")

Berry Market Digest | Week 18, 2026

This week, strawberry markets across Europe show southern-origin prices at seasonal lows or stabilizing as production peaks, while northern greenhouse fruit continues to command a strong premium. Mercamadrid posted its first weekly increase since January, while Belgian-origin fruit at Rungis has fallen significantly from its early-season peak. Dutch and German greenhouse strawberries remain in the high €7–8/kg range, widening the gap between greenhouse supply and field production.

Stay up to date with our weekly Fresh Fruit Market Digests

European strawberry market overview

The European strawberry market is currently in the peak phase of southern production, while northern supply is only beginning to expand.

Spain’s Huelva campaign, the dominant early-season volume driver in Europe, is at peak output. Growing conditions have been broadly favourable in recent weeks, with balanced temperatures, adequate sunlight, and sufficient rainfall supporting both yield and fruit development without disrupting harvesting, as seen earlier in the season. Market sources report strong quality and large calibres.

Italy is also at peak production, with high volumes and generally good quality. The market remains largely domestically oriented, but export flows continue into Central Europe.

In Greece, production in the western Peloponnese remains solid. Price volatility persists, driven by variability in fruit quality and a heavier reliance on domestic absorption, alongside a more limited and inconsistent export channel into Northern Europe.

Further north, greenhouse production in the Netherlands, Belgium, and Germany continues to anchor the premium segment of the market. Open-field production remains several weeks away from scaling meaningfully, keeping northern markets dependent on protected cultivation.

Overall, southern open-field volumes are saturating markets, while northern Europe continues to trade at a premium, reinforcing the two-tier pricing dynamic.

Price analysis across four markets

Mercamadrid

Mercamadrid recorded a weekly rise to €2.67/kg in Week 18, up 6.8% from €2.50/kg the previous week. While modest, it marks the first upward movement since week 12.

.jpg)

Prices have fallen steadily through the season, reaching a low in Week 17 before this rebound. The move is consistent with supply normalization, reflecting peak Huelva volumes. The Spanish market is stable at current levels, and prices are not expected to drop much lower. Sometime in May, when supply dwindles, prices are expected to increase.

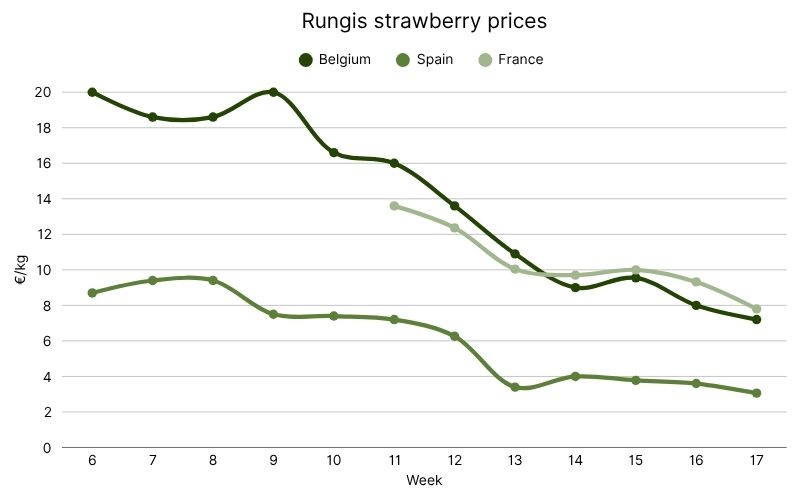

Rungis International Market

The Paris wholesale market continues to reflect the most pronounced price correction.

Spanish-origin fruit at Rungis went from above €9/kg in Week 8 down to €3.05/kg by Week 17 (-68%). The Spanish price floor at Rungis is now within €0.40/kg of the Mercamadrid price, showing that logistics and handling are absorbing nearly the entire price spread.

French domestic supply entered the dataset at €13.60/kg in Week 11 and has since settled at €7.80/kg in Week 17, slightly above Belgian fruit. The convergence of Belgian and French prices around €7.20–7.80/kg in Week 17 indicates that open-field and greenhouse supply are now more in line.

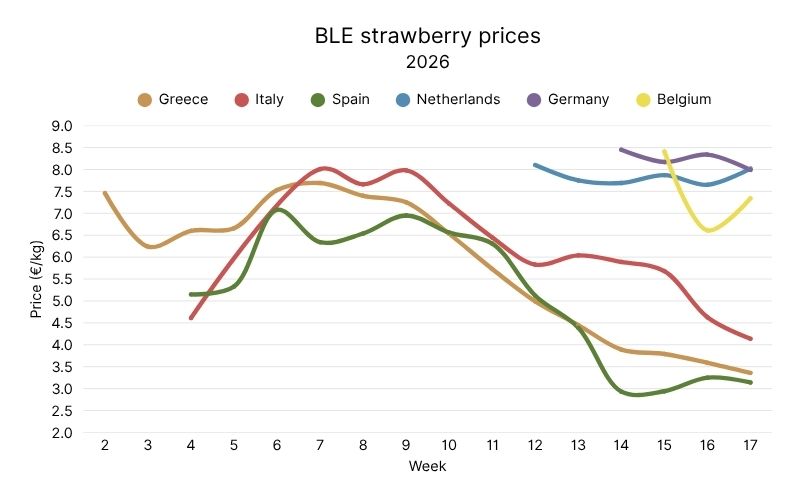

German Federal Office for Agriculture & Food (BLE)

The German wholesale benchmark currently displays the most pronounced two-tier structure. Mediterranean origins — Greek, Italian, Spanish — cluster between €3.15/kg (Spanish) and €4.20/kg (Italian) in Week 17. Northern origins — Dutch, German, Belgian — cluster between €7.40/kg (Belgian) and €8.00/kg (Dutch and German). The €4–5/kg gap reflects the cost of protected production.

Within the southern tier, Italian fruit is holding a roughly €1/kg premium over Spanish and Greek origin, a premium that has narrowed sharply from its Weeks 7–9 peak. Greek and Spanish prices have converged in the low-€3 range, with both down approximately 50–55% from their early-spring highs. The Belgian drop to €6.60/kg in Week 16, below the Dutch and German prices, suggests possible inventory clearance.

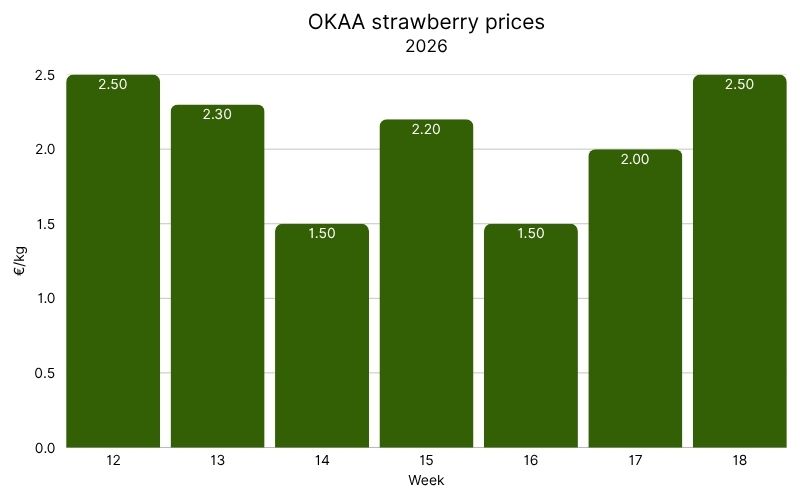

Greek Central Markets & Fishery Organization (OKAA)

OKAA is the most volatile market in the panel, with prices swinging between €1.50/kg and €2.50/kg over the strawberry availability window. Most of the fruit is consumed domestically, and therefore prices depend heavily on domestic demand.

The Week 14 and Week 16 lows of €1.50/kg could symbolize over-supply, possibly tied to irregular harvests. The Week 18 close of €2.50/kg matches the seven-week high and represents a 67% rebound in only one week. With Greek-origin fruit at BLE simultaneously trading at €3.30/kg, the OKAA-to-BLE spread of €0.80/kg has narrowed, making it difficult to cover export logistics costs.

Cross-market dynamics

Three clear dynamics are emerging across the European strawberry trade:

1. Southern supply at peak: Spain and Greece are at peak volume, but markets this week show early signs of price stabilization.

2. Northern pricing remains structurally elevated: Greenhouse fruit in the Netherlands, Germany, and Belgium continues to trade at a persistent premium, supported by production costs and limited early field supply.

3. Arbitrage windows are narrowing: The spread between origin and destination markets—particularly between Spain and France—has compressed to levels that leave little commercial margin outside contracted flows.

Market intelligence takeaways

Where prices are strengthening. Mercamadrid (+6.8% w/w) and OKAA (+25% w/w) both registered upward moves in Week 18 — the first coordinated bullish signal from southern origin markets in weeks.

Where prices are weakening. Belgian fruit at Rungis continues to decrease and is now below Dutch and German benchmarks at BLE, a sign that the greenhouse premium is lessening as the calendar moves toward field-harvest season. Italian fruit at BLE has lost roughly half its peak value and continues to drift lower as volumes scale.

What to watch next week:

● Southern European prices are approaching a floor. A second consecutive uptick in Mercamadrid would confirm this, while a relapse below €2.50/kg would indicate the decrease was a single event.

● Northern open-field production is scaling. The progressing field harvests will likely compress the BLE northern premium.

Overall, the next few weeks will define the pace of the south-to-north balance in the European strawberry market.

Buy and sell fresh fruit on the Wikifarmer Marketplace and track real-time prices with Wikifarmer’s Price Insights

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")