")

Stone Fruit Market Digest | Week 26, 2026

In Week 26, the European stone fruit harvest is at its peak. At Mercamadrid, volumes eased back from last week’s high, and prices went two different ways. Northern markets are seeing high volumes, with German cherry market prices dropping sharply across all origins, and French stone fruit prices too, week on week.

This report covers stone fruit wholesale activity in four major EU markets: Mercamadrid (Spain), Rungis International Market (France), the Federal Office for Agriculture and Food (BLE) market reporting system (Germany), and Athens Central Market (OKAA) in Greece.

Stay up to date with our weekly Fresh Fruit Market Digests

Mercamadrid volumes down, prices split

With the seasonal peak now behind it, Mercamadrid turned two-sided. Volumes eased off last week’s high: cherries lowered to 1,030 tons, the peach complex to 1,312 tons, and nectarines to 676 tons.

Prices split: Apricots firmed to €2.47/kg, red peaches to €2.25/kg and flat peaches to €2.47/kg, Meanwhile, cherries eased to €3.52/kg, yellow peaches to €2.05, nectarines to €2.28 and purple plums to €2.25. The month-long decline is flattening for some fruits, while others continue to drop.

.jpg)

Cherry prices continue declining

Cherries are at their peak. At Mercamadrid the most-frequent price eased to €3.52/kg on a tapering 1,030 tons.

Greece (OKAA, Athens) again held domestic cherries at €2.50/kg, still around half the year-ago level.

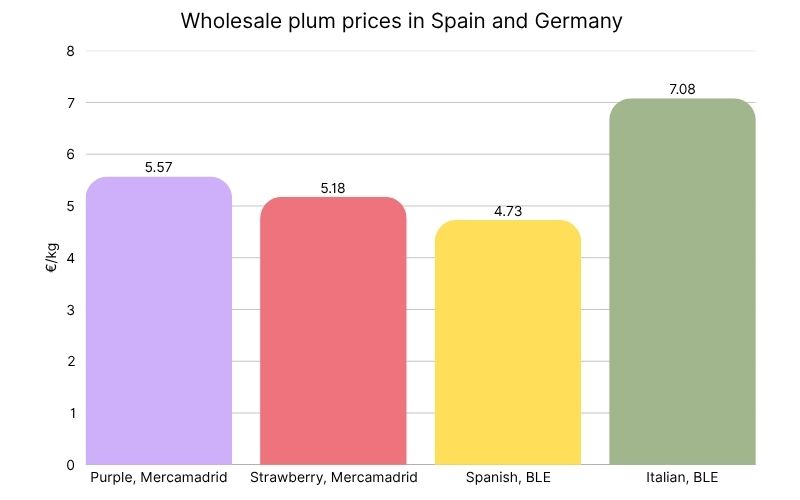

In Germany, the campaign is unwinding fast. The assortment was broad: Spanish-led, with strengthening German supply, a larger Turkish role (absent only in Frankfurt), and Italian, Greek, and French fruit too. However, demand could not absorb it, and every origin fell sharply: large-fruited Spanish to €5.18/kg (from €7.17), Italian to €4.73/kg (from €7.78), Greek to €5.57/kg, and German to €7.08/kg.

In France, Rungis was called the cherry market complex due to heavy arrivals, timid consumption, and inconsistent Spanish quality, with both French and Spanish lots lowering prices to sell inventory rather than leave stock unsold.

.jpg)

Rungis receives peak volumes

At Rungis, the rising peak-season volume alongside strong inter-regional and Spanish competition dragged stone fruit prices down across the board.

French apricots fell 16% to €2.80/kg, nectarines 12% to €3.70/kg, and French peaches 11–12% to €3.66–3.74/kg. Spanish peaches dropped to €1.88–1.92/kg. Demand was decent, but it could not keep up with the offer.

On plums, the French Golden Japan campaign began while Spanish operators cut prices to hold share.

.jpg)

Apricots

Apricot prices varied by market. At Mercamadrid they were the week’s firmest line, up to €2.47/kg (€1.10–5.00) on 315 tons, Murcia-led.

Greece held early apricots around €1.50/kg, with premium grades near €3.50.

At the northern markets, they eased: Germany had French apricots at €3.44/kg, Turkish at €3.25 (the first significant Turkish arrivals), Italian at €3.08 and Spanish at €2.86, with German fruit around €4.15.

France’s Rungis dropped French apricots 16% to €2.80/kg.

Peaches and nectarines

Peaches and nectarines split between firming red fruit and softening yellow fruit. At Mercamadrid, early red peaches firmed to €2.25/kg while yellow peaches eased to €2.05 and nectarines to €2.28/kg.

Greece held domestic peaches at around €1.50/kg.

In Germany, Spanish supply still led but eased: yellow AA nectarines were priced at €3.38/kg, white AA nectarines at €3.35, with French (peach >AA €4.57, nectarine AA €4.07) and Italian fruit above, and the first Turkish nectarines arriving.

France’s sharp declines are shown above.

Flat peaches and flat nectarines

Spanish flat peaches firmed at origin while the northern markets eased. Paraguaya at Mercamadrid rose to €2.47/kg on 400 tons.

In Germany, Spanish paraguayos slipped to €3.07/kg (from €3.30) and platerinas (flat nectarines) to €3.99/kg (from €4.46) as volumes increased.

Plums rising

Plums are the counter-trend: volumes are climbing and the range is broadening across origins, as prices ease.

Mercamadrid now carries three Spanish lines on 361 tons (up from 288 tons last week): early strawberry plums at €4.00/kg, dark plums at €2.50/kg, and purple plums easing to €2.25/kg as the crop ramps up.

In Germany, Spanish plums opened their season at €3.21/kg alongside the first Italian new-harvest plums at €4.19.

At Rungis, the French Golden Japan campaign began as Spanish prices were lowered to hold share.

Key factors to keep an eye on

- Peak season: Spanish volumes eased off last week’s high, and prices turned two-sided, with apricots, red and flat peaches firming, cherries and yellow lines still easing. Watch prices as volumes flood markets.

- Cherry prices dropping: German wholesale cherries have roughly halved over three weeks across imported origins. Clean large-calibre fruit holds superior value.

- High volumes: France and Germany are absorbing the peak that Spain saw last week, and French stone fruit fell 8–16%. Some further softening is likely.

- Plums ramping up and broadening: Spanish volumes still climbing, Italian new-harvest plums at BLE and French Golden Japan starting at Rungis. Purple-plum prices ease as volume builds.

- New origins arriving: The first significant Turkish apricots and nectarines reached the German market this week, adding to the already ample supply, and possibly another source of downward pressure on the markets.

Buy and sell fresh fruit on the Wikifarmer Marketplace and track real-time prices with Wikifarmer’s Price Insights

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.