")

Stone Fruit Market Digest | Week 19, 2026

The European stone fruit campaign is well underway. In a single week, Spanish apricot volumes in Mercamadrid grew 44%, cherry volumes nearly quadrupled, and Murcian peaches and nectarines arrived in large volumes. Yet prices are split: cherries and apricots are softening fast as supply scales, while peaches, nectarines and flat peaches hold firm—a sign that consumer demand is keeping pace with supply. Read on to get the latest news.

Stay up to date with our weekly Fresh Fruit Market Digests

Market snapshot

● Spain dominates supply: France, Italy and Greece remain pre-season for cherries, peaches and apricots. Italy’s first apricots and yellow-flesh stone fruit entered the Frankfurt market in Week 18.

● Volumes are increasing dramatically: At Mercamadrid, week-on-week supply rose +44% for apricots, +283% for cherries, +363% for nectarines and +166% for flat peaches. Peaches multiplied more than tenfold off a low base of 11.6 t in W18.

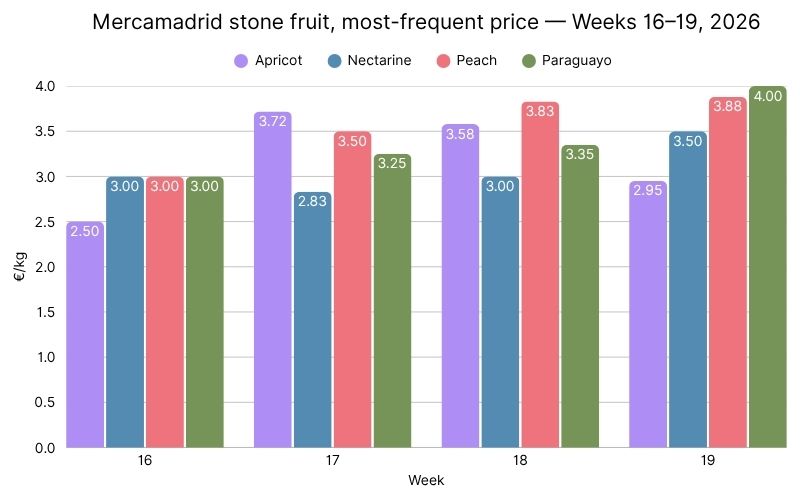

● Cherry prices are dropping: Mercamadrid most-frequent prices fell from €30/kg in W16 to €9.75/kg in W19 — a 68% decline as Cáceres (Jerte basin) and Murcia plantations come online.

● Apricot prices are easing: As Murcia ramps up production, Mercamadrid’s most frequent price slipped to €2.95/kg (–18% w/w). The German BLE weekly average for Spanish apricots was €6.21/kg (–6% w/w). At Rungis, Cat.I 40–45 mm apricots were priced at €5.25/kg.

● Peaches, nectarines, and flat peaches are increasing in price: Prices are firming despite higher volumes, suggesting demand is matching supply at this still-early stage. Mercamadrid peaches are up 1% w/w, nectarines up 17%, and flat peaches up 19%.

Spain leads the stone fruit rollout

Spain is the largest stone fruit producer in Europe and currently has the most advanced season. Italy, Greece, and France start later. Italy has just begun with early apricots from protected cultivation, while Greek and French volumes remain pre-season.

Volumes increasing

Mercamadrid shows all of its stone fruit categories increasing in volume this week, signalling a strong start to the season.

.jpg)

● Apricots reached the market in limited volumes in Week 16 and have skyrocketed since, remaining the volume leader so far.

● Nectarines and peaches entered the market in Week 16 as well, saw a brief dip in volumes last week, but jumped dramatically this week.

● Cherries started in Week 17 and have seen a large increase in volume, making them second in volume.

● Flat peaches entered the market in Week 16 in very limited volumes and have grown steadily, though they remain the lowest-volume category.

Price evolution and divergence

There is divergence in the price evolution of stone fruit categories over the last four weeks:

● Apricots and cherries have decreased in price, reflecting supply-led corrections as volumes scale up. Apricots dropped 18% week on week, while cherries dropped 30%.

● Peaches, nectarines and flat peaches have increased in price, showing demand-led firming despite rising volumes. Peaches saw a modest 1% week-on-week increase, nectarines 17%, and flat peaches 19%. This means buyer absorption is outpacing the increase in volume.

.jpg)

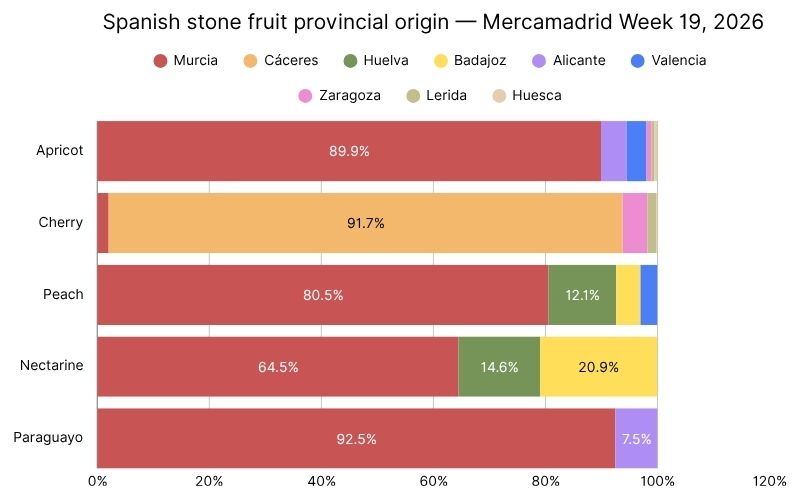

Production concentration

In Week 19, two provinces alone accounted for between 64.5% and 92.5% of Mercamadrid’s supply across all categories: Murcia for apricots, peaches, nectarines and flat peaches, and Cáceres for cherries.

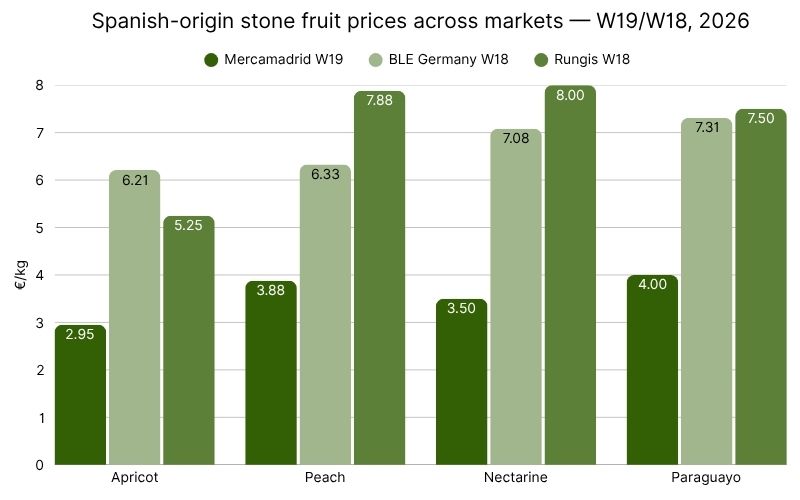

Spanish-origin stone fruit across markets

Both the German BLE and Rungis feature Spanish-origin stone fruit. The higher price Spanish fruit has in external markets reflects transport and handling costs, importer margins, calibre mix, local demand patterns, and scarcity premiums. Spanish exporters ship directly to German and French wholesale floors. Cherries are excluded as they have only begun trading at scale, and the data is fragmentary.

Of the three markets, Rungis is generally the most expensive for Spanish-origin stone fruit. Apricot is the only exception, where BLE Germany trades above Rungis — likely reflecting France's more advanced campaign progression at the wholesale level.

Fruit by fruit

Apricots

This week, Mercamadrid saw 348 tons of apricots, a 44% week-on-week increase in volume. The most frequent price was €2.95/kg, down 18% week-on-week. Murcia accounted for 90% of Week 19 supply, with smaller volumes from Alicante, Valencia, Zaragoza, Lerida and Huesca.

Murcia’s producer-exporter association (APOEXPA) stated in mid-April that 2026 Murcia apricot production will be half the size of a normal year, yet Europe-wide 2026 apricot production is forecast to be slightly higher than the average.

Italian volumes are scaling, but slower than Spanish volumes. Italian apricots arrived in Frankfurt in Week 18, as seen in the BLE.

Cross-market price comparison: Spanish-origin apricots traded at €2.95/kg in Mercamadrid, €6.21/kg in Germany (−6% vs Week 17), and €5.25/kg at Rungis (Cat.I 40–45 mm, −16% week on week in Week 17). The €3.26/kg spread between the highest and lowest market prices is the equivalent of 111% of the Madrid price. Apricots are also the only category this week in which the French market trades below the German one, reflecting France’s more advanced campaign progress.

Cherries

Mercamadrid saw 246 tons of cherries in Week 19, compared with 64 tons last week. The most-frequent price was €9.75/kg, down 30% week on week. Cáceres province alone delivered 226 tons, which is 92% of the supply.

This week saw a strong production boom, as is usual during cherry season, signalling optimism for the season ahead.

The price decline from €30/kg in Week 16 to €9.75/kg in Week 19, a 68% drop over four weeks, is a typical season-opening collapse. Calibre 24/26 mm dominates early; calibre 28+ will likely replace it in the coming weeks as orchards progress. Prices will likely continue to decrease as more volumes arrive, and larger-calibre fruit will retain the premium.

Cross-market price comparison: Spanish-origin cherries traded at €9.75/kg in Mercamadrid, €20/kg on Friday at Frankfurt (BLE, 28 mm in 2 kg cartons), and €20–€35/kg at Rungis (full calibre range), weakening toward the weekend. Because cherry is in its first complete trading week, neither the German nor the French market publishes a weekly weighted average yet. The spread is a range from about 105% on the smallest calibres up to 259% on the largest premium calibres, with the upper end being the largest spread of any stone fruit category.

Peaches

Mercamadrid saw 159 tons in Week 19, an increase of 1,269% on a low Week 18 base of 11.6 tons. The most frequent price is €3.88/kg, up just 1% week-on-week. Murcia supplied 81% of the fruit, Huelva 12%, and Badajoz and Valencia accounted for the remaining 7% combined.

The season officially started last week with its first volume, but it is not yet in full supply. Higher volumes can be expected from next week onwards.

For prices, demand-led firming will likely continue next week. Italy added size A peaches and nectarines in the German BLE Frankfurt market in Week 18, from southern Italian protected cultivation. Spanish mid-season varieties will likely enter at scale in two to three weeks, which is when prices should stabilize.

Cross-market price comparison: Spanish-origin peaches traded at €3.88/kg in Mercamadrid, €6.33/kg in Germany (BLE size A weekly average, with AA at €7.17/kg and B at €6.35/kg), and €7.88/kg at Rungis (white-flesh Cat. I A in Week 17, +5.1% week on week). Yellow-flesh lots ran higher at Rungis: Cal A at €10/kg and Cal B at €8/kg. The €4/kg spread between the highest and lowest market prices equals 103% of the Madrid price.

Nectarines

Mercamadrid saw 173 tons in Week 19, up 363% week on week. The most-frequent price was €3.50/kg, up 17% week on week. Murcia supplied 64%, Badajoz 21%, and Huelva 15%.

The Murcia campaign window is nearly identical to the peach window. Some early Murcia nectarine varieties were affected by frost earlier in the season, but overall, the season is progressing well. Italian size A nectarines also began arriving at the Frankfurt market in Week 18.

The +17% price firming alongside +363% volume growth likely means demand is outpacing supply and that buyers are absorbing everything that arrives. This likely won’t last long, as Italian volumes are set to arrive in the coming weeks, which should stabilize prices lower.

Cross-market price comparison: Spanish-origin nectarines traded at €3.50/kg in Mercamadrid, €7.08/kg in Germany (BLE size A weekly average, with AA at €7.58/kg and B at €6.44/kg), and €8/kg at Rungis (Cal B in Week 17). The €4.50/kg spread equals 129% of the Madrid price, reflecting tight first-lot supply at the German and French wholesale floors.

Flat peaches

Mercamadrid saw 27 tons in Week 19, up 166% week on week. The most frequent price was €4.00/kg, up 19% week-on-week. Murcia supplied 92% and Alicante 8%.

APOEXPA reported a flat peach acreage expansion this season. This fruit has been gaining in popularity among consumers, and more growers are willing to produce it.

Cross-market price comparison: Spanish-origin flat peaches traded at €4/kg in Mercamadrid, €7.31/kg in Germany (BLE weekly average), and €7.50/kg at Rungis (Cal A in Week 17). The €3.50/kg spread equals 88% of the Madrid price, the narrowest among the four stone fruit categories, reflecting a more even distribution of flat peach supply across the three markets.

Looking ahead

The stone fruit season is progressing well, and the volume jump in Mercamadrid this week is a positive sign. Here are some key trends to watch in the coming weeks:

● Apricots could reach a price floor soon: Murcia mid-season varieties are peaking, Italian volumes will add pressure, Greek varieties should arrive soon at a lower price floor than the current Spanish supply, and BLE prices should settle soon too, with increased supply.

● Expect further softening in cherries: More volumes are coming, and larger calibre-28+ fruit will slowly replace the smaller 24/26 mm fruit in markets now. Calibre 30+ will hold a premium. The high Rungis price should decrease too.

● Peach and nectarine prices could firm before they fall: The Week 19 demand-led firming is unsustainable once Italy adds fruit and Spain’s mid-season cultivars enter at scale.

● Resale margins under pressure: BLE Hamburg flagged rising volumes as a factor. Northern European re-distributors may see margin compression.

● French campaign start: A delayed French campaign would extend Spain’s monopoly window and may support firmer pricing.

● Italian Ninfa incoming: The BLE noted Italian Ninfa entering the Frankfurt market from protected cultivation in Week 18. If outdoor volumes follow soon, expect faster Spanish price compression.

Buy and sell fresh fruit on the Wikifarmer Marketplace and track real-time prices with Wikifarmer’s Price Insights

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")