")

Berry Market Digest | Week 19, 2026

European berry markets enter mid-May with broadly stable pricing despite rising Spanish and Portuguese supply and strengthening northern European production. Strawberries continued to show a north–south split, with softer conditions in the south contrasting with firmer pricing in France, Belgium, and Germany. Blueberries, meanwhile, hold prices despite higher Iberian throughput, supported by steady spring demand.

Stay up to date with our weekly Fresh Fruit Market Digests

Market overview – weekly developments

- Strawberry supply continues to rise in Spain, later than usual, particularly from Huelva, where delayed early-season production has extended output into May. This has kept Spanish volumes elevated at a point when they typically begin to decline.

- Northern European production has expanded further. Germany increased domestic supply and overtook Greece as a key origin, while Belgium, France, and the Netherlands all saw improving availability ahead of peak spring consumption.

- For blueberries, despite rising arrivals from Spain and Portugal, prices remained broadly stable, with very limited movement in weekly averages.

Price analysis across four markets

Mercamadrid

Mercamadrid recorded 1,272.5 tonnes of strawberries between 4–7 May (week 19). Huelva dominated supply with 87% of arrivals, followed by Portugal at 12.8%, while Segovia accounted for a minor share of 2.2 tonnes.

.jpg)

Wholesale strawberry prices remain under pressure. Huelva and Portuguese fruit traded within a broad €1.50–€5.00/kg range, with the most frequent price at €2.69/kg. Segovia fruit achieved a slightly higher average price of €2.75/kg.

The late-season supply profile is unusual for May. Disrupted early production due to winter storms delayed the campaign, resulting in a compressed overlap between mid- and late-season varieties. As a result, elevated Spanish supply is now extending further into the European season than normal, keeping prices subdued.

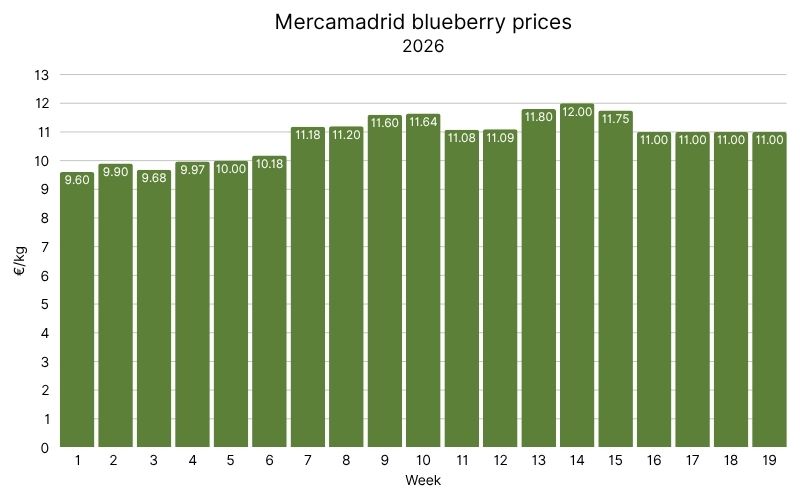

On the other hand, blueberries remained stable despite rising Iberian arrivals. Fruit from Huelva, Portugal, and Segovia continued to trade within a €6.00–12.00/kg range, with €11.00/kg the most common level.

Partial week 19 data shows Iberian arrivals rising to nearly 48 tonnes (Mon–Thu), up from 31 tonnes the previous week. Huelva increased from roughly 28 tonnes to over 41 tonnes, while Portugal added around 5 tonnes.

Despite this increase, prices held firm, indicating that demand continues to absorb additional supply without meaningful discounting. The market peaked near €12.00/kg in week 14 (Easter period) before easing slightly, but has since stabilized at higher-than-expected levels.

Rungis International Market

Rungis International Market saw firmer strawberry pricing in week 18 ahead of the May 1 holiday period, as demand improved after earlier concerns about oversupply.

.jpg)

Prices strengthened through the week: Spanish 1kg trays rose from €3.00 to €4.00, Belgian 500g punnets from €7.00 to €9.00, and French 500g punnets from €7.00 to €8.00.

The spread between origins has narrowed significantly. Belgian strawberries, now in peak production after a season opening in mid-March, are trading far closer to Spanish fruit than earlier in the year. French fruit is now broadly aligned with Belgian pricing at the wholesale level.

German Federal Office for Agriculture & Food (BLE)

German Federal Office for Agriculture and Food (BLE) reported a sharp rise in domestic strawberry supply in week 18, with German fruit overtaking Greek origins as northern European production strengthened.

Despite improved demand ahead of the May 1 holiday, supply growth outpaced consumption, leading to price cuts across multiple origins. Berlin reported difficulties moving standard grades due to retail returns, while Munich flagged quality issues in Spanish and Greek fruit requiring rapid clearance.

.jpg)

Greek strawberries were down 25% year-on-year, while German domestic prices fell 16.9% week-on-week as early greenhouse premiums faded. However, they remain above long-term seasonal averages.

Germany is now entering its main open-field production phase, with volumes expected to peak in May and June.

Italian strawberries continue to trade at a structural premium of around €0.65/kg over Spanish fruit, supported by strong southern Italian export production.

Greek Central Markets & Fishery Organization (OKAA)

Greek Central Markets & Fishery Organization (OKAA) reported a prevailing strawberry price of €2.50/kg on 5 May (week 19), unchanged from both the previous week and the same period in 2025.

.jpg)

Production remains concentrated in the Peloponnese, particularly Manolada, where the season runs from late September through late June, peaking in April and May. Prices have firmed slightly in weeks 18–19 as the season enters its final phase.

Domestic stability contrasts with higher Greek-origin values in northern European wholesale channels, where logistics and distribution costs lift landed prices.

Cross-market dynamics

- Southern markets are entering late-season conditions where elevated supply and overlapping harvest windows are weighing on prices.

- Northern Europe is being driven by expanding domestic production, reduced reliance on imports, and earlier-season pricing stabilization.

- In blueberries, the market remains in temporary equilibrium. Rising Iberian supply has not yet disrupted pricing, indicating that demand is currently absorbing additional volume.

Market outlook

Spanish strawberry supply is expected to gradually decline over the next 4–6 weeks as the Huelva campaign winds down, though the delayed season may push volumes into later weeks.

In Germany, prices are likely to ease as open-field production expands and greenhouse premiums fade. Belgium and the Netherlands are expected to remain relatively firm due to more controlled production systems.

Italy remains an exposed origin, facing sustained competition from Spanish volumes into late May.

For blueberries, further supply increases from Spain and Portugal will test price stability, likely leading to lower prices relatively soon.

Buy and sell fresh fruit on the Wikifarmer Marketplace and track real-time prices with Wikifarmer’s Price Insights

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")