")

by Wikifarmer")

Potatoes are among the world´s most consumed staple crops, in traditional diets and in modern processed foods like fries and chips. However, the crop is largely consumed domestically, with most production not entering international trade flows. Today, the potato market is vast, encompassing many product streams, more industrialized, and remains geographically concentrated.

There are more than 5,000 potato varieties worldwide, providing genetic diversity for improved production stability and resistance to pests and adverse weather conditions.

Where do potatoes come from?

Potatoes originated in the Andes of South America, where they were an important part of the Inca diet. Following European contact in the 16th century, potato consumption spread throughout the world.

In Europe, potato adoption accelerated during urbanization and the Industrial Revolution. In China, potatoes (alongside sweet potato and maize) helped support population growth from the late Ming and Qing dynasties onward. In Ireland, overreliance on a narrow genetic base of potatoes led to the Great Famine of the 1840s, when crops got infected by blight. During World War II and other conflicts, potatoes were widely consumed because they are easy to grow, high-yielding, and a source of starch.

Global production

According to the FAO, global potato production was 390.3 million tonnes in 2024, cultivated on 17.07 million hectares, with an average yield of 22.9 t/ha. Production is very concentrated: the top 5 producers make up 54% of global production. The top 10 countries produce 67% of the world´s potatoes, and the top 15 produce 75%. The entire global market is valued at about $111–120 billion, showing its scale within global agriculture.

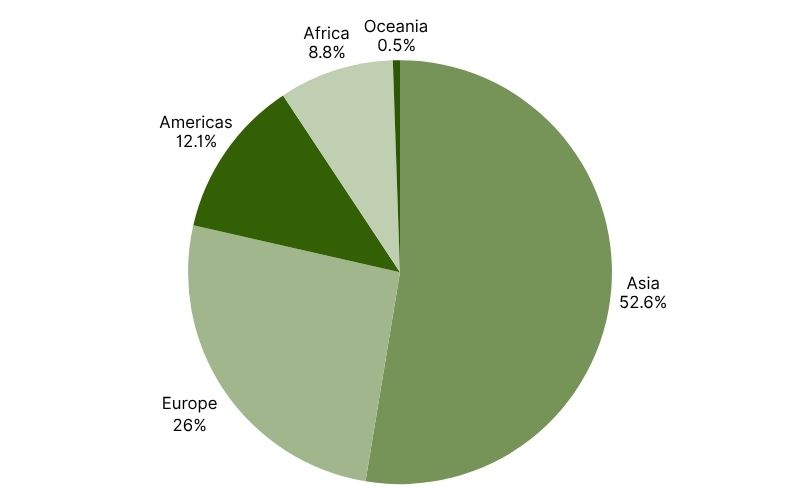

Regional production distribution

● Asia: 205.3 Mt (52.6%) on 9.24 Mha

● Europe: 101.3 Mt (25.9%) on 4.01 Mha

● Americas: 47.4 Mt (12.2%)

● Africa: 34.2 Mt (8.8%)

● Oceania: 2.1 Mt

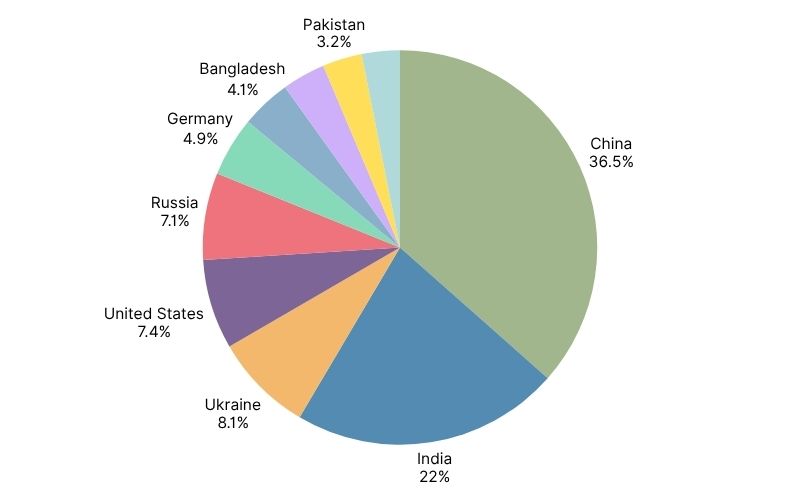

Top 10 producing countries

● China: 94.8 Mt (24.3%)

● India: 57.0 Mt (14.6%)

● Ukraine: 21.1 Mt

● United States: 19.1 Mt

● Russia: 18.5 Mt

● Germany: 12.7 Mt

● Bangladesh: 10.6 Mt

● France: 9.2 Mt

● Pakistan: 8.4 Mt

● Egypt: 8.1 Mt

Asia

Asia produces more than half of the world's potatoes (52.6%), led by China and India. The region is industrializing rapidly and emerging as a processing and export hub. China is a net exporter of frozen fries, and India's own frozen-fry exports have been increasing dramatically. The UAE is a large importer.

Europe

Europe is the most industrialized potato region, especially the EU-4 processing belt which includes Germany, France, the Netherlands, and Belgium. These countries produce the highest concentration of yields in the world.

This increase in production led to oversupply, weakening potato prices. Oversupply has been diverted into feed, starch, and anaerobic digestion, helping with processor input costs but causing problems at the producer level. A decrease in potato acreage and production is expected this season.

Americas

The Americas make up 47.4 Mt (12.2%) of global production. The United States is the largest player, producing 19.1 Mt and yielding an average of 50.9 t/ha, the highest yield among major producers.

The U.S. Department of Commerce quoted global potato exports at 3.1 million tonnes from July 2024 through June 2025, down 3.75% in volume and 0.8% in value to USD 2.3 billion. Within that total, frozen exports rose 2% and fresh exports 1%, while dehydrated fell 14.4% and chips fell 13.4%. Mexico is the top importer.

Canada (6.5 Mt) and Peru (6.6 Mt) are the next-largest producers in the region. Argentina's 2025 marketing year faced oversupply, with producers reporting very low prices.

Yield imbalance

The data shows that crop productivity is highly uneven around the world, not just in how much land is farmed, but also in how many potatoes each hectare produces:

● Oceania: 42.9 t/ha

● Americas: 30.5 t/ha

● Europe: 25.3 t/ha

● Asia: 22.2 t/ha

● Africa: 15.4 t/ha

There is a major gap between highly mechanized farming systems, which can produce around 40–50 tonnes per hectare, and low-input systems, where yields can fall below 10 tonnes per hectare in parts of Africa. The FAO now considers the potato a key crop for climate adaptation and is supporting breeding programs to develop varieties that better withstand heat, drought, and diseases, especially in Sub-Saharan Africa, South Asia, and the Andes.

Global consumption divide

Potato consumption varies sharply by region:

● Western Europe: about 50–80 kg per capita annually

● Eastern Europe: above 100 kg per capita annually

● Much of Asia: under 20 kg per capita annually

Asia-Pacific is the largest consumption region, while Africa is the fastest-growing region in terms of demand expansion. As incomes rise, demand growth shifts away from fresh consumption and toward processed potato products.

Market challenges and volatility

Potato trade dynamics nowadays are shaped by regulation and geopolitical friction. In 2025, the World Trade Organization ruled that Colombia violated trade obligations by extending 2018 anti-dumping duties on frozen fries from Belgium, Germany, and the Netherlands, which covered roughly 85% of EU exports, and ordered their removal. Furthermore, U.S. tariffs and a weaker dollar have weakened European export competitiveness.

On the other hand, biological risk is a worsening problem. EuroBlight, a research network of experts protecting potato crops from diseases, estimates that late blight costs European growers roughly €900 million annually, and the network has flagged the expansion of new clonal lineages like EU43 and EU46, as well as increased genetic diversity in pathogen populations, complicating control strategies.

Prices environment

Despite vast acreage, strong yields, solid production and demand growth, potato prices are under pressure. This is caused by uneven supply distribution and increased export competition. In Europe, for example, excess supply has pushed farmers to struggle with lower-than-normal prices while processor margins remain supported by cheap raw material inputs. In the U.S., the spread between contracted and open-market prices has widened. In Russia, however, prices are reported to have risen due to a domestic shortage.

Market takeaways for 2026/27

Here are some factors for potato market participants to consider this season:

● In Europe, a potato surplus means that expanding planting risks further price weakness.

● For processors, low-cost potatoes are helping profits, but they still need strong consumer demand to keep running at full capacity.

● China and India produce the majority of the world´s potatoes, supported by steadily improving processing capabilities, and are likely to continue exerting persistent export pressure on processors in Europe and North America.

Outlook

The potato has evolved from being a simple staple crop to a vast, industrialized global commodity system. The market is projected to expand to $145–150 billion by 2030, growing at a 3–4% CAGR. Growth is driven by processed-food demand and persistent regional oversupply, but is held back by supply chain volatility, complex logistics, adverse climate events, more crop diseases, and limited producer margins. Profitability will depend on industrial integration, mechanization, efficiency, and addressing the yield gap.

")