")

The avocado, native to the Americas, is cultivated in tropical and Mediterranean climates and consumed worldwide. Its characteristic flavour, smooth, green flesh, high nutrient density and healthy fat content have made it very popular and applicable in a wide range of diets. It is also valued in the cosmetic industry for its natural sterol, used in skin products like moisturizers, sunscreens, cleansers, as well as hair products and makeup.

Today, it is one of the world’s most widely traded fruits and among the fastest-growing, highest-value commodities in global produce markets. Demand continues to expand faster than supply can keep pace, while production remains geographically concentrated.

Global production

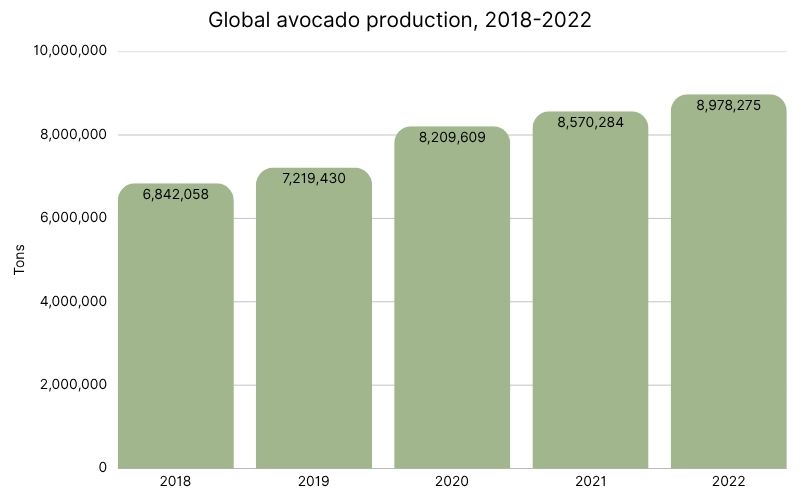

According to FAOSTAT data, global production was 11.2 million metric tons in 2024, up from 10.5 MT in 2023 and more than doubling over the past decade.

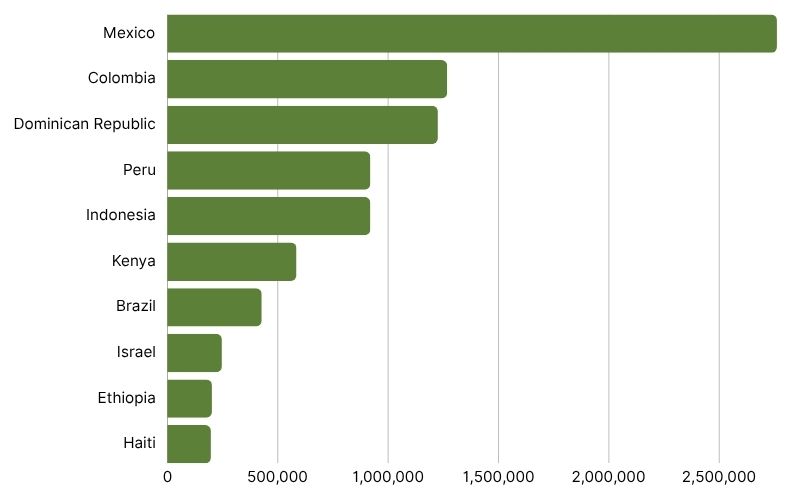

Production is heavily concentrated in a few countries. The Americas account for the majority of the global supply.

● Mexico (2.76 million MT): The world’s largest producer, producing about a quarter to a third of global output. The state of Michoacán dominates production and exports.

● Colombia (1.27 million MT): The second-largest producer, with rapidly expanding Hass avocado cultivation driven by export demand.

● Dominican Republic (1.23 million MT): A major producer with various local green-skin varieties, strong domestic consumption, and export-oriented production.

● Peru (0.92 million MT): A leading global exporter focused on counter-seasonal supply to Europe and North America.

● Indonesia (0.92 million MT): Significant planted area, but production is mostly consumed domestically.

● Kenya (0.59 million MT): Africa’s leading producer, with production reaching record levels in recent years as export-oriented farming expands.

● Brazil (0.43 million MT): Historically focused on domestic markets, but now increasingly tergeting export markets.

● Israel: (0.25 million MT): Recently, domestic production has expanded and exports primarily to Europe.

● Ethiopia (0.20 million MT): Africa's second-largest avocado producer.

● Haiti: (0.20 million MT): Primarily produces large West Indian avocado varieties.

Mexico dominates the global avocado market, producing 25% of world output. Mexico’s main growth regions, like Michoacán, have a warm, sub-humid climate, volcanic soils, and robust export infrastructure. The Mexican agricultural sector has expanded rapidly over the last few years, shifting from lower-value crops to export-oriented avocado production.

However, this high concentration of production also poses a risk to the global market. The top 5 countries account for 63% of global production, and the top 10 for 78%. Disruptions in production regions can rapidly affect global pricing. This happened during the 2024-2025 season, when extreme heat stress and droughts ravaged growing regions, disrupting fruit development and driving price increases globally.

The 2025–2026 campaign saw a partial recovery, thanks in part to a stronger Californian crop. Multi-origin sourcing is essential risk management for buyers.

Varieties

There are hundreds of avocado varieties, but the most commonly traded is the Hass variety, prized for its delicious taste, a darkening skin that signals ripeness, durable shelf life, and year-round availability across hemispheres.

In the U.S., the Hass variety accounts for 80% of the national avocado crop and 95% of California's. In Kenya, the Hass variety also dominates, accounting for 74% of national production in 2025, while the Fuerte variety accounted for the rest.

The Hass variety is so common that global trade logistics and retail systems have been built around it, including ripening management, packaging standards, and shelf life management.

Other common varieties include: Fuerte, Bacon, Pinkerton, Gwen, Lamb Hass, Reed, Choquette, and Zutano.

Trade

The OECD-FAO projects the export value of the avocado trade to reach about USD 10.4 billion by 2033.

Exporters

Mexico is the world's largest avocado exporter, with a net export surplus of about USD 4 billion in 2024. The FAO estimates that Mexico will remain the global export leader for the coming years, with a 53% share of global avocado exports by 2033.

Peru is the second-largest global exporter, with exports of about USD 1.49 billion in fresh and dried avocados in 2025. Its top destinations were the Netherlands, Spain, the United States, the United Kingdom, and Chile.

Colombia is another major exporter, followed by Brazil, Ecuador, Kenya, Morocco, and South Africa. Latin America will likely continue to dominate, with exports from Africa increasing.

The Netherlands is a major exporter by value. The country itself produced very little avocado, but it is Europe's central re-export hub, redistributing imported avocados across the EU.

Importers

The United States is the largest avocado importer, and so North–South trade flows between the U.S. and Latin America are a key structure of the market. The U.S. imported about 1.26 million tons of avocados in 2023, with the majority coming from Mexico.

Europe is the second-largest importer, as Spain's domestic avocado season is limited and requires counter-seasonal imports from Peru, Colombia, Chile, Kenya, Morocco, and South Africa.

Retail, consumption and demand

The United States is the world's largest consumer, consuming about 3 billion pounds a year, or about 9.2 lb per person (2023/24). The country's consumption has risen sharply over the last few decades as the fruit gained popularity through greater health awareness, the phytosanitary ban on Mexican Hass imports was lifted, and supply increased.

European demand keeps growing, with strong demand sustaining high prices through 2024 and into 2025, though consumption varies widely by country, and lagging markets are catching up. High Peruvian summer volumes periodically pressure wholesale prices in Rotterdam and Spain.

Asia is the fastest-growing region for avocado demand. China is among the fastest-growing destinations for Peruvian avocados in 2024–2025. However, this market is heavily influenced by price, habit formation, and macro conditions.

Market and price drivers

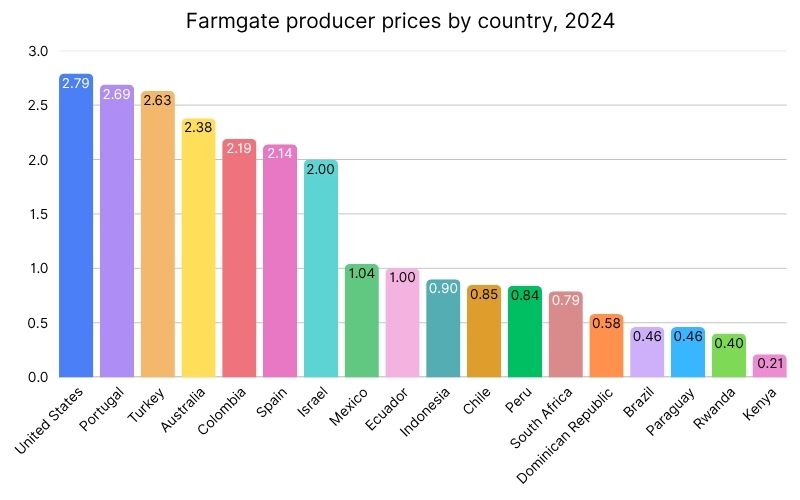

Avocados do not trade on a futures exchange; prices form at the producer level. This makes the market prone to sharp, supply-driven swings. Supply drives short-term prices rather than demand.

Origin windows matter enormously. The U.S. market sources from Mexico, California, Peru, Chile, and Colombia, each with an optimal quality window; Kenya's main export window runs March–September with a premium off-season secondary harvest; Peru peaks in the European summer. Managing fruit into the right window at the right quality is a core competitive skill.

Post-harvest technology, including controlled-atmosphere shipping and ripening protocols, extends shelf life and enables access to distant markets, helping to smooth volatility and expand the addressable market.

Outlook

The avocado market will continue to grow in the coming years, cementing its place as the highest-value tropical fruit in trade. Mexico is expected to retain export leadership, with Peru and Colombia consolidating, and Africa and emerging Latin American countries diversifying supply.

For producers and exporters, diversifying markets can help reduce the risks associated with geographic concentration, and investing early in compliance and traceability is equally important. Manage fruit quality within the right seasonal window and consider value-added processing, such as oil, guacamole, or frozen avocado, to monetize lower-grade fruit and capture margin.

For importers, retailers, and foodservice operators, it’s also important to have a multi-region sourcing plan to avoid production concentration and price volatility. Watch out for supply-driven price swings.

For processors, the prepared-foods and oil segments are growing fast. Avocado oil is growing in demand and production. These value-added products are likely to become an increasingly important source of competitive advantage.

The future of the avocado market will depend on a sustainable, reliable supply across borders and the evolving trade-policy landscape.