year.

Only premium apricot grades, at €3.00/kg, are trading close to last season's values. Ample domestic production continues to favour buyers, but margins remain under pressure for growers.

Market outlook

- Prices steadying: Peaches, nectarines and flat peaches have settled around seasonal lows across Spain, while French and German markets have become considerably more stable. Unless weather or demand changes unexpectedly, prices are likely to remain within a relatively narrow range through the coming weeks.

- Yellow peaches increase: The 19% rebound at Mercamadrid signals that main-season fruit is taking over, rather than a supply shortage.

- Cherry season ending: French production has ended, Spanish harvests are entering their final stages, and German wholesale prices have already begun to strengthen as availability tightens. Further upward movement is likely.

- Plums are the growth line: New producing regions are entering across southern and central Europe, prices have remained comparatively stable, and the category is expected to take a more prominent role as other stone fruit seasons wrap up.

Buy and sell fresh fruit on the Wikifarmer Marketplace and track real-time prices with Wikifarmer’s Price Insights

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")