")

Focus on Oils | April 2026

March has brought contrasting conditions across global edible oil markets. Mediterranean olive oil origins are entering a wait-and-see phase as flowering begins and operators closely monitor conditions for the 2026/27 crop. Rapeseed remains stable on strong production expectations and steady industrial demand, while sunflower oil is trading firmer under geopolitical risk linked to Black Sea and Middle East tensions. Avocado oil, meanwhile, is softening under peak Peruvian supply, with further seasonal shifts expected later in the year as Mexican production ramps up.

Stay up to date with our Weekly Olive Oil Market Digest

Olive oil market

Mediterranean origins are in a holding pattern as harvests have concluded, stocks are drawing down faster than buyers expected, and attention has shifted to the flowering window that will set the tone for the 2026/27 campaign.

Spain’s olive oil market

Spain’s 2025–2026 olive oil campaign was solid overall, though final production fell short of the Ministry of Agriculture’s (MAPA) initial expectations. As of the end of April, cumulative production stood at 1,294,590 tonnes, 5.6% below MAPA’s revised forecast of 1,371,938 tonnes due to weather-related impacts. Production is also approximately 9% lower than last year’s total.

-1.jpg)

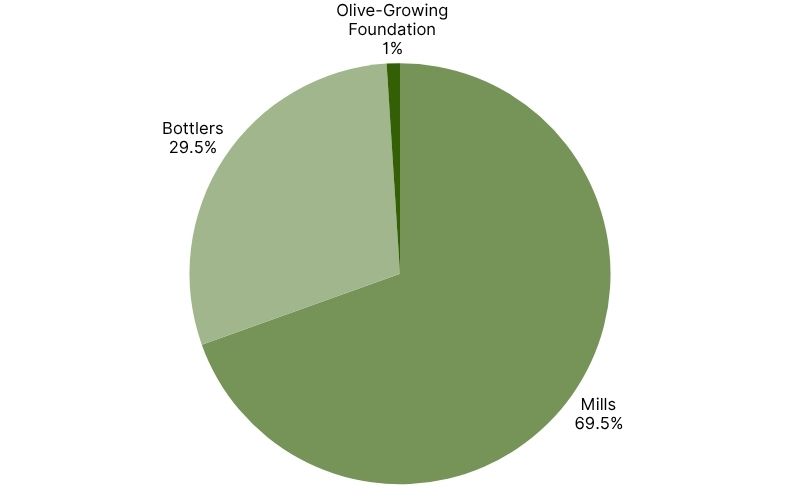

Stock levels heading into the summer are lower than many operators had anticipated. Total stocks at the end of April stood at 863,339 tonnes, down 76,964 tonnes from March. Of this, 600,270 tonnes were held by mills, representing a 13.3% monthly decline, while bottler inventories rose 6.8% to 254,325 tonnes. Stocks held by the Olive-Growing Heritage Foundation fell 8.9% to 8,744 tonnes. With well over half of this season’s production already dispatched, supply remains tighter than expected for this stage of the campaign.

April market outputs totalled 94,527 tonnes, down 20.6% from March. However, March volumes had been exceptionally high, making some correction inevitable. April is also traditionally a quieter trading month due to Easter-related slowdowns, although market participants note that this alone does not fully explain the weaker dispatch figures.

(11)-1.jpg)

Softer activity has contributed to a nervous market tone. Lower output has raised concerns about slowing consumption, fuelling speculation that prices could soften. Buyers have become increasingly selective, while sellers are carefully managing inventories to ensure sufficient availability until the next harvest, reluctant to release stock too aggressively with several months still remaining before the next crop arrives.

Uncertainty continues to dominate sentiment, with the market caught between signs of weaker demand and the risk of tighter availability later in the year.

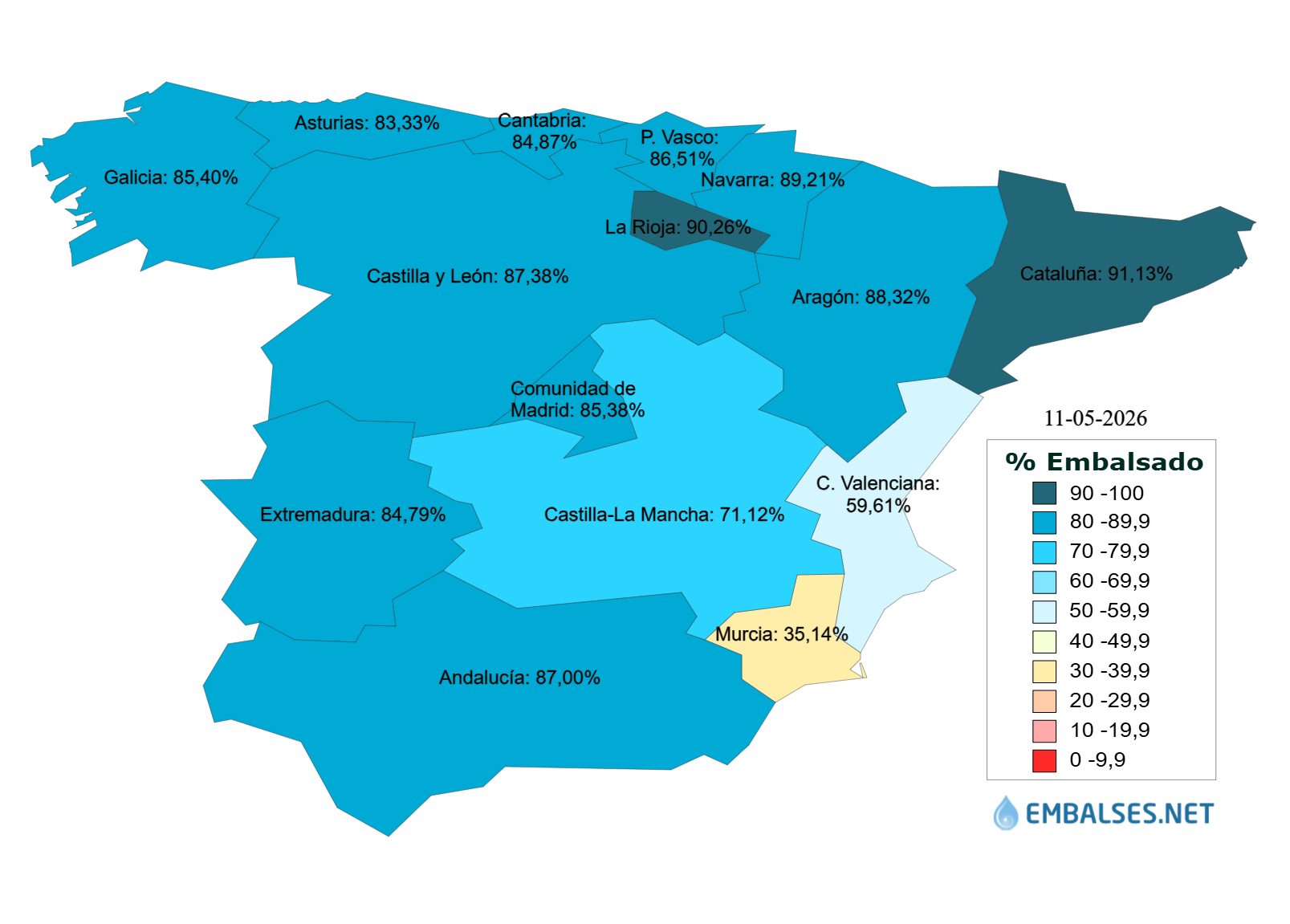

Attention is now on the early outlook for the 2026–2027 harvest as flowering and fruit set progress across producing regions. Conditions are very positive, with favourable spring temperatures and healthy reservoir levels (80–90%+ across key areas), supporting expectations for a strong crop next season.

Prices have declined since last week. Extra virgin olive oil (EVOO) is trading at €4.00–€4.60/kg, virgin olive oil (VOO) at €3.70–€3.80/kg, and lampante at €3.20–€3.30/kg.

.jpg)

Greece’s olive oil market

Greece’s olive oil market remains quiet, with prices edging slightly lower amid limited trading activity and cautious sentiment.

Although stock levels are relatively low, the market is not facing an extreme shortage. Operators are carefully managing inventories to ensure supplies last through to the next harvest. With few active buyers, sellers are proceeding cautiously, reluctant to release stock aggressively amid uncertainty.

Reduced market output is fuelling concerns about weaker demand and consumption, adding potential downward pressure on prices. The supply environment remains nervous, similar to Spain, with sellers increasingly cautious.

Attention is on flowering and early fruit development for the 2026–2027 harvest. Initial conditions are encouraging, and expectations for solid production next season are building, creating uncertainty as operators reassess pricing amid lower consumption.

Current EVOO is priced at €4.15–4.80/kg, reflecting modest downward pressure.

Italy's olive oil market

Italy’s olive oil market remains quiet, with low trading activity and limited buyer interest as participants wait for clearer signals on supply and pricing direction. Transaction flow remains weak, reflecting a cautious tone.

Inventory levels are tight relative to demand, prompting careful stock management ahead of the next harvest. Domestic consumption remains subdued, further weighing on momentum.

Production has fallen this season, leaving output below Italy’s consumption needs and export commitments. As a result, the country continues to rely on imports from Spain and Tunisia, although volumes are limited.

EVOO prices, while still holding a premium over other origins, have eased significantly to €5.80–6.80/kg, reflecting weaker demand conditions and a normalization from the high-price environment of past years.

Attention is now focused on the flowering stage, which is broadly positive across key regions. However, expectations of a stronger upcoming harvest, combined with weaker sales, are creating an uneasy market tone.

Tunisia's olive oil market

Tunisia has recorded an exceptionally strong production campaign, resulting in abundant supply and significant volumes still unsold.

Prices are under pressure, with EVOO currently trading between €3.80 and €4.10/kg, reflecting ample availability in a well-supplied market. Even so, Tunisian oil remains highly competitive compared with other origins.

Export demand has held relatively steady, supported mainly by buyers in the United States. In contrast, domestic consumption has weakened as higher prices continue to limit local purchasing power.

Agronomic conditions remain broadly positive, with good flowering and healthy reservoir levels supporting a stable outlook for the next campaign. However, sentiment remains cautious, as strong current production combined with expectations of a solid harvest is keeping the market well supplied.

Cross-country analysis

Across the Mediterranean, the olive oil market is characterized by adequate supply and low activity, creating a cautious and uncertain trading environment. Sentiment remains nervous, with operators closely managing inventories and reluctant to take on risk, as low sales volumes are increasingly interpreted as a signal of weaker underlying consumption.

Spanish and Greek oils are trading in a relatively narrow and lower range compared with last year, while Italy continues to command a clear premium. Tunisia remains the most competitive origin.

.jpg)

Overall, the market is driven by psychological tension between adequate supply, weak demand momentum, and heightened sensitivity to forward harvest expectations.

Rapeseed oil

The rapeseed oil market is stable and well supplied, with overall sentiment remaining balanced. Harvest expectations are strong due to favourable crop conditions across key producing regions. Global production for 2026/27 is forecast at record levels, driven by expanded acreage. Canada is expected to remain the largest producer, while EU output is projected to reach a multi-year high.

At the same time, steady demand from crushers, the biodiesel sector, and the food processing industry continues to underpin consumption. European rapeseed prices rose steadily through Q1, although momentum has recently stabilized.

Trade flows have been reshaped by policy shifts, with Canadian rapeseed oil facing a 100% tariff in China and being redirected toward US and European markets. Australia has partially filled the gap by resuming exports to China after a five-year pause, helping offset the imbalance.

Sunflower oil

The sunflower oil market is currently firm but volatile, driven mainly by geopolitical risk and tighter Black Sea supply conditions. Prices have risen in recent weeks following conflict-related disruptions, with an additional risk premium emerging from tensions in the Middle East.

Despite this, underlying fundamentals remain relatively balanced. Global trade flows are steady, while Black Sea availability remains structurally constrained. As a result, the market is highly sentiment-driven, with prices reacting quickly to geopolitical developments.

Looking ahead, expectations of a strong upcoming harvest cycle suggest potential for prices to stabilize or ease once current risk premiums fade, provided no further supply disruptions occur.

Avocado oil

The avocado oil market is currently stable, with a slightly softer tone due to peak seasonal supply from Peru, which is increasing availability and weighing on prices in the short term. This softness is expected to be temporary, with the market likely to recover once Peruvian output normalizes.

However, a second downward phase is expected later in the year as Mexico enters its peak production period, adding further volumes and reintroducing price pressure.

Demand remains strong, driven by steady growth in health-focused consumption and food use in Europe and North America, helping to limit downside risk and maintain a stable baseline.

Market outlook

Across the edible oil complex, market dynamics remain mixed. Sunflower oil continues to be the most volatility-driven market due to geopolitical risk, while olive and rapeseed oils remain anchored by balanced-to-ample supply conditions. Avocado oil is shaped by cyclical production peaks within a broader long-term growth trend.

Key watchpoints by sector:

● Olive oil: Flowering, fruit set, and summer weather conditions across the Mediterranean will shape expectations for the next harvest and drive market sentiment.

● Rapeseed oil: Crop development in Canada, Argentina, and the EU, alongside biodiesel demand, will determine whether supply remains comfortably balanced.

● Sunflower oil: Geopolitical developments in the Black Sea and Middle East remain the main risk factors, with any disruption likely to trigger sharp price volatility.

● Avocado oil: Peru’s seasonal supply decline and the timing of Mexico’s next production peak will define short-term price direction.

Source vegetable oil with confidence on Wikifarmer's Marketplace:

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")