")

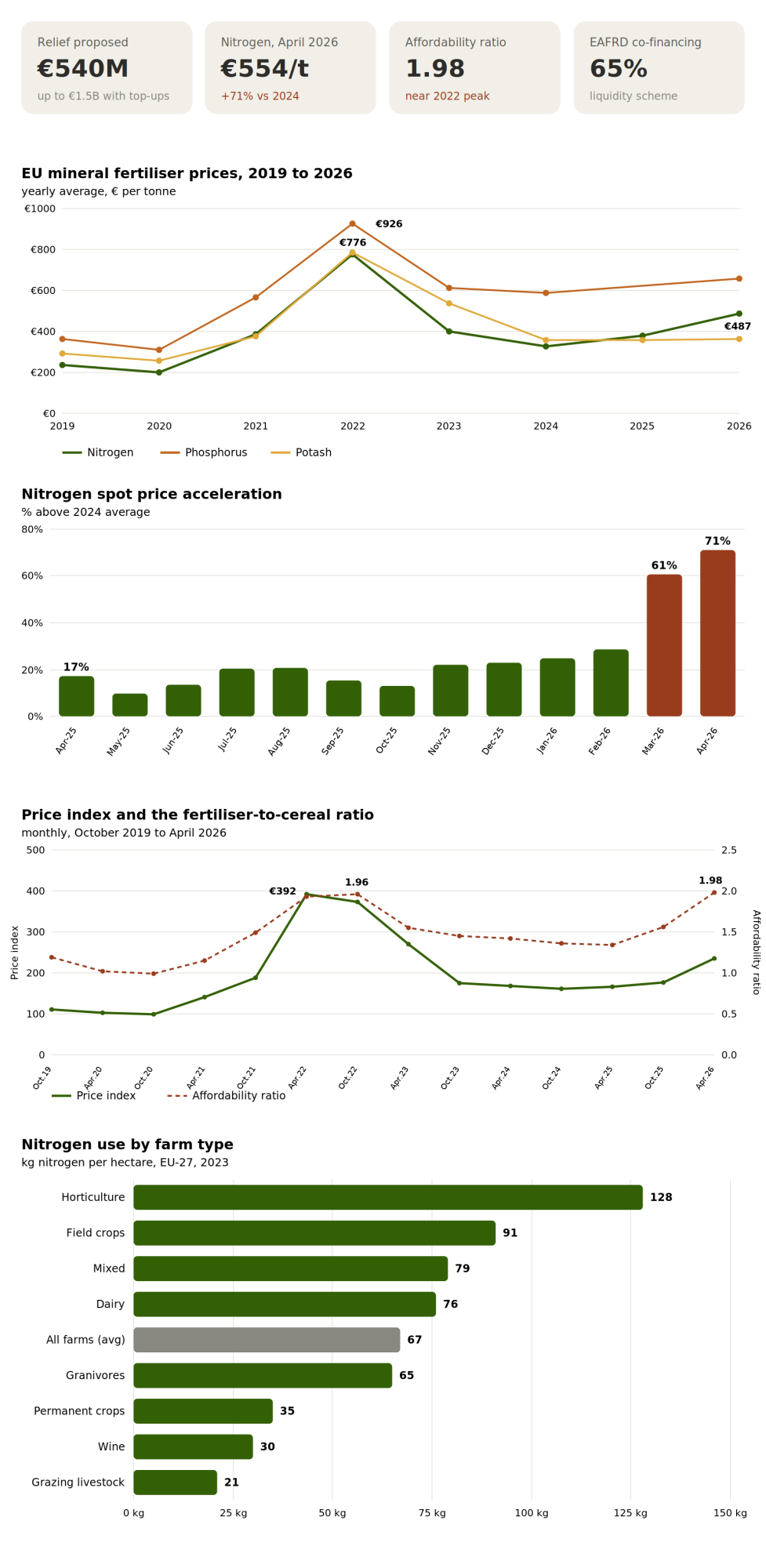

The European Commission proposed a €540 million financial relief package for farmers on 12 June 2026, the first concrete money attached to the Fertilizer Action Plan announced on 19 May. With national co-financing of up to 200%, the total support could reach €1.5 billion. The proposal needs the approval of the member states and the European Parliament, with final adoption targeted for the end of July 2026.

The package responds to a sharp run-up in fertilizer costs. EU nitrogen fertilizer averaged €554 per tonne in April 2026 and €541 in May, the highest monthly levels since the 2022 energy crisis, when nitrogen peaked at an annual average of € 776. Against the 2024 average of €327, current nitrogen prices sit roughly 70% higher. Phosphorus has climbed to €717 per tonne, while potash has held close to €370.

The fertilizer crisis in four figures and four charts. Nitrogen has climbed back toward 2022 crisis levels; the spot price is now 71% above the 2024 average; affordability has fallen to its worst since 2022; and the burden lands hardest on horticulture and field crops. Sources: EU Agri-food Data Portal and Farm Sustainability Data Network (FSDN).

What is the money for

The relief has two parts.

The first is a direct injection into the EU agricultural reserve. The Commission proposed adding €300 million from the 2026 EU budget to the funds already in the reserve. Member states can then top this up with national funds of up to 200%, which brings the headline figure to a potential €1.5 billion. The corresponding national envelopes are specified in the proposal, and the agricultural reserve element is subject to a member state vote in the Committee on the Common Organization of the Markets.

The second part is a set of targeted adjustments to the Common Agricultural Policy to accelerate support to farmers. These are legislative amendments heading to the Parliament and Council.

How the CAP changes work

Three mechanisms are included in the CAP package.

A new liquidity scheme under rural development provides member states with a crisis-support instrument that can be co-financed up to 65% by the European Agricultural Fund for Rural Development. It can absorb unused funds that might otherwise be lost at the end of the programming period, and member states may add national financing of up to 200%. To get money out quickly, support can be paid as a fixed amount per hectare and run through the existing CAP Strategic Plans rather than requiring new administrative structures.

Earlier direct payments are the second mechanism. Member states will be able to pay advances before 16 October 2026 at an increased rate, improving cash flow for farmers heading into the autumn sowing season for the 2027 harvest.

The third is budget flexibility. Member states will be allowed to adjust their direct payment allocations for calendar year 2027, giving them room to respond to the cost pressure within their national envelopes.

The design choice running through all three is speed. Fixed-per-hectare payments, delivery through existing Strategic Plans, and the redirection of unused funds are all aimed at providing relief to farms before the next planting cycle rather than after it.

Why nitrogen specifically

The cost problem is concentrated in nitrogen, and the reason is structural. Nitrogen fertilizer production runs on natural gas, which serves as both the feedstock for ammonia synthesis and the energy to drive it. Natural gas accounts for 70-80% of nitrogen production costs, according to the Commission. When gas prices move or supply tightens, nitrogen follows within weeks.

The immediate trigger was the military escalation in the Middle East from 28 February 2026, which disrupted a region accounting for 20-30% of global ammonia and urea exports, and a key source of the sulfur used in phosphate production. The mechanism by which that disruption transmits to fertilizer prices, and why supply cannot simply scale up to meet it, is set out in our analysis of how the Strait of Hormuz disruption is changing 2026 fertilizer planning.

The price climb is steep when measured month by month. Domestic nitrogen spot prices, expressed as the difference from the 2024 average, ranged from 13% to 23% through most of 2025 before jumping to 28.6% in February 2026, 60.7% in March, and 71.1% in April. The acceleration in early 2026 turned a manageable cost increase into a crisis, prompting the Commission to judge it worth a dedicated relief package.

The affordability squeeze

Price level is only half the story. What matters for farm viability is the ratio between what farmers pay for inputs and what they earn for outputs, and on that measure, the picture is worse than the raw nitrogen number suggests.

The Commission tracks a fertilizer-to-cereal price ratio, with a higher figure indicating that fertilizer is less affordable relative to crop revenue. That ratio reached 1.98 in April 2026, approaching the 2022 crisis peak of around 2.00 and standing at the least affordable level since that year. The squeeze is compounded by lower cereal prices in 2026 compared to 2022, leaving farmers with high input costs without the higher grain prices that partly offset them during the last crisis.

The fertilizer price index tells the same story. After falling from its 2022 peak to a stable band around 160-185 through 2023 to early 2026, it jumped to 235 in April 2026. The combination of rising input prices and soft output prices is precisely the scenario the relief package is designed to cushion.

Which farms are most exposed

Fertilizer use varies widely by farm type, which determines who feels the nitrogen price most acutely.

Horticulture is the heaviest user by a wide margin, applying around 128 kg of nitrogen per hectare in 2023, along with high rates of phosphorus and potassium. Field crops follow at roughly 91 kg of nitrogen per hectare, then mixed farms and dairy at around 79 and 76 kg, respectively. Permanent crops such as vineyards and orchards use far less, in the 30-35 kg range, and extensive grazing livestock, least of all, at around 21 kg. The EU average across all farm types is about 67 kg of nitrogen per hectare.

For arable and horticultural operations, fertilizer is one of the largest single input costs, representing 24% of intermediate inputs and 16% of total inputs for arable crop farmers in 2023, according to the Commission's Farm Sustainability Data Network figures. These are the farms the relief is principally aimed at, and the ones where the nitrogen price spike does the most damage to margins.

How does this fits the broader plan

The €540 million is the short-term, emergency leg of a larger structure. The full EU Fertilizer Action Plan, adopted on 19 May, pairs this kind of immediate relief with longer-term measures intended to reduce Europe's dependence on imported mineral fertilizers altogether, through domestic production support, a push toward bio-based and circular nutrients, and changes to nutrient regulation.

The relief package is explicitly framed as a bridge to those structural measures rather than a standalone fix. The Commission's position is that getting farmers through the 2027 sowing season is the precondition for the longer transition to work, since farms under acute cost pressure cannot also invest in the efficiency and substitution measures envisaged by the plan.

What happens next

The two halves of the proposal move on separate tracks. The agricultural reserve top-up will be put to a member state vote in the Committee on the Common Organization of the Markets, with adoption targeted for the end of July. The CAP legislative amendments go to the European Parliament and Council, with the Commission calling for them to be treated as urgent.

For farmers, the practical questions are national. How much each member state adds on top of the EU money, how quickly national authorities implement the per-hectare payments, and whether the earlier advance payments arrive before autumn sowing will determine how much the package actually relieves. The EU framework sets the ceiling and the mechanism. National implementation decides the delivery.

The next confirmation point is the end-of-July adoption vote. If the agricultural reserve top-up clears at the proposed level and member states commit national co-financing, the relief reaches farms during the 2026 autumn sowing window. If it slips, the support arrives after the planting decisions it was meant to support have already been made.

References

- European Commission. (2026). Commission proposes €540 million in financial relief and other supports for farmers facing fertiliser crisis. Press release IP/26/1348, 12 June 2026.

- European Commission. (2026). Fertiliser Action Plan: Partnership for ensuring the availability, affordability and strategic autonomy in home-grown EU fertilisers. COM(2026) 310 final, 19 May 2026.

- European Commission. (2026). Ensuring availability and affordability of fertilisers. DG Agriculture and Rural Development.

- EU Agri-food Data Portal / Fertilisers Market Observatory. (2026). Fertiliser prices, affordability and consumption data. DG Agriculture and Rural Development.

")