")

Melon Market Digest | Week 28, 2026

European melon markets remained broadly stable in Week 28 as peak Spanish production kept supplies abundant, while cooler weather following the recent heatwave softened consumer demand across northern Europe. Spain is at its peak with Piel de Sapo, Cantaloupe, and Galia melons, alongside French Charentais, Italian, and Greek melons. Markets continue to rely heavily on Moroccan and Turkish watermelon alongside domestic production.

This report covers melon and watermelon wholesale activity in four major EU markets: Mercamadrid (Spain), Rungis International Market (France), the Federal Office for Agriculture and Food (BLE) market reporting system (Germany), and Athens Central Market (OKAA) in Greece.

Stay up to date with our weekly Fresh Fruit Market Digests

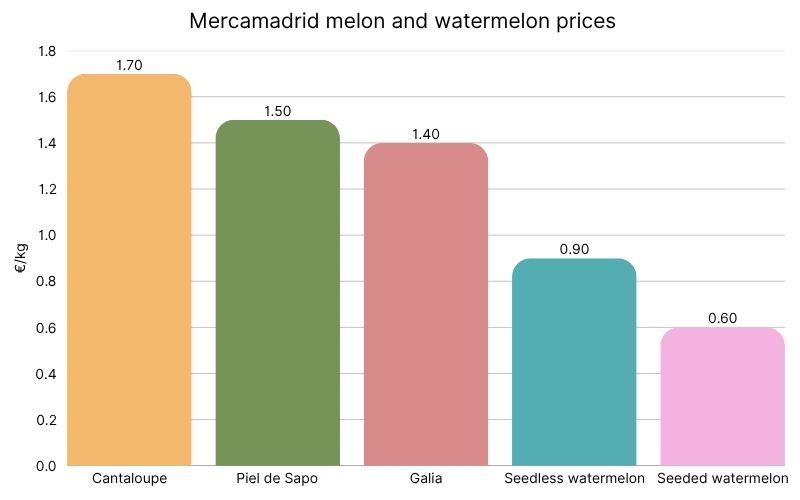

Spain’s melon market

Piel de Sapo continues to set the tone for the European melon market. Large harvests from Almería, Murcia and Valencia supplied more than 1,300 tonnes during the week, yet prices held at €1.50/kg, suggesting that seasonal demand is still broadly absorbing peak production.

Cantaloupes fetched a premium of €1.70/kg on a small volume of just 29 tons, and Galia sat at €1.40/kg for 57 tons. Prices held around last week’s levels as peak Spanish supply met summer demand.

Watermelon remained the highest-volume category by a considerable margin. Seedless fruit accounted for almost 1,800 tonnes during the week, while seeded watermelon added another 650 tonnes. Spanish production was supplemented by Moroccan imports, illustrating how watermelon continues to rely on multiple origins during peak summer demand.

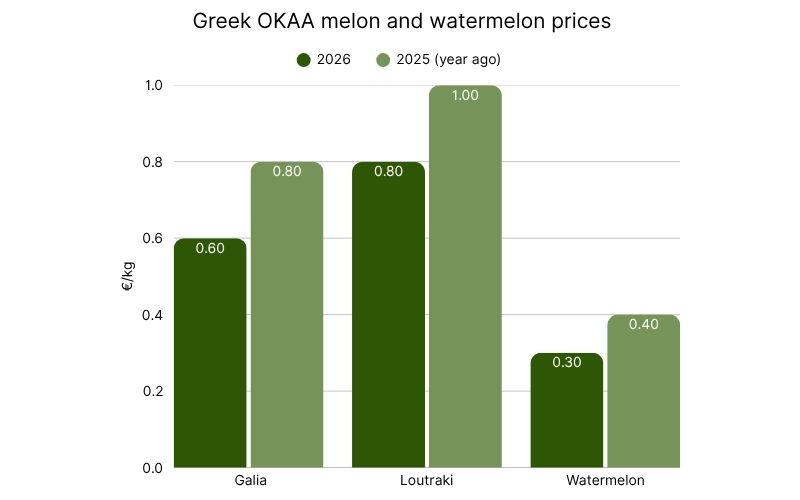

Greece’s melon market

Greece continues to trade at a significant discount to the rest of Europe. Domestic Galia averaged just €0.60/kg compared with €0.80/kg a year earlier, while Loutraki melon fell to €0.80/kg from €1.00/kg. Watermelon remained exceptionally cheap at €0.30/kg, reflecting abundant domestic production.

France and Germany's melon markets

At France’s Rungis, cooler post-heatwave temperatures slowed melon sales, and price concessions were needed to keep fruit moving. Watermelon held up better than melon, helped by more limited volumes.

At the German market, extensive watermelon supplies from Morocco and Turkey created intense competition, forcing Spanish and Italian offers to concede on price.

Market outlook

The European melon market has avoided significant price volatility despite reaching peak production, with the current supply broadly matching seasonal demand. The recent end of the heatwave has softened consumption, particularly in France, but not enough to create widespread oversupply.

- Supply is at its peak: With supply maximal, price direction from here is determined by consumer demand and weather.

- Weather is key driver: Melon is usually an impulse, hot-weather buy. The break in the heatwave has softened demand and prompted concessions.

- Piel de Sapo dominates: Spain’s signature melon is the price reference right now, steady at €1.50/kg.

- Watermelon is cheap and origin-mixed: Volume is high, but it is heavily Moroccan and Turkish in the northern markets, pressuring Spanish and Italian fruit. A high-volume, low-value, competitive line.

- Greece is soft: Domestic Galia, Loutraki and watermelon are all cheaper than in 2025 on ample local supply.

Buy and sell fresh fruit on the Wikifarmer Marketplace and track real-time prices with Wikifarmer’s Price Insights

Disclaimer: The information provided on this website, including market prices, insights, and projections, is for general informational purposes only. While we strive to ensure accuracy and timeliness, we make no guarantees regarding the completeness, reliability, or suitability of the information presented. Users are solely responsible for independently verifying the data and assessing its relevance to their specific circumstances before making any decisions. Wikifarmer and its operators shall not be held liable for any losses, damages, or consequences arising from the use of the information provided herein.

")