")

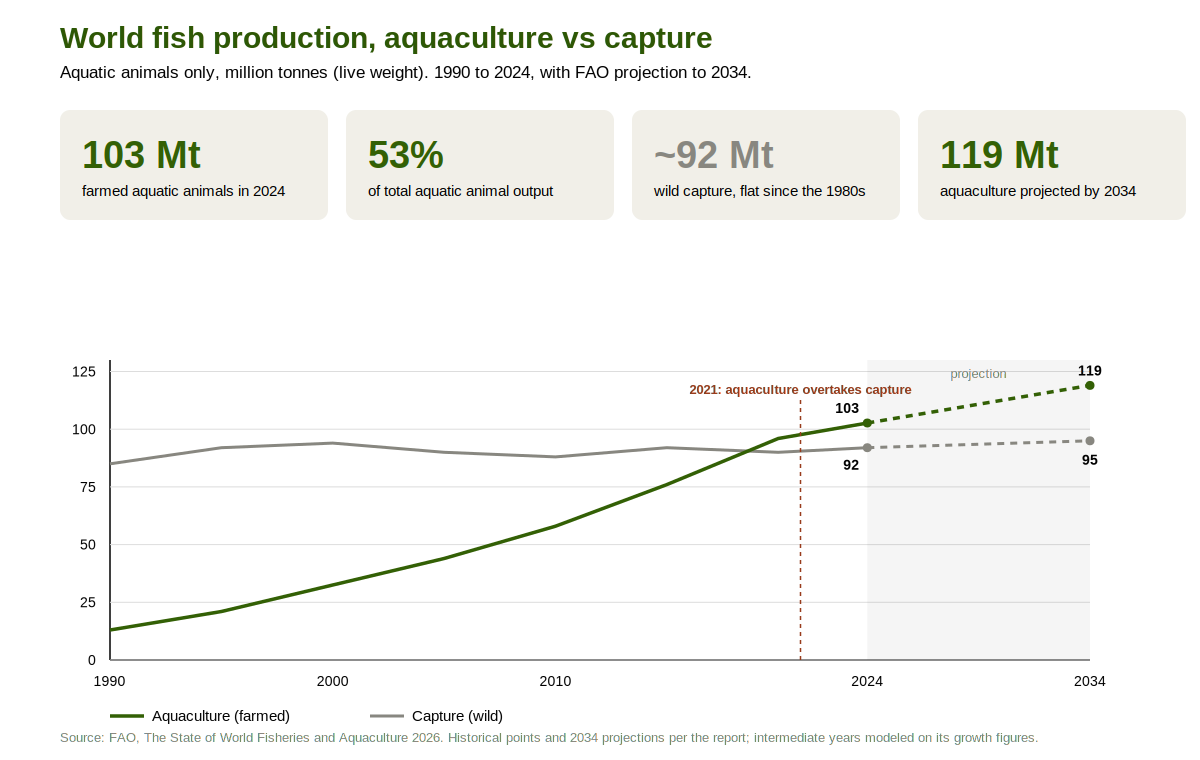

For most of human history, the fish on a plate came from a net pulled through open water. That is no longer the default. According to the 2026 edition of The State of World Fisheries and Aquaculture, the FAO flagship report on the sector, farmed aquatic animals have moved past wild-caught ones as the main source of the fish people eat. In 2024, aquaculture produced 103 million tonnes of aquatic animals, an all-time record, equal to 53% of global aquatic animal output and more than 59% of the aquatic animal food destined for human consumption.

This is a structural change in how the world feeds itself, and the numbers behind it are worth reading carefully, because they reshape what producers, buyers and consumers can expect from the seafood supply over the next decade.

A record year for total production

Total fisheries and aquaculture production reached a new high of 235 million tonnes in 2024. That figure breaks down into 195 million tonnes of aquatic animals measured in live weight equivalent and 40 million tonnes of algae measured in wet weight. Aquatic animal production has grown steadily for decades, expanding at an average annual rate of 3.2% since 1950, and 89% of it is destined for human consumption. Average per capita availability now exceeds 21 kg per year.

The growth is coming almost entirely from one side of the ledger. Capture fisheries, the wild catch, stayed essentially flat at around 92 million tonnes in 2024, continuing a long pattern of fluctuating between roughly 86 and 94 million tonnes since the late 1980s. Marine capture remains the single largest source of wild aquatic animals at about 80 million tonnes, and inland fisheries reached a record 12.3 million tonnes. But the wild catch has hit a ceiling. Aquaculture, by contrast, keeps climbing, and that divergence is the whole story of the 2024 figures.

What the 53% milestone actually means

It is worth being precise about the milestone, because the headline numbers can be stated in several ways. Aquaculture's 103 million tonnes represents 53% of total aquatic animal output. When the comparison is narrowed to aquatic animal food intended for people to eat, rather than the portion diverted to fishmeal, fish oil and other non-food uses, aquaculture's share rises above 59%. Either way, farmed fish are now the majority source of the seafood that reaches human diets.

This matters because wild capture cannot fill the gap left by rising demand. The share of the world's marine fishery stocks fished within biologically sustainable levels declined to 62.4% in 2023, down 2.1 percentage points from 2021. When weighted by catch volume, the picture is somewhat better, with 72.6% of the landings from assessed stocks coming from sustainably fished populations, which indicates that larger and more productive stocks tend to be better managed. Even so, the direction is clear. There is little room to harvest more from the wild without depleting it further, which is precisely why farmed production has become the route to meeting growing demand. By taking on that role, aquaculture relieves pressure on wild populations, a point covered in our look at the role of aquaculture in preserving marine biodiversity.

Where the world's farmed fish come from

Two facts define the geography and biology of aquaculture today, and both carry consequences for the wider sector.

Production is concentrated. Asia accounts for around 89% of global aquatic animal aquaculture, and the top five producing countries together generate 82% of the total. A supply this concentrated means that policy shifts, disease outbreaks or input-cost changes in a handful of countries ripple through the entire global market.

Freshwater dominates. Of the 103 million tonnes of farmed aquatic animals, 64 million tonnes (63%) came from freshwater systems, against 38 million tonnes (37%) from marine and coastal systems. The mental image of aquaculture as offshore sea cages is only part of the reality; inland ponds and freshwater systems still produce most of the world's farmed fish.

For the Mediterranean, the marine share is where the regional industry sits. European sea bass and gilthead sea bream anchor the basin's marine aquaculture and command strong markets across Europe. The farming methods and economics of these and other farmed species are set out in our overview of the most important cultivated marine species.

Aquatic foods in diets and rural economies

The shift toward farmed production goes beyond volume. Aquatic foods supply essential micronutrients, omega-3 fatty acids and high-quality protein that support healthy diets, and the dietary case for them is detailed in our piece on marine sources of omega-3 fatty acids. In 2023, aquatic animal foods provided at least 20% of the per capita animal protein supply for more than 40% of the world's population. In Africa, they contribute around 19% of animal protein availability, the second-highest regional share, and in many low-income countries they are among the most affordable and accessible sources of high-quality protein.

The sector is also a major employer. Aquatic food systems supported 65 million people in primary production in 2024, a backbone of rural economies and coastal communities. Women make up 27% of primary-production employment and 56% of the workforce in processing. And the value moving through the system is substantial. Global trade in aquatic products reached USD 186 billion in 2024, involving 230 countries and territories, a value comparable to trade in terrestrial meats and equal to about 9% of total agricultural trade.

The next decade points the same way

FAO projections to 2034 extend the trend rather than reversing it. Total aquatic animal production is expected to reach 214 million tonnes, with aquaculture remaining the main source of growth at a projected 119 million tonnes. Capture fisheries are forecast to recover modestly to around 95 million tonnes, attributed to improved management and reduced losses rather than expanded effort. More than 90% of production is expected to reach human consumption, lifting per capita availability to 21.9 kg globally.

That global average hides an uneven distribution. The fastest growth in aquatic food availability is forecast for Africa, at 18%, yet per capita availability there is still projected to fall, because population growth will outpace the gains in supply. This is the central tension running through the report. Aquaculture has the capacity to feed a growing world, but whether that capacity reaches the regions that need it most depends on investment, governance and innovation rather than on production records alone. Without progress on those fronts, growth risks outpacing both equity and sustainability.

The 2024 figures confirm the milestone. Farmed fish now feed more people than the wild catch does. The harder question for the decade ahead concerns not the pace of growth but its quality, whether aquaculture can grow sustainably and reach the diets that depend on it.

")