")

Stone Fruit Market Digest | Week 22, 2026

The European stone fruit campaign is now in its high-volume phase. Spanish supply is surging in all categories. Prices have decreased for most cherries, peaches, nectarines, apricots, and flat peaches. Wholesale markets in Germany and France are slowly catching up, increasing supply, but their prices remain markedly higher and, for premium cherries, are still climbing.

This report analyzes fresh fruit in four major EU wholesale markets: Spain's Mercamadrid, France's Rungis International Market, the German Federal Agency for Agriculture and Food market reporting (BLE), and Greece's Athens Central Market (OKAA).

Stay up to date with our weekly Fresh Fruit Market Digests

Mercamadrid prices drop

Mercamadrid prices are the lowest of the four markets compared this week. Across the board, all stone fruit prices at the Madrid wholesale market are lower than two weeks ago, indicating the campaign is moving from early-variety scarcity into main-season abundance.

.jpg)

Cherries

A huge amount of cherries, about 698 tons, is being sold through Mercamadrid this week. They are this week's top-selling variety, even surpassing peaches. At Mercamadrid, the most-frequent price has fallen to €5.20/kg (range €1.80–9.00), down hard from €8.18/kg two weeks earlier. Mercamadrid cherries this week came from Zaragoza (300 tons), Cáceres (236 tons) and Lleida (70 tons).

Spain's national crop is recovering toward a strong year. However, hail and rain damage were reported on early Extremadura and Aragón fruit, keeping top-grade, large-calibre fruit scarcer.

In Germany, the BLE quoted large Spanish-origin cherries at €9.07/kg, large Greek-origin cherries at €7.48, and small Spanish-origin cherries at €6.06. The supply was Spanish-led but uneven in quality.

In France, the Rungis bulletin called cherry prices “very high” and still rising into the weekend on thin volume. Domestic French large calibres and the premium French Rainier variety are around €10–12/kg.

In Greece, OKAA shows very different prices. Domestic cherries are prevailing at just €2.50/kg (Cat I €2.00–5.00), about half the level shown for the same week last year on that bulletin and easing further week-on-week.

Trade signal:

Mercamadrid is cheapening fast while German and French quotes remain high. German and French averages are likely to ease if larger Spanish volumes continue to clear into those markets. The exception is large-calibre and premium fruit (French Rainier, Jerte Picota), which trades as a separate, firmer market. Italy's structurally short crop continues to keep buyers oriented toward Spanish-origin supply.

Apricots

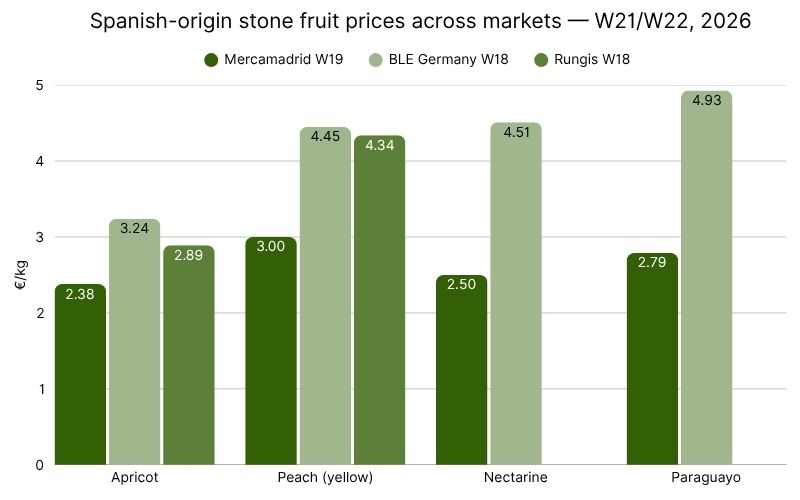

Apricots are the volume-constrained category of the season. Spain's crop is forecasted to be down, but supply has widened enough this week to soften prices. At Mercamadrid, the most frequent price for common apricots is €2.30/kg (€0.90–6.00), down from €2.72 two weeks ago, with Murcia overwhelmingly dominant, accounting for 224 of the 297-ton total.

In Greece, domestic early apricots prevail at OKAA at €2.00/kg (Cat I €1.50–3.00), easing off the prior week.

In France, Rungis called Spanish apricots clearly bearish, priced at €2.70/kg (40–45 mm) and €3.08/kg (45–50 mm), both down about 20% on the week. The French orange type is priced at €4.56/kg (down 17%), due to inconsistent fruit quality, which is slowing demand.

In Germany, the BLE showed Spanish apricots at €3.24/kg, Italian apricots at €3.54/kg, Turkish apricots at €3.66/kg, and French apricots at €4.56/kg. Supply has expanded to meet demand, with discounts to avoid overhang and to address small calibres that are difficult to sell in Hamburg.

Peaches and nectarines

Peach and nectarine volumes are now at peak levels. At Mercamadrid, the peach complex showed 555 tons. The main yellow peaches are most frequently priced at €3.00/kg, with volume exploding from just 10 tons to 155 tons in two weeks. Early red peaches are priced at €2.54/kg, down from €3.25. Yellow-flesh nectarines totalled 363 tons this week, priced at €2.50/kg, down sharply from €3.50 two weeks earlier. The nectarine is the most widely planted Spanish stone fruit. Murcia leads on production, with Badajoz and Huelva supplementing.

In Greece, OKAA lists domestic early peaches prevailing at €2.00/kg (€1.50–3.00).

In the German and French markets, prices softened. Rungis reported that Spanish-origin peaches and nectarines were both bearish: white-flesh peaches at €4.40/kg, down 20%, and yellow-flesh peaches at €4.34/kg, down 21%. Nectarine quality is described as “varying enormously,” and late-week heatwaves prevented a price increase.

The BLE shows Spanish and Italian fruit leading, with calibre and colour ranges widening. However, demand is unable to keep pace with supply, and discounts are accelerating clearance. Spanish-origin nectarines AA are priced at €4.51/kg, yellow peaches AA at €4.45, and white-flesh nectarines increased to €5.56.

Flat peaches and flat nectarines

The flat fruit segment is a growing European stone fruit market, and the data shows it is arriving in force. Paraguaya (flat peach) volume at Mercamadrid jumped up 70% week-on-week to a total of 208 tons, with the most-frequent price at €2.79/kg, down from €3.58. Murcia supplies the bulk with 149 tons.

Platerina (flat nectarine) commanded the premium end in Germany at €6.94/kg, while Spanish paraguayos were priced at €4.93/kg. Rungis held flat peaches stable on smaller volumes.

Expect flat-fruit availability and price competition to intensify quickly through June as Spanish volumes peak.

Plums

Plum season has not started yet, but some early varieties are beginning to appear in small amounts. Mercamadrid shows the first domestic purple plums at €2.93/kg on a small but rising 60 tons from Badajoz and Murcia. The price dropped from €3.32 two weeks ago.

France and Germany still do not carry European plums. The BLE plum line reflects only South African imports, priced at €2.33/kg. With the Spanish plum crop forecast slightly down this season due to fruit-set issues, early volumes stay thin until the main campaign builds in mid-summer.

Key factors to keep an eye on

● Price levels converging: The German and French averages for Spanish-origin peaches, nectarines and apricots are likely to ease as the season's larger volumes register there. Watch whether the gap narrows.

● Cherry market split: Average cherry prices keep falling with increased volume, but premium large-calibre and protected-origin fruit (French Rainier, Jerte Picota) trade as a separate, firmer market. Watch the calibre spread, not the price average. Italy's structurally short cherry crop continues to pull buyers toward Spanish supply.

● Quality risk: Inconsistent taste and quality are repeatedly reported across markets, especially in apricots and nectarines. Rain and hail have affected early Spanish cherries. The biggest factors affecting profit are how much product gets downgraded in quality and what condition it arrives in.

● Flat fruit acceleration: Paraguaya and platerina volumes are climbing the fastest. Buyers may want to lock in specifications now, before price competition increases and quality differentiation matters less.

Buy and sell fresh fruit on the Wikifarmer Marketplace and track real-time prices with Wikifarmer’s Price Insights

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")