")

EU oilseed imports are set to fall 5.9% by 2035

The European Commission projects a 5.9% decline in net EU oilseed imports by 2035 compared with the 2023–2025 average. For a bloc that currently pulls in more than 12 million tonnes of soya beans and nearly 6 million tonnes of rapeseed every marketing year, that shift carries real consequences for pricing, sourcing, and contract planning across the supply chain.

The drop will not be sudden. It reflects a set of structural changes already underway in EU agriculture, energy policy, and livestock production. Traders who understand which oilseeds are losing ground, which are gaining, and why, will be better positioned than those reading headlines alone.

What is driving the decline in imports

Three forces are converging.

Biofuel demand is contracting. The EU's biofuel sector is expected to grow in the short term but shrink between 2028 and 2035 . Rapeseed oil, the main crop-based biodiesel feedstock in Europe, will bear the brunt. Rapeseed oil use for biofuels is projected to fall 11.2% between 2023–2025 and 2035, as the policy framework shifts toward advanced feedstocks like waste oils. Palm oil use is being phased out almost entirely, with a projected 87.6% drop in biofuel applications.

Feed demand is falling. The EU's livestock sector is shrinking. Pigmeat and beef production are both in decline, and milk yield growth is slowing. Feed use of oilseed meals, particularly soya and sunflower meal, is set to drop accordingly. Improved genetics and feeding efficiency are compounding the effect, meaning fewer imported tonnes per unit of animal output.

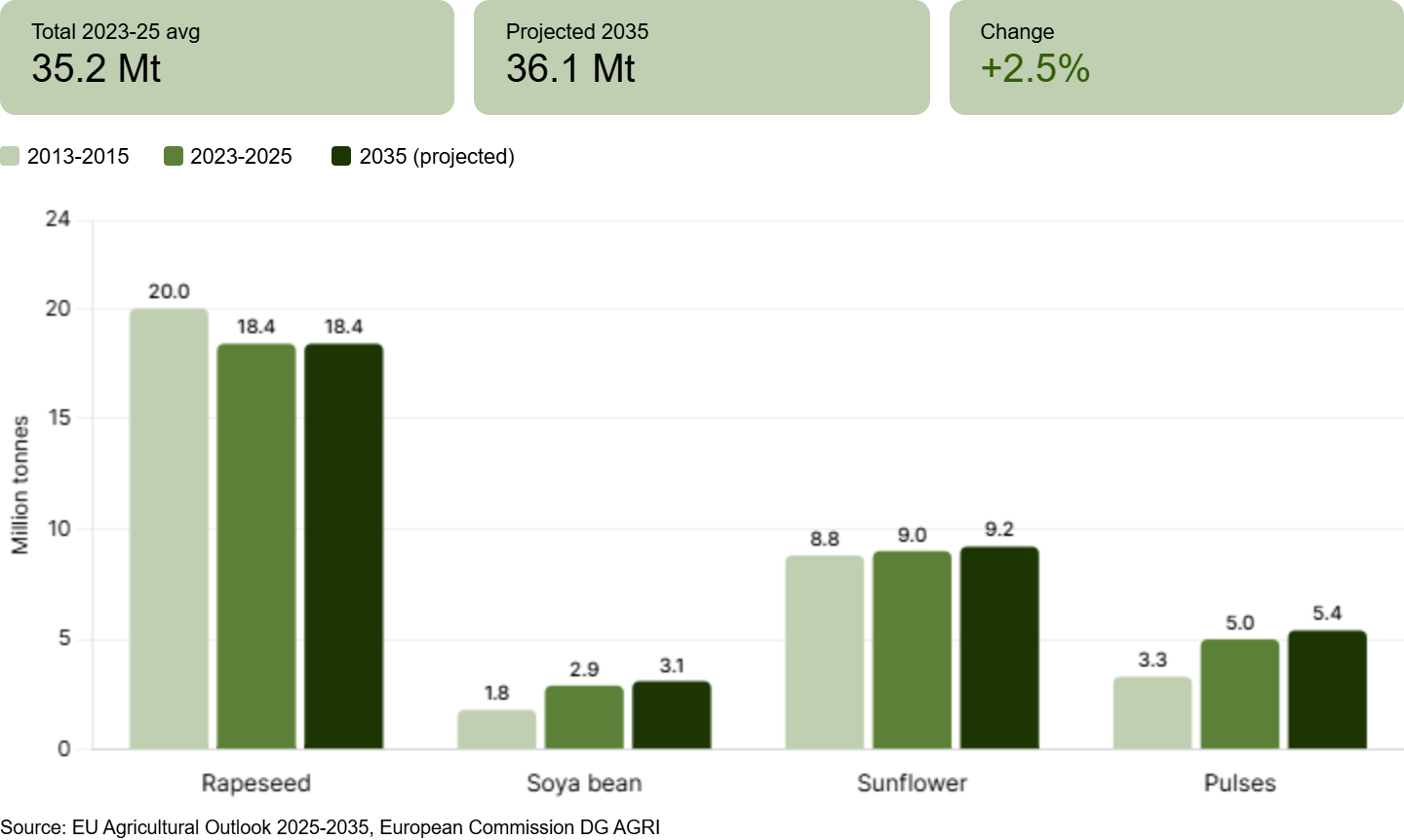

Domestic production is rising. EU oilseed and pulse production is projected to reach 36.1 million tonnes by 2035, a 2.5% increase over the 2023–2025 baseline. Soya bean production is growing at 0.7% per year, sunflower seed at 0.2%, and pulses at 0.8%. EU policy support for plant-based protein production and growing food demand for pulses are the main drivers here.

The three crops are moving in different directions

The headline 5.9% masks very different trajectories for rapeseed, soya beans, and sunflower.

Rapeseed is the biggest loser. EU rapeseed production is projected to flatline at around 18.4 million tonnes through 2035, held back by declining biofuel demand and reduced availability of plant protection products. Crushing volumes are set to fall 5.1% to 22.3 million tonnes. For traders, this means weaker demand for imported rapeseed, with current imports already heavily concentrated from Australia (43.1% of EU rapeseed imports in 2024/25).

Soya beans are holding steady with a slight upside. EU soya bean crushing is projected to grow modestly, reaching 14.5 million tonnes by 2035, a 0.9% increase. Domestic soya production is expanding to 3.1 million tonnes, up from 2.9 million tonnes in 2023–2025. The EU imported 12.18 million tonnes of soya beans in the current marketing year through week 45, with the United States supplying 47%. Soya bean prices are projected to grow 1.6% per year over the next decade, the fastest among the three major oilseed crops.

Sunflower is the growth story. Sunflower seed use in the EU is projected to rise 2.7% by 2035, driven by food demand. Production is expected to increase marginally to 9.2 million tonnes. Sunflower oil imports from Ukraine surged 29% in 2024/25, with Ukraine supplying an extraordinary 94.9% of the EU's sunflower oil imports. That concentration creates obvious supply-chain risk, and any disruption would ripple through vegetable oil markets immediately.

What the current market looks like

The DG AGRI Oilseeds Dashboard for May 2025 captures a market already in transition.

Soya bean export prices (FOB US Gulf) stood at $418/t, down 13% year-on-year. Rapeseed prices at EU Moselle were €487/t, up a modest 5%. Sunflower seed prices at EU Bordeaux hit €594/t, a sharp 36% year-on-year increase. That sunflower premium reflects both the recovery in Ukrainian supply chains and sustained food-sector demand.

On the meals side, soyameal prices collapsed 29% year-on-year to $310/t (FOB Argentina), while rapemeal at Hamburg fell 5% to €268/t. The divergence between seed and meal prices signals that the protein fraction is under pressure from declining feed demand, while oil-side margins are holding better.

Global production is meanwhile surging. World oilseed output reached 692 million tonnes in 2024/25, with soya beans alone accounting for 427 million tonnes. World vegetable meal production hit 395 million tonnes, and vegetable oil production 232 million tonnes.

What this means for sourcing and risk

EU total oilseed stocks are thin at 3.0 million tonnes (2024/25 forecast), split between rapeseed (0.8 million tonnes), soya bean (1.3 million tonnes), and sunflower (0.9 million tonnes). Low stock-to-use ratios leave limited buffer against supply shocks.

Three risks stand out for traders. First, the EU's near-total reliance on Ukraine for sunflower oil creates a single-point-of-failure for the vegetable oil complex. Second, the biofuel policy timeline between 2025 and 2028 creates a short-term demand bump followed by a structural decline, making contract duration and hedging horizon matter more than usual. Third, soya bean sourcing is diversifying (Brazil supplied 50.2% of soyameal imports in 2024/25), but trade policy developments and deforestation regulations could shift flows unpredictably.

-1.png)

The broader signal

The 5.9% import decline is not an isolated statistic. It reflects the EU's agricultural sector becoming slightly more self-sufficient in plant proteins, less dependent on crop-based biofuels, and leaner in livestock production. For commodity traders operating in European markets, the strategic horizon is shifting from volume growth to value positioning. Soya bean prices will likely outpace rapeseed and sunflower over the next decade. Sunflower supply concentration demands active risk management. And rapeseed's structural decline in the biofuel channel will reshape the EU crushing industry over the next ten years.

The traders who build these structural shifts into their forward books now will have an edge when the numbers start appearing in quarterly trade data.

Source vegetable oils with confidence on Wikifarmer's Marketplace:

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

References

- European Commission. (2025). EU Agricultural Outlook for Markets, Income and Environment 2025–2035. DG Agriculture and Rural Development.

- European Commission, DG AGRI. (2025). Oilseeds Dashboard. Last updated 23 May 2025. Sources: DG ESTAT, DG JRC, DG AGRI, IGC, USDA, CME, Euronext.

")